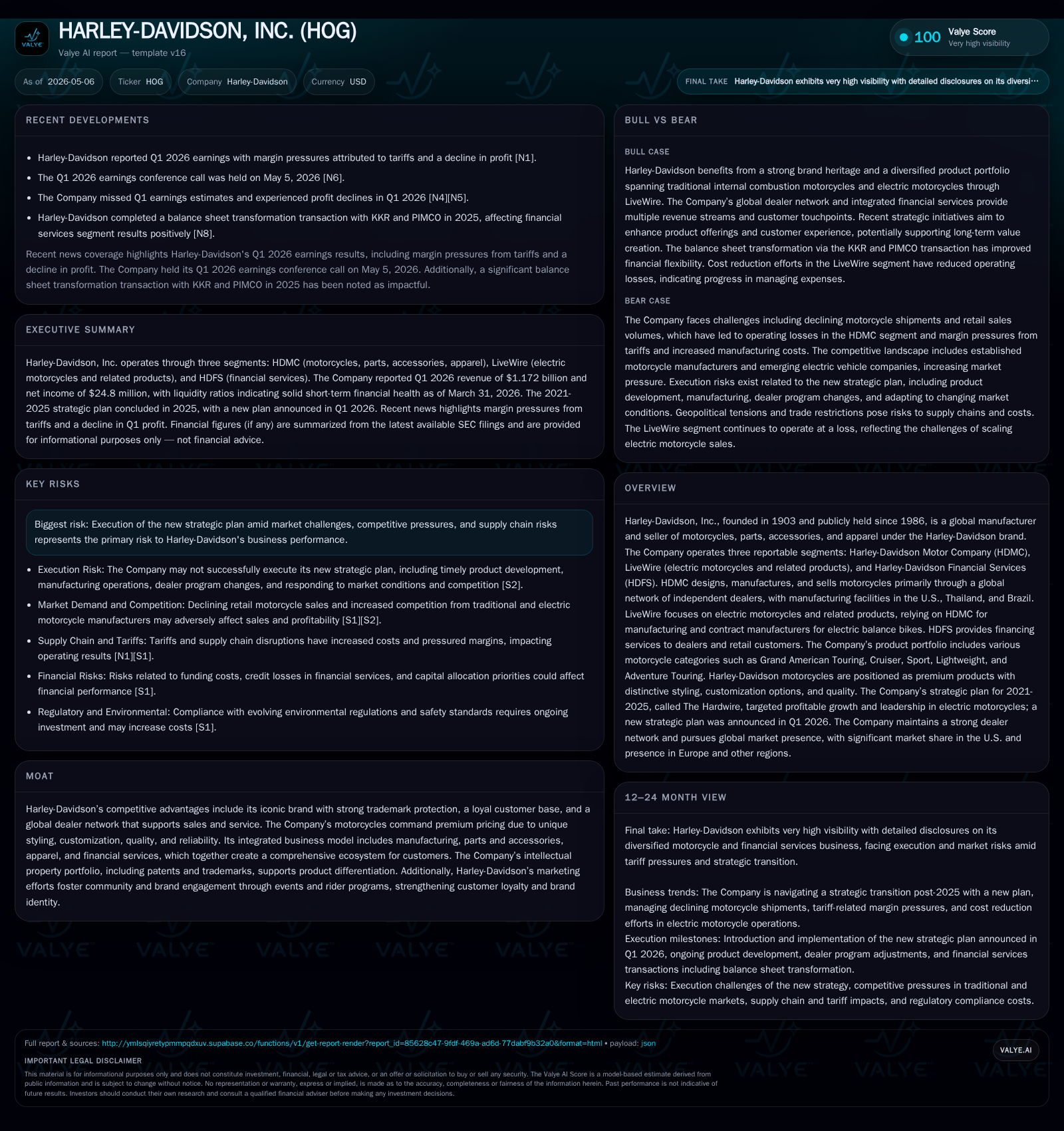

Harley-Davidson Confronts Tariff Pressures and Strategic Shifts in Q1 2026

Q1 2026 results highlight tariff-related margin compression and mark the launch of a new strategic plan amid a challenging motorcycle market.

Harley-Davidson’s first-quarter 2026 earnings reflect ongoing headwinds from tariffs and softer consumer demand despite efforts to optimize product mix and pricing. The company rolled out its new Back to the Bricks strategic plan, emphasizing product innovation, dealer engagement, and operational adaptability to stabilize sales. The legacy Harley-Davidson Motor Company segment continued to face volume declines, while LiveWire's electric vehicle losses narrowed with rigorous cost control. Financial Services repositioned its portfolio post a significant receivables sale, affecting near-term income streams but reducing funding risk. Key risks remain tied to execution of the new strategy under persistent macroeconomic and geopolitical uncertainties.

Recent Operating Update: Q1 2026 Earnings and Strategic Shift

Harley-Davidson reported its first-quarter results for the period ending March 31, 2026, on May 5, revealing continued pressure on margins from elevated tariff costs combined with volume softness across core markets [S2][S3][N1][N2]. The quarter's performance underscored the industry-wide headwinds impacting premium discretionary products amidst economic uncertainty and persistent high interest rates.

Net revenue trends reflected a contraction in worldwide retail motorcycle sales, with operating profit compression driven largely by the Harley-Davidson Motor Company (HDMC) segment's lower shipments. Cost increases tied to new or increased tariffs implemented through 2025 further strained unit economics despite strategic price adjustments and efforts to optimize product mix [S2][S14].

The company simultaneously unveiled its "Back to the Bricks" strategic plan, aiming to recalibrate growth drivers by injecting fresh product innovation—including small displacement motorcycles—and stronger dealer collaboration frameworks [S17][S1]. This initiative replaces the Hardwire plan concluded at year-end 2025.

Business Model: Integrated Motorcycle Manufacturing with Financial Services Support

Harley-Davidson's business spans three reportable segments: HDMC focusing on design, manufacture, and sale of motorcycles along with parts, accessories, and licensed apparel; LiveWire serving the electric motorcycle niche including contract-manufactured e-balance bikes; and Harley-Davidson Financial Services (HDFS), which provides retail and dealer financing solutions [S1].

Revenue is primarily earned through motorcycle sales via a global network of independent dealers complemented by online retail channels for parts and accessories in select regions. HDMC’s product categories include Grand American Touring, Cruiser (traditionally its flagship styling segment), Sport, and Lightweight motorcycles.

LiveWire extends the brand into electric vehicle markets but has faced delays in broad consumer adoption prompting recalibrated investment focused on cost control [S5]. HDFS monetizes through interest income on retail finance receivables as well as loan servicing fees under new asset sale agreements that reduce balance-sheet risk.

Industry Structure and Competitive Position

Harley-Davidson dominates a niche of heavyweight premium motorcycles characterized by distinctive styling associated with American cruiser culture. It benefits from strong intangible assets including its iconic trademarks, loyal customer following developed over a century, and a dense dealer footprint exceeding 1,100 points globally [S1].

However, the industry confronts cyclical demand akin to other discretionary leisure goods exacerbated by macroeconomic headwinds such as elevated borrowing costs and volatile consumer confidence. The electric mobility trend challenges incumbent combustion-engine dominators like Harley-Davidson; LiveWire’s comparatively weak EV uptake reflects tougher competition from startups specialized in urban electric micro-mobility [S5].

Tariffs imposed in recent years at U.S. and foreign levels increase sourcing complexity and cost bases for manufacturing inputs—steel tariffs alone have imposed approximately $31 million cost load in 2025, with cumulative estimated impact rising in 2026 [S1][S2]. Given Harley’s U.S.-centered manufacturing base complemented by overseas production facilities in Thailand and Brazil for select models, supply chain localization limits some tariff exposure but does not eliminate it entirely.

Growth Drivers

Product Innovation Capability

The announced introduction of smaller displacement motorcycles planned for 2026 alongside an iconic classic cruiser refresh is central to recapturing younger or entry-level riders dissuaded by larger displacement choices or higher ownership costs [S1][S17]. This product expansion targets diversification across rider demographics addressing shifts towards urban mobility preferences.

Enhanced Dealer Engagement & Customer Experience

Evolving dealer support models aim to streamline inventory management against expected fluctuations in retail demand while enhancing experiential programs fostering community around Harley's lifestyle brand ethos. Expanded eCommerce channels for parts/apparel also serve growing digital direct-to-consumer demand segments.

LiveWire Cost Rationalization & Portfolio Focus

With slower EV adoption than originally forecasted due to limited incentives and infrastructure gaps, LiveWire is concentrating on establishing sustainable operations through aggressive cost reductions while selectively pursuing attractive urban mini-motorcycle niches relevant to contemporary mobility trends [S5].

Financial Services Portfolio Reengineering

HDFS completed significant sales of retail finance receivables during H2 2025 reducing funding requirements considerably while adopting Forward Flow Agreements that monetize future loan originations without holding full credit risk. This stabilizes capital allocation flexibility but tempers interest income contribution near-term [S21].

Risks / Watchpoints / Growth Constraints

- Execution Risk on New Strategic Plan: The Back to the Bricks plan depends heavily on timely new product development success, dealer transition management, adapting manufacturing cadence amidst volatile demand, and navigating geopolitical tariff uncertainties [S17]. Failure or delay could compound weak earnings.

- Tariff Uncertainty: Judicial challenges to US tariffs create volatility in cost forecasting; sustained or increased trade barriers potentially uplift input costs materially ($75-$105 million estimated tariff impact in 2026) affecting pricing power [S1][S2].

- Declining Motorcycle Retail Volumes: Broader leisure spending constraints and an aging demographic core constrain core HDMC sales volume with implications for manufacturing scale economics.

- Electric Vehicle Market Dynamics: Slower-than-expected EV adoption coupled with heightened competition threatens LiveWire profitability and market relevance.

- Financial Services Income Variability: Sale of finance receivables limits interest income stability even as it reduces balance-sheet risk creating near-term earnings pressure [S21].

- Supply Chain Disruptions: Potential interruptions due to raw material shortages or logistic challenges could exacerbate fixed cost absorption difficulties in manufacturing.

- Cybersecurity Governance Changes: Departure of Harley’s CISO during late 2025 introduces transitional cybersecurity risk though mitigated by experienced interim leadership [S1].

What To Watch Next

- The company's progress reporting against Back to the Bricks milestones including launch dates of new small displacement models will be key demand indicators.

- Quarterly shipment volumes relative to prior year periods will confirm if retail declines are stabilizing or accelerating.

- Updates on tariff litigation outcomes impacting expense forecasts.

- LiveWire’s ability to narrow its operating losses further through cost restructuring measures.

- HDFS financing portfolio growth patterns alongside interest income trajectory given ongoing asset sales under Forward Flow Agreements.

- Management commentary on dealer program adaptation effectiveness under evolving market conditions.

- Currency exchange rate movements affecting international revenues and costs given significant overseas sales presence.

- Capital allocation activity around share repurchases versus reinvestment will indicate confidence levels in growth prospects.

Financial Profile Summary

Harley-Davidson's liquidity remains robust entering Q2 2026 with cash & equivalents standing at approximately $1.81 billion against current liabilities of about $2.48 billion, yielding a healthy current ratio near 1.91 [F1][S2]. Net debt approximates $5.09 billion factoring outstanding total debt vs cash balances recorded per Q1 filings [F1].

Capital allocation continues balancing reinvestment needs for innovation alongside shareholder returns via dividends and discretionary share repurchases—16.8 million shares remain authorized for buyback as of quarter end after completing an accelerated share repurchase program totaling $200 million during recent quarters [S13][S16][S29].

Operating income was pressured notably within HDMC due to lower shipment volumes compounded by tariff costs despite gains from favorable pricing/mix actions noted during 2025 year-end context [F1][S14]. LiveWire’s reduced loss trajectory evidences disciplined expense management but remains a drag overall until broader EV market maturation occurs [S22]. HDFS saw elevated operating income last year partly related to credit loss releases from portfolio sales but expects tapering as financing assets diminish steadily [S23][S25].

Latest Financial Snapshot (as of Q1 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1805mm | |

| 2026-03-31 | ||

| Current assets | $4.7bn | |

| 2026-03-31 | ||

| Current liabilities | $2.5bn | |

| 2026-03-31 | ||

| Current ratio | 1.91x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period Ending |

|---|---|---|

| Cash & Equivalents | $1.81 billion | 03/31/2026 |

| Current Assets | $4.74 billion | 03/31/2026 |

| Current Liabilities | $2.48 billion | 03/31/2026 |

| Total Debt | $6.89 billion | End of Year (estimate, latest disclosed date) |

| Current Ratio | ~1.91 | 03/31/2026 |

Conclusion

Harley-Davidson's Q1 2026 results paint a picture of a legacy premium motorcycle brand wrestling with external macroeconomic pressures—primarily tariffs—and structural industry shifts toward electrification coupled with evolving consumer tastes. The newly launched Back to the Bricks strategic framework attempts to address these challenges through realigned product innovation focus, enhanced dealer partnerships, nimble manufacturing execution, and disciplined financial stewardship within its business units.

While tariff impacts continue eroding margins and demand softness weighs on volume leverage dynamics negatively affecting earnings quality in the near term, Harley-Davidson leverages deep brand equity and global distribution networks alongside incremental product initiatives as pillars for recovery potential across the medium term horizon. Success ultimately hinges on execution agility amid geopolitical uncertainties influencing supply chains plus sustained market adoption velocity for both traditional motorcycles and electrified alternatives offered via LiveWire.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments