Syndax Pharmaceuticals Advances Cancer Therapy Commercialization with Strong Liquidity and Ongoing R&D

The latest quarter underscores Syndax’s focus on co-commercializing approved cancer therapies while managing collaboration costs and maintaining robust liquidity.

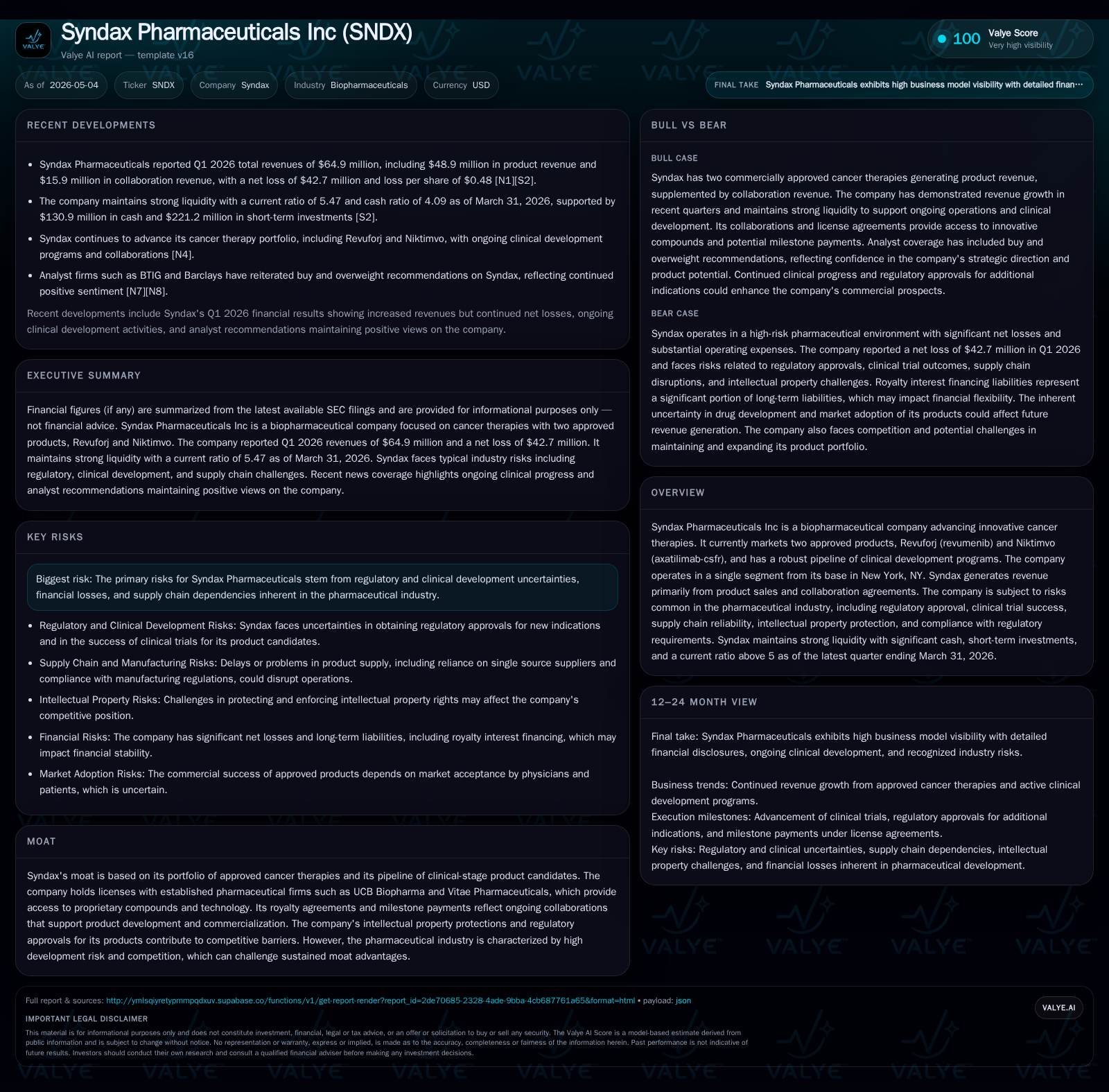

Syndax Pharmaceuticals reported its first quarter of 2026 financial results with ongoing commercialization of two approved cancer therapies, Revuforj and Niktimvo, underpinned by a key collaboration with Incyte. The company continues to invest heavily in research and development, sharing costs and profits on axatilimab-based therapies in the U.S., while maintaining a strong balance sheet with cash reserves of $130.9 million and a current ratio above 5. Syndax faces typical biotech industry risks such as regulatory uncertainties and clinical trial dependencies but benefits from proprietary licensing agreements that support its product pipeline and competitive positioning.

Recent Operating Update

Syndax Pharmaceuticals' latest quarterly filing dated April 30, 2026 [S2], along with the concurrent 8-K reporting the Q1 financial results [S3], anchors the current view on the company's operational status. The company reported no material impairments to assets as of March 31, 2026, indicating stable asset valuation amidst an active development environment. Syndax continues commercial activities around its two approved oncology products—Revuforj (revumenib) and Niktimvo (axatilimab-csfr)—with revenues primarily generated through product sales integrated with collaboration profit-sharing mechanisms.

The revenue profile includes recognition of collaboration revenue reflecting Syndax's share of profits or losses on the co-commercialization of Niktimvo within the U.S., a direct result of the partnership agreement with Incyte initiated in September 2021 [S26]. This arrangement positions Incyte as principal for sales outside the U.S., where royalties apply instead.

Financially, Syndax maintains a robust liquidity buffer: cash and equivalents stood at approximately $130.9 million at quarter-end March 31, 2026, complemented by total current assets of roughly $471.2 million against current liabilities of $86.2 million—yielding a strong current ratio near 5.47 [F1]. This liquidity framework provides runway to sustain R&D investments and navigate regulatory cycles without immediate refinancing pressures.

Business Model Overview

Syndax operates as a commercial-stage biopharmaceutical entity focused exclusively on oncology therapies. The company derives income through three primary channels:

- Product Sales: Direct sales of their two FDA-approved products for targeted cancer indications.

- Collaboration Revenue: Revenue share from partnerships, most notably with Incyte for co-commercializing axatilimab in the United States.

- Milestone and Royalty Payments: Income linked to licensing in-licensed compounds or technology from entities such as UCB Biopharma and AbbVie’s subsidiary Vitae Pharmaceuticals.

The business model is anchored on leveraging in-licensing agreements to access proprietary oncology compounds, developing clinical candidates internally or jointly, obtaining regulatory approvals for niche unmet medical needs in oncology and fibrotic diseases, then commercializing those assets either directly or through collaborations.

The company's cost structure reflects high R&D expenditures crucial for advancing its pipeline alongside commercialization expenses necessary to support market adoption of Revuforj and Niktimvo. Shared cost arrangements under the Incyte license allocate approximately 55% of U.S.-focused development costs to Incyte versus Syndax’s 45%, balancing risk exposure [S26].

Industry Structure and Competitive Position

Operating solely within innovative cancer therapeutics, Syndax competes in a crowded landscape marked by sizable pharmaceutical companies deeply invested in oncology R&D as well as smaller biotech firms aiming for first-in-class treatments. The industry requires rigorous scientific validation through costly clinical trials coupled with navigating complex regulatory pathways.

Syndax differentiates itself through specialized focus on epigenetic regulators (Revuforj) and immunomodulatory biologics (Niktimvo), which address refractory hematological malignancies and chronic graft-versus-host disease respectively. Their strategic licensing deals underpin access to compounds not originally developed in-house but integrated into their portfolio to accelerate commercialization timelines.

The partnership with Incyte demonstrates adaptive go-to-market strategy employing collaborative commercialization models that blend revenue sharing with cost risk mitigation—common among mid-tier biotech firms seeking scale without full commercialization overheads.

Nonetheless, competition is intense given multiple therapeutics vying for approval in overlapping indications alongside emerging modalities such as CAR-T therapies or bispecific antibodies reshaping treatment paradigms.

Growth Drivers

Pipeline Momentum

Growth prospects hinge largely on progressing their clinical-stage programs through pivotal trials toward regulatory approval extending beyond their existing products. Syndax's ongoing investments aim to enhance label indications for Revuforj (revumenib) and broaden patient populations addressed by Niktimvo.

Collaboration Expansion & Milestones

Incyte's role as commercialization partner ex-U.S. expands geographic reach potentially unlocking royalty revenue alongside milestone payments contingent upon clinical progress or market entry triggers.

Market Adoption & Reimbursement

Improved physician awareness coupled with pricing strategies underpinning reimbursement alignment are vital growth levers especially given the specialty nature of their therapies targeting difficult-to-treat cancers where few alternatives exist.

Strategic Licensing Deals

Continued licensing arrangements providing novel compounds can replenish pipeline depth or add complementary mechanisms bolstering Syndax's long-term innovation capacity.

Risks & Constraints

Regulatory & Clinical Trial Uncertainty

Given the inherent volatility in drug development success rates compounded by evolving regulatory standards, Syndax faces considerable execution risk impacting both timeline predictability and capital requirements.

Supply Chain Reliance

Delays or disruptions in sourcing active pharmaceutical ingredients or manufacturing compliance issues could hinder product availability affecting sales trajectories.

Dependency on Collaborations

While collaborations reduce capital outlay risk, they introduce shared decision-making complexity; adverse performance by partners like Incyte could adversely affect revenue flow or operational agility.

Intellectual Property Challenges

Maintaining patent exclusivity amidst biosimilar competition remains an ongoing legal battleground essential for protecting revenue streams from approved products.

What to Watch Next

- Clinical Development Milestones: Progression timing for trials expanding indications for Revuforj/Niktimvo or advancing pipeline candidates toward registration phases.

- Regulatory Approvals: FDA or EMA decisions broadening drug labels particularly addressing refractory cancers or fibrotic conditions.

- Commercial Performance Updates: Quarterly sales metrics reflecting market penetration trends post-launch along with revenue share impacts from partnership structures.

- Collaboration Announcements: Any extension or adjustment of agreements like that with Incyte signaling shifts in strategic direction or financial arrangements.

- Financial Guidance & Liquidity Management: Any updates concerning spending plans relative to cash reserves highlighting sustainability over multi-year development horizons.

Financial Profile Summary (Q1 2026 Highlights)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $131mm | |

| 2026-03-31 | ||

| Current assets | $471mm | |

| 2026-03-31 | ||

| Current liabilities | $86mm | |

| 2026-03-31 | ||

| Current ratio | 5.47x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As per the Q1 filings [S2][F1], Syndax holds a strong liquidity position without material impairments reported recently. Total debt appears relatively modest compared to cash holdings and does not constrain near-term operating flexibility [F1]. Sustained R&D spend coupled with collaboration expense-sharing agreements frames a capital-efficient growth pathway although profit margins remain pressured due to high fixed operating costs typical among biopharma companies at this stage.

Disclaimer: This analysis is furnished solely for informational purposes based on publicly available SEC filings and news sources as of May 4, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments