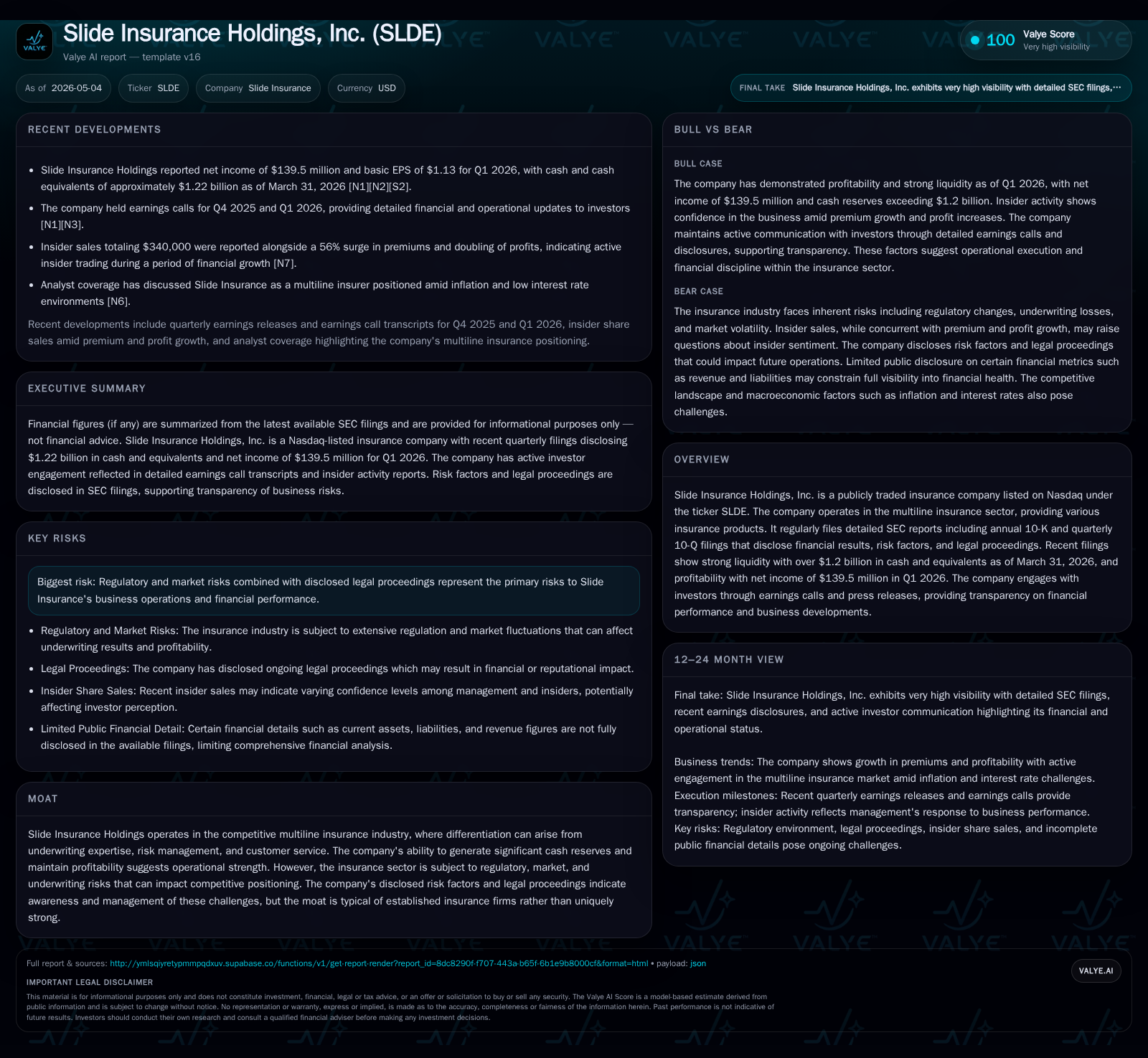

Slide Insurance Advances Share Buybacks After Strong Q1 Profit Performance

Slide Insurance announces a $100 million stock repurchase plan following robust Q1 2026 profitability, underscoring capital allocation confidence.

In its latest quarterly report, Slide Insurance Holdings, Inc. demonstrated significant profitability gains with net income of $139.5 million in Q1 2026 and enhanced shareholder value through authorization of a $100 million stock buyback program. The company's multiline insurance model continues to leverage underwriting discipline and premium growth, supported by strong liquidity exceeding $1.2 billion in cash reserves. Competitive positioning is typical for a midsize multiline insurer, balancing operational strength with regulatory and market risks. Upcoming catalysts include execution of the repurchase plan and monitoring premium expansion amid evolving market conditions.

Q1 2026 Operational Highlights: Profit Growth and Capital Return Authorization

Slide Insurance Holdings disclosed strong operating results in its 10-Q for the quarter ended March 31, 2026 [S2]. Notably, net income reached $139.5 million in Q1, evidencing meaningful profitability improvement driven by underwriting gains and controlled operating expenses. Complementing this financial progress, the company announced via an 8-K dated April 28, 2026, a board-approved common stock repurchase plan authorizing up to $100 million of share buybacks [S3]. This capital deployment strategy reflects management’s confidence in the underlying business fundamentals and signals intent to enhance shareholder returns following steady earnings growth.

The repurchase program's open-ended design allows purchases through diverse methods including open market transactions and Rule 10b5-1 trading plans, providing flexibility aligned with market conditions and company strategy. Given the timing shortly after Q1 results release, this move recalibrates near-term investor expectations regarding capital allocation priorities while preserving balance sheet strength.

Business Model and Product Quality: Multiline Offerings Driving Customer Value

The company's foundational model centers on multiline insurance products spanning personal lines (e.g., auto, homeowners) and commercial lines (e.g., small-to-mid-size business coverage) [S1]. This diversified portfolio mitigates segment-specific volatility inherent to insurance underwriting cycles and spreads risk across heterogeneous customer bases. Slide leverages underwriting expertise to selectively price risk pools while maintaining disciplined claims management.

Customer retention benefits from modest switching costs tied to policy bundling capabilities and service quality initiatives. As an insurance holding company with vertically integrated underwriting and claims operations, Slide emphasizes risk-adjusted profitability over volume alone. The multiline approach aids in smoothing periodic earnings swings common in narrowly focused insurers yet depends heavily on effective pricing-to-risk calibration amid evolving loss trends.

Competitive Positioning Within the Multiline Insurance Industry

Within the competitive landscape of midsize multiline insurance carriers, Slide occupies a position characterized by solid operational execution but typical industry-wide pressures [S1]. Pricing power remains constrained by market comparisons and regulatory scrutiny; claims inflationary pressures continue to require agile underwriting adjustments. Regulatory compliance costs and litigation exposure further shape competitive dynamics as detailed in recent risk disclosures [S24].[S22]

While liquidity reserves afford operational flexibility uncommon to smaller peers, Slide’s moat is neither uniquely broad nor deeply entrenched—it aligns with standard incumbency advantages such as established distribution relationships and brand recognition without distinct technological or scale-based differentiation.

Growth Drivers: Premium Expansion, Underwriting Excellence, and Market Penetration

Recent disclosures highlight a substantial pickup in premium volumes—a 56% surge reported in secondary sources underscores robust top-line momentum born from selective book expansion and rate increases [N8][S2]. Such premium growth is instrumental in scaling revenue while leveraging underwriting discipline to improve combined ratios.

Operational management suggests ongoing initiatives targeting underserved client segments via tailored product offerings alongside geographic market expansion within regulatory frameworks. These strategies aim at capturing incremental premium while preserving loss ratio improvements noted in Q1 results. Measurable KPIs include new policies written, renewal rates indicating retention health, combined ratio trending below unity reflecting underwriting profits, and booking trends signaling sustained demand.

Risks and Constraints: Regulatory Environment, Legal Matters, and Market Volatility

Slide’s filings consistently foreground regulatory risk as a key challenge given the complexity of multilayered state insurance regulations impacting rate filings, reserve adequacy standards, and capital requirements [S24][S22]. Material ongoing legal proceedings detailed in the annual filing pose reputational or financial risks that remain subject to litigation outcomes [S1]. Additionally, sector cyclicality influences underwriting margin trajectories; adverse claim developments or catastrophe occurrences could constrain margin expansions realized earlier in 2026.

Prudent risk management frameworks remain essential amid these headwinds. Investors monitoring Slide should note potential effects of regulatory changes or unfavorable court rulings on future earnings variability.

Near-Term Catalysts and Monitorables: Guidance, Repurchase Execution, and Premium Trends

Looking ahead, key execution milestones revolve around the pace of share repurchases under the new board authorization—with buyback activity serving as a tangible gauge of capital return commitment [S3]. Quarterly earnings updates will clarify whether premium growth sustains post-Q1 momentum or adjusts due to competitive or macroeconomic shifts [N1]. Management commentary during upcoming calls will likely address guidance trajectories integrating these factors.

Investors may also track combined ratio movement as an indicator of ongoing underwriting discipline effectiveness alongside market share shifts within target segments.

Latest Financial Snapshot: Liquidity, Profitability, and Balance Sheet Strength

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1218mm | |

| 2026-03-31 | ||

| Total debt | $35mm | |

| 2026-03-31 | ||

| Net debt | $-1183mm | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

| --- | --- | --- | | Cash & Equivalents | $1.22 billion | 2026-03-31 | | Net Income | $139.5 million (Q1) | 2026-03-31 | | Total Debt | $35 million | 2026-03-31 |

As reflected above based on most recent filing data [F1], Slide Insurance maintains considerable liquidity exceeding $1.2 billion against modest total debt levels around $35 million as of quarter-end March 31. This results in a net cash position providing strategic capacity for operational investments or additional shareholder distributions if warranted. The financial profile complements the operational narrative of sustained profit generation with conservative leverage conducive to absorbing sector cyclicality.

This analysis synthesizes information from Slide Insurance Holdings’ latest SEC filings including the Q1 2026 Form 10-Q [S2], subsequent event disclosures around share repurchases [S3], annual business model context from the Form 10-K [S1], as well as corroborating news sources capturing operational commentary and market perspectives. It aims to provide an objective internal memo-style perspective on current performance drivers balanced against inherent insurance sector risks without delivering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments