Archrock, Inc. Faces Critical Turn in Debt Refinancing and Aftermarket Growth

Q1 2026 filings reveal Archrock’s refinancing milestones alongside operational pressures and aftermarket expansion potential.

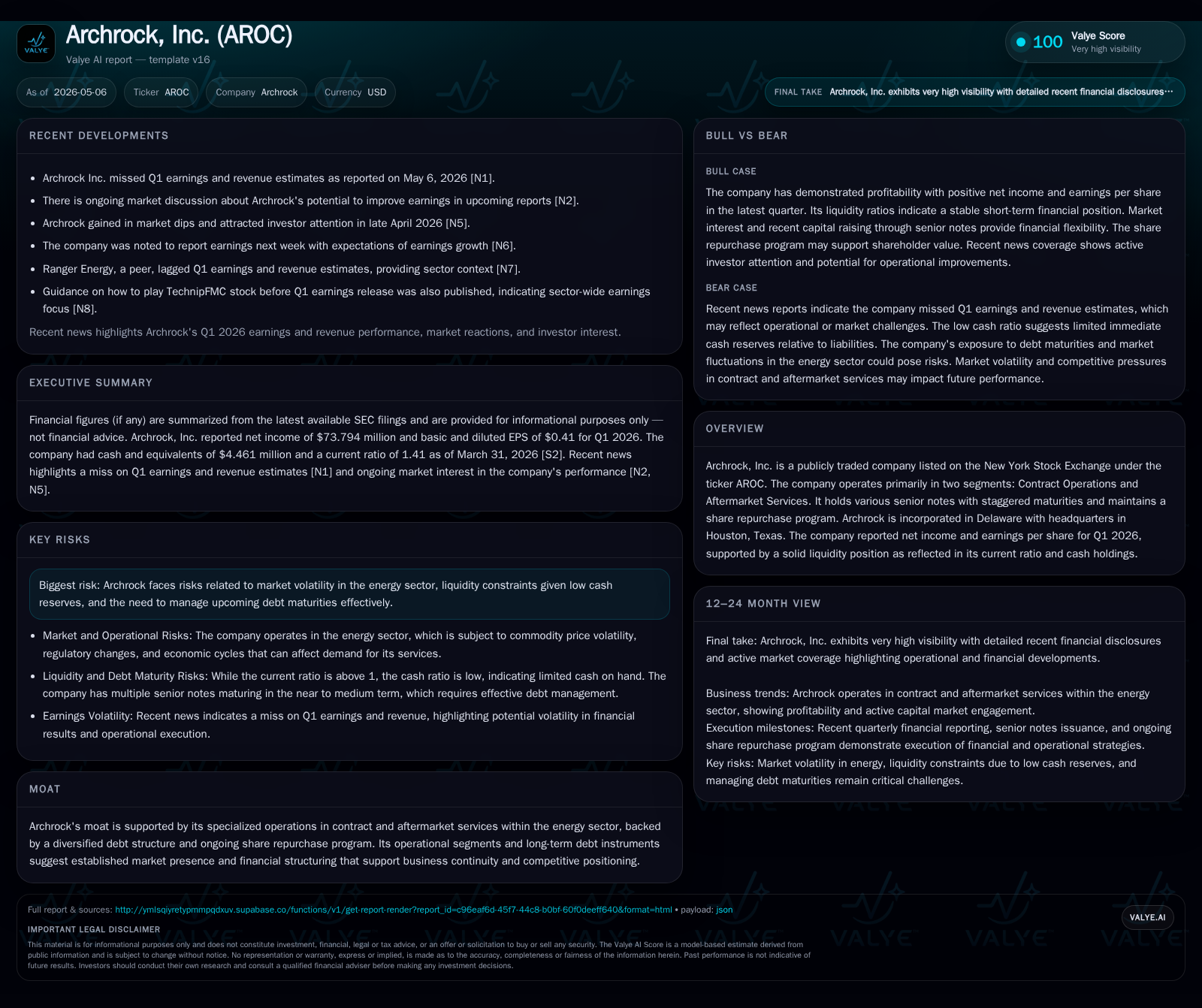

Archrock's latest 10-Q filing for Q1 2026 exposes a pivotal moment as the company completes the redemption of its April 2028 senior notes, significantly reducing credit facility utilization and improving financing flexibility. Despite solid contract operations anchored by large horsepower fleets in major U.S. basins, Archrock struggles with revenue and earnings misses amid market volatility. Its aftermarket services segment offers a path to margin improvement through enhanced parts and service offerings. However, liquidity remains tight against significant net debt, warranting close scrutiny of debt maturities and fleet utilization trends ahead.

Q1 2026 Operational Update Highlights

Archrock's May 6, 2026 10-Q filing outlined critical operational and financial developments that frame the company's near-term trajectory [S2][S3]. A centerpiece was the completion of the $800 million redemption of its April 2028 senior notes in April 2026, effectively removing this maturity from the immediate refinancing calendar and reducing dependence on revolving credit lines. This event tightened available facility usage sharply compared to prior quarters when the credit facility balance aggregated near $96.8 million at quarter-end versus over $918 million in December 2025 [S2].

The quarter also marked Archrock's adoption of FASB ASU 2023-05 concerning joint venture accounting effective for formations after January 1, 2025. By applying fair value measurements on JV asset/liability recognition upon formation, this change aims to provide greater clarity for investors on the financial profile of joint operations [S2]. This accounting shift may influence investor perception around archival JV disclosures but does not materially affect standalone operations.

Operationally, Archrock reported revenue and net income miss commentary in market releases dated early May 2026 [N1][S3], pointing towards some near-term softness tied to energy sector headwinds impacting compression demand hours. Despite these misses, cash flow from operating activities remained robust at approximately $185.9 million for Q1 [S22], supported by steady contract renewals.

Business Model Explanation: Contract Operations and Aftermarket Services

Archrock generates its revenue from two principal business segments: Contract Operations and Aftermarket Services [S1]. The Contract Operations segment delivers essential natural gas compression services using a fleet weighted heavily toward large horsepower equipment. These compressors operate under long-term contracts with customers primarily engaged in upstream production and midstream processing across major U.S. plays such as the Permian Basin and Eagle Ford Shale [S1].

This business is considered "must-run" due to its critical role in maintaining uninterrupted gas production volumes – no compression leads directly to loss of throughput and product flow downstream. Archrock leverages geographic density with approximately three-fourths of operating horsepower concentrated in these prolific basins enabling operational efficiencies by standardizing maintenance crews and minimizing logistics costs per unit horsepower deployed [S1].

The Aftermarket Services segment complements contract operations by providing maintenance, overhaul, reconfiguration services plus over-the-counter sales of parts/components required to keep compression equipment operational [S2][S25]. This creates an annuity-like revenue stream tied closely to the underlying installed base's uptime requirements with higher margin potential relative to contract services due to parts pricing leverage.

Recent strategic activity includes disposing smaller horsepower units (325k HP sold in year ended Dec 2025) to sharpen focus on larger units that better meet customer demand profiles for cost efficiencies and emissions compliance [S1].

Competitive Positioning and Industry Environment

Archrock enjoys a moat anchored predominantly in its scale leadership in total compression fleet horsepower within key U.S. shale regions [S1]. The concentration in Permian and Eagle Ford not only provides direct access to high-volume upstream customers but also delivers supply chain advantages unlikely matched by smaller competitors lacking geographic or scale density.

Through concentrated presence, Archrock benefits from operating leverage; administrative costs rise slower than fleet expansion enabling cost per horsepower reductions over time. Additionally, large horsepower units align with evolving industry trends favoring higher capacity compressors owing to regulatory pressures around emissions and operational efficiency mandates.

However, the company's fortunes remain tethered to natural gas demand cycles subject to commodity price swings affecting upstream drilling activity which drives compressor utilization. Pricing power is moderate given competition among compression service providers but somewhat insulated by contract durability and productivity expectations around midstream throughput reliability.

Capital intensity requirements act as a barrier for new entrants due to the high cost of acquiring and maintaining specialized compressor fleets along with requisite maintenance infrastructure.

Growth Trajectory and Key Drivers

Several factors underpin Archrock’s growth potential moving forward:

- Fleet Optimization: Continued divestiture of smaller horsepower assets reallocates capital toward upgrading or expanding large horsepower compressors that enjoy stronger market demand and improved ROI profiles [S1].

- Aftermarket Expansion: Growing penetration in parts sales enhances margins since these sales leverage existing customer relationships while consuming less capital than fleet expansions [S25]. Continuous innovation in service offerings could boost retention rates.

- Geographic Density Leverage: Deepening footprint within premier shale basins amplifies operating synergies such as consolidated service teams which decrease per unit service costs creating incremental profitability.[S1]

- Joint Venture Accounting Transparency: Implementation of ASU 2023-05 can encourage JV formations by offering clearer valuation bases for partners which may accelerate collaboration opportunities or asset-sharing arrangements adding revenue streams [S2].

Collectively these drivers reflect structural improvements more than cyclicality with operational efficiencies poised to sustain cash flow generation even amid volatile commodity markets.

Risks, Constraints, and Watchpoints for Investors

Archrock faces several notable risks influencing its near-term outlook:

- Liquidity Pressure: As of Q1 end March 31, 2026, cash reserves stood at approximately $4.46 million against current liabilities totaling $219.2 million resulting in a current ratio of roughly 1.41 placing pressure on working capital cushions amid ongoing operating expenses [F1][S2].

- Substantial Net Debt Load: With total debt at about $1.597 billion (best-effort estimate) netted against cash leaves around $1.59 billion net debt elevating refinancing risk especially as senior note maturities cluster over next few years; proactive management needed despite recent April 2028 note redemption easing immediate burden [F1][S17].

- Energy Sector Volatility: Fluctuations in natural gas prices or upstream drilling impact compressor utilization directly influencing revenue stability; downturns reduce contractual volume commitments potentially squeezing margins [N1].

- Competitive & Regulatory Pressures: Industry competitive intensity could compress pricing particularly if supply chain constraints ease or regulatory changes impose additional operational costs constraining pricing power.[S1]

Investors should monitor liquidity metrics closely along with management guidance around refinancing plans.

Upcoming Milestones and What to Watch Next

Key events and indicators signaling Archrock’s trajectory include:

- Follow-up quarterly earnings reports will be critical for evaluating whether contract operations revenues rebound post-Q1 misses seen May 2026 [N2,N6,S3].

- Updates regarding share repurchase program execution could signal management confidence or capital allocation priorities amid leverage reduction efforts [S2,S3].

- Monitoring progress on revolving credit facility strategies ahead of expiration dates remains essential given historical reliance before recent note redemptions [S17].

- Commentary on joint venture deals applying ASU 2023-05 accounting might shed light on partnership expansion success contributing incremental growth avenues [S2].

- Fleet utilization rates disclosed through guidance updates constitute a direct gauge of demand environment shifts.[N1]

Collectively these milestones will help discern operational resilience versus macro-driven headwinds.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $4mm | |

| 2026-03-31 | ||

| Current assets | $309mm | |

| 2026-03-31 | ||

| Current liabilities | $219mm | |

| 2026-03-31 | ||

| Current ratio | 1.41x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This snapshot underscores the delicate balance Archrock must maintain between servicing a substantial debt load while navigating working capital demands amid an uneven energy market.

This analysis is based solely on publicly filed SEC documents up to May 6, 2026, company disclosures, and recent market reports without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments