SUPA Consolidated Inc. Betting on Food Tech: Transition Challenges and Opportunity Scope

SUPA’s latest quarterly filings confirm its ongoing pivot from autonomous vehicle technology to an early-stage food tech venture amid tight liquidity.

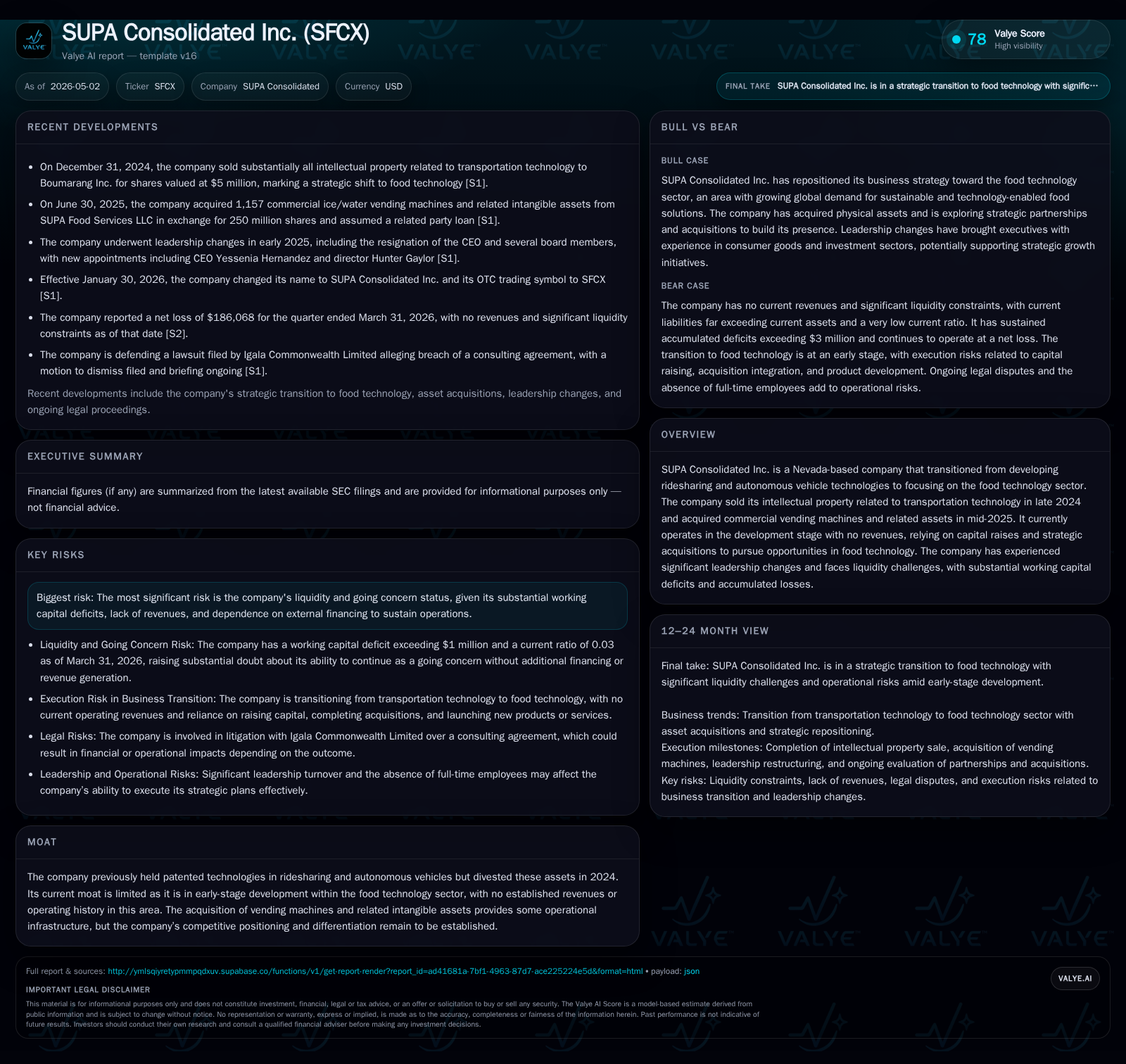

SUPA Consolidated Inc., formerly a player in ridesharing and autonomous vehicle technology, has divested its intellectual property assets to reposition as a food technology company focusing on commercial vending operations. The May 2026 quarterly report reconfirms the firm’s development-stage status with no revenues and significant working capital deficits, underscoring liquidity and execution risks. Strategic acquisitions of vending machines provide initial operational infrastructure, but SUPA’s path to sustainable growth hinges on raising additional capital and successfully establishing itself in a competitive, innovation-driven food tech market.

LATEST QUARTERLY OPERATING UPDATE: An Early-Stage Food Tech Transition

SUPA’s latest quarterly filing dated May 1, 2026 [S2] confirms it continues to operate without generating revenues and remains classified in the development stage as it pivots from its former ridesharing and autonomous vehicle business to food technology. Operationally, expenses have risen due to the increased activity surrounding legal fees, professional services, and rental costs linked to integrating its newly acquired commercial vending machine assets. The company has also solidified leadership changes initiated in early 2025, aiming to stabilize governance through new appointments. Despite these operational shifts, SUPA reported no topline sales, reflecting that commercial traction remains elusive as of the quarter-end.

BUSINESS MODEL EVOLUTION: From Patented Transportation IP to Commercial Vending Assets

Until late 2024, SUPA focused on ridesharing enabling technologies underpinned by patented AI and machine learning applications designed to optimize dispatch and customer pricing strategies [S1][S21]. However, on December 31, 2024, SUPA divested nearly all transportation-related intellectual property—including software, patents (notably U.S. Patent Nos. 9,984,574 & 11,217,101), trade secrets and goodwill—to Boumarang Inc., receiving approximately $5 million worth of Boumarang common shares in exchange [S1][S24]. This transaction marked a definitive break from its original Autonomous Vehicle tech business model.

The company’s current business model now centers on owning and operating commercial vending infrastructure primarily through its acquisition in mid-2025 of SUPA Food Services LLC [S6]. This deal transferred over 1,100 ice and water vending machines along with intangible assets such as location rights and customer contracts valued collectively at around $40,800 [S6][S25]. The acquisition was settled by issuing SUPA common stock totaling $125,000 in value accompanied by assumption of related party loan obligations. Presently, SUPA’s revenue generation strategy relies heavily on leveraging this tangible asset base to enter the food service delivery value chain while exploring further acquisitions or partnerships within food tech.

However, beyond the acquired vending machines infrastructure, SUPA lacks proprietary food technology or differentiated product offerings—a factor that keeps it firmly in early-stage development without proven monetization capabilities.

INDUSTRY CONTEXT AND COMPETITIVE POSITIONING: Navigating Food Tech Challenges Without Legacy Moat

The global food technology sector is undergoing rapid transformation driven by consumer preferences for healthier foods, sustainability mandates, and digitization of supply chains. This creates opportunity for companies with innovative technologies enabling healthier options or more efficient distribution [S1]. Nevertheless, SUPA enters this crowded sector without an established technological moat unlike its past transportation IP portfolio which included patented solutions with some market defensibility.

SUPA's competitive disadvantage originates mainly from two sources: absence of proprietary food-tech inventions and lack of any operational history generating market traction or revenue. The company’s offering currently extends only as far as operating a network of commercially acquired vending machines rather than offering transformative food tech services or products that meet emergent consumer demands uniquely.

While ownership of physical vending assets provides operational leverage into retail environments and direct customer touchpoints, competition includes numerous incumbents ranging from FMCG brands innovating via technology-enhanced foods to digital platforms enabling last-mile distribution. Without a clear technological or brand differentiation strategy demonstrated in its filings or recent activities so far, SUPA faces significant hurdles establishing sustainable competitive positioning.

GROWTH DRIVERS: Capital Raises, Strategic Acquisitions, and Food Tech Market Potential

Given the company's development status with no revenue streams yet realized, fresh capital infusions are vital growth enablers. The filings highlight a reliance upon external equity or debt financing to fund ongoing operations including integration costs related to acquisitions as well as research into prospective new products or partnerships within food tech [S1][S6].

Strategic acquisitions present potential pathways for growth beyond the initial vending machine network—though such moves carry integration risk given limited operating scale thus far. SUPA appears attuned to current macro trends favoring sustainability-oriented food tech initiatives which may attract investor interest if materialized effectively [S1]. However, successful translation of these opportunities into concrete revenue generation remains uncertain.

Operationalizing acquired assets into revenue-producing units while scaling will require expanding distribution agreements or partnering with branded product manufacturers aligned with evolving consumer choices for healthier options—steps implied only qualitatively without disclosed KPI metrics at this stage.

RISKS AND CONSTRAINTS: Liquidity Crunches, Operational Uncertainty, and Execution Risks

The prevailing risk landscape is dominated by financial constraints that threaten continue operations absent timely capital injection. As reported for March 31, 2026 quarter end based on companyfacts data supplemented by SEC filing disclosures [F1][S7], SUPA suffers from a perilously low current ratio approximating 0.03—reflecting current liabilities vastly exceeding liquid current assets ($41k vs $1.31m respectively). This working capital deficit underscores critically constrained liquidity.

Accumulated deficit totals roughly $3 million further compound concerns around sustained cash flows given zero historical revenue performance since pivot initiation [F1][S7]. These issues spawn substantial doubt about going concern assumptions explicitly discussed within SEC notes highlighting dependency on continuous funding rounds [S7]. Additionally, ongoing legal proceedings such as the January 2026 lawsuit filed by Igala Commonwealth Limited seeking additional share issuance contingent on disputed contractual provisions introduce potential contingent liabilities that may exacerbate financial frailty [S23].

Aside from balance sheet stressors are operational risks tied to limited track record managing food tech ventures or converting existing vending machine holdings into profitable business lines. Leadership changes during this transition raise questions regarding strategic continuity even though newer executives bring diverse experience aligned with industry aspirations [S6][S25]. Execution challenges are therefore multifaceted — spanning finance availability through business model validation.

LOOKING AHEAD: Key Milestones and Capital Raising as Turning Points

Investors navigating SUPA’s trajectory should focus tightly on near-term corporate milestones related primarily to financing events enabling sustainability beyond twelve months forward horizon given scarce internal cash generation capacity [S2][S1]. Progress or announcements around closing additional funding rounds—whether debt or equity—as well as firming up strategic partnership agreements within food tech will be critical leading indicators.

Other key markers include whether SUPA can demonstrate operational ramp-up translating acquired vending machine footprint into measurable revenue streams or successful launch of any licensable food tech products contemplated but not yet detailed in filings. Observing stability within executive leadership team following recent turnovers will also be relevant for gauging managerial execution competency [S25].

Preliminary resolution outcomes regarding ongoing litigation could alleviate some contingent threat factors affecting investor confidence.

Qualitative proxies might dominate until concrete bookings or sales data emerge given early-stage nature but monitoring SEC quarterly disclosures for evolving expense structures alongside working capital trends remains prudent.

FINANCIAL PROFILE: Current Liquidity, Debt Position, and Working Capital Deficit

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $41035 | |

| 2026-03-31 | ||

| Current liabilities | $1314173 | |

| 2026-03-31 | ||

| Current ratio | 0.03x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value ($) | Period End |

|---|---|---|

| Current Assets | 41,035 | |

| 2026-03-31 | ||

| Current Liabilities | 1,314,173 | |

| 2026-03-31 | ||

| Current Ratio | 0.03 | |

| 2026-03-31 |

As per the most recent reports and companyfacts snapshot metrics [F1], SUPA holds modest current assets totaling just above $41k at quarter-end versus staggering current liabilities exceeding $1.3 million—resulting in an acute liquidity imbalance where less than four cents of current assets back each dollar owed short term.

Total debt is estimated at approximately $244k based on best available data trailing into late 2023 periods; subtracting likely minimal cash balances results in net debt near $234k illustrating moderate leverage though overshadowed by broader working capital tension given immediate obligations outstrip available resources substantially [F1].

Operating losses contributing cumulatively to roughly $3 million deficit underscore ongoing negative cash flow dynamics which coupled with negligible revenues reaffirm critical reliance on external capital resources for survival [F1][S7].

This analysis strictly reviews factual disclosures from SEC filings complemented by validated financial snapshots without speculative forecasts or investment guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments