NVR Inc. Updates Show Sales Pressure in Early 2026 Despite Strong Cash Position

NVR’s Q1 2026 results reveal revenue and earnings softness triggered by mortgage rate-driven housing demand decline, balanced by substantial liquidity and resilient business fundamentals.

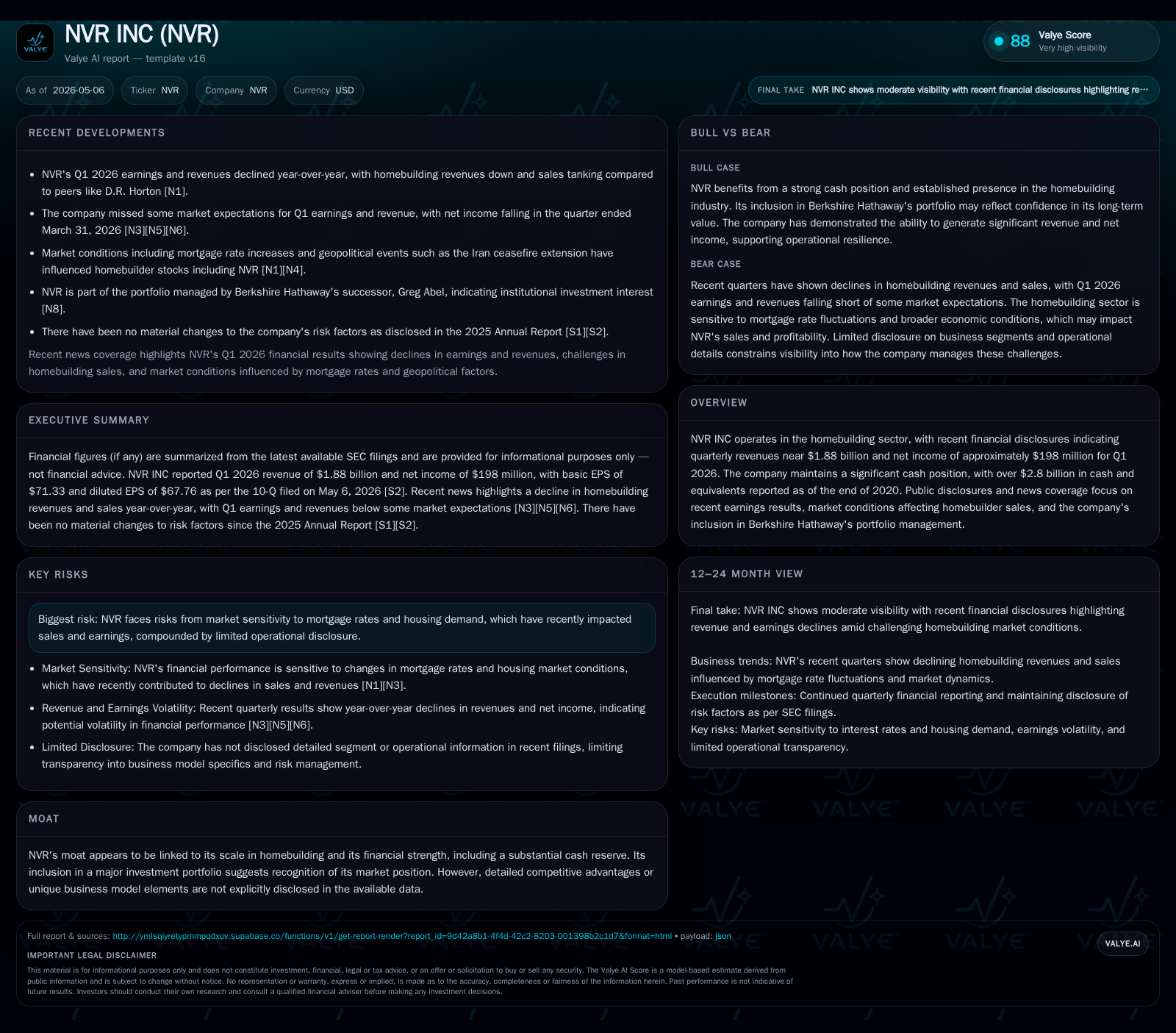

NVR Inc.’s latest quarterly filing dated May 6, 2026 [S2] unveils a year-over-year revenue contraction to approximately $1.88 billion and net income near $198 million for Q1 2026, missing earnings expectations amid challenging mortgage rates. The homebuilder continues to operate within a capital-intensive model heavily reliant on single-family home sales, supported by an integrated mortgage banking segment detailed in its February 11 annual report [S1]. Although the industry faces persistent cyclical headwinds driven by higher rates impacting affordability, NVR’s substantial cash reserves reported historically [F1] provide a buffer for near-term volatility. The company’s scale and strong balance sheet distinguish it amid intense competition from peers like D.R. Horton and PulteGroup [N1, N12]. Monitoring mortgage rate trends and order backlog developments will be critical in assessing recovery potential as management addresses these market pressures.

Latest Quarterly Operating Update: Sales and Earnings Softness

NVR’s May 6, 2026 quarterly filing (10-Q) details a soft start to the year marked by significant declines in both sales and profits compared to the prior-year quarter [S2]. Total revenues for Q1 stood near $1.88 billion—a notable decrease reflective of sluggish new home orders as mortgage rates elevated beyond recent lows. Net income retreated to approximately $198 million, underperforming consensus expectations noted in news summaries immediately following the April earnings release [S3], [N2], [N4], [N9]. Management commentary embedded within the filing indicates persistent headwinds attributed primarily to affordability constraints imposed by the mortgage market environment.

No changes were made to previously disclosed risk factors concerning housing market volatility or interest rate sensitivity in this quarter’s report [S2], underscoring ongoing uncertainty rather than new operational surprises.

Understanding NVR’s Business Model and Homebuilding Offering

The backbone of NVR’s revenue generation lies in constructing and selling single-family detached homes concentrated across key metropolitan regions in the United States as outlined in its annual filing dated February 11, 2026 [S1]. The company prioritizes product quality with a streamlined build-to-order approach aimed at balancing customization preferences without imposing excessive construction timelines or inventory risk.

A strategic component of its model includes an integrated mortgage banking segment that facilitates buyer financing—both simplifying transaction flows and potentially cushioning demand volatility through cross-selling opportunities [S1]. The vertical integration aspect enhances control over financing terms which is critical given the sensitivity of buyers’ purchasing power to interest rate movements.

Geographic concentration enables operational focus but also exposes the company to regional economic trends influencing employment patterns and demographic shifts relevant to housing demand.

Competitive Positioning and Industry Dynamics in Residential Construction

Within the U.S. homebuilding sector — populated by major players such as D.R. Horton (DHI) and PulteGroup (PHM) — NVR holds competitive strength primarily through its sizable scale and robust financial position [N1], [N12], [N13]. Unlike some competitors investing heavily in niche or speculative land accumulation strategies or offering significant product differentiation via luxury segments, NVR operates with a conservative land acquisition stance augmented by lean inventory management as detailed annually [S1].

This translates into predictable operational cadence but limits distinct moats built around exclusive designs or unique construction methods. Pricing power is generally constrained given that buyers often compare across multiple standard builder offerings amid fluctuating input cost inflation including labor shortages and materials pricing.

Regulatory frameworks governing zoning and building approvals further add complexity that all industry participants must navigate concurrently.

Growth Drivers: Potential Catalysts for Recovery and Expansion

Primary growth catalysts for NVR revolve around improvements in mortgage market conditions where modest declines from peak interest levels could reinvigorate buyer appetite for new homes [N6]. Elevated cancellation rates experienced recently could reverse with more favorable financing terms supporting order book stabilization.

Additionally, any acceleration in residential construction permits nationally would suggest expanding opportunity windows alongside selective geographic expansion or enhancements in build efficiencies documented during annual reviews [S1]. Cross-leveraging mortgage banking capabilities remains a tactical advantage enhancing customer retention through bundled services when compared with competitors lacking this vertical integration.

Continuous monitoring of policy changes affecting affordable housing initiatives or tax incentives could also present incremental upside if effectively capitalized upon.

Key Risks and Constraints: Mortgage Rates, Demand Sensitivity, and Market Volatility

Demand declines have been sharply correlated with rising mortgage rates that exacerbate buyer affordability challenges—the central risk outlined both in Q1 disclosures as well as prior annual risk reports [S2], [S1]. Persistent macroeconomic uncertainties including inflationary pressures may prolong elevated financing costs thus lengthening the recovery horizon.

Furthermore, inherent cyclicality governs new homebuilder revenues closely linked to housing start trends influenced by economic employment data and consumer confidence indices. Unexpected regulatory shifts imposing stricter environmental or labor standards could increase unit costs constraining margins if not offset by price adjustments.

Supply chain disruptions pose additional margin pressure risks given the reliance on timely deliveries of raw materials such as lumber and steel combined with skilled construction labor scarcity reported industry-wide.

Next Steps: What to Watch in Upcoming Quarters for Execution and Demand Signals

Key indicators warranting close attention following this first quarter include updates on order backlogs which will provide early directional clues on demand normalization or continued softness as reported alongside quarterly earnings ([S2]). Management guidance revisions—if forthcoming—may clarify outlooks against volatile financing environments.

Tracking mortgage rate movements remains essential since even small basis point adjustments influence buyer behavior materially as per recent market commentary ([N6]). Operational execution markers such as cost control effectiveness or announced land purchases might signal strategic shifts aiming to capitalize on anticipated market rebounds.

Stock market reactions post-earnings provide sentiment cues potentially reflecting broader investor positioning relative to homebuilding cyclicality ([N7], [N8]).

Brief Financial Context: Balance Sheet Strength and Profitability Snapshot

While near-term operating results suggest margin pressures from declining sales volume amid challenging external conditions, the firm's long-established liquidity buffer supports stability during cyclical troughs. Historically documented cash & equivalents positions approximated $2.8 billion at end-2020 per companyfacts data providing ample runway for working capital needs or opportunistic investments absent immediate refinancing concerns [F1].

Total debt levels appear modest relative to cash holdings indicating low net leverage structurally reducing financial distress risks even in downturn scenarios ([F1]). Net income figures around $198 million for Q1 indicate continuing core profitability despite top-line contractions mediated through prudent cost management strategies highlighted by management disclosures ([S2]).

This profile offers sufficient strategic optionality to navigate current headwinds while positioning for eventual cyclical upturns aligned with homebuyer demand reacceleration.

This analysis is based exclusively on disclosed SEC filings and credible industry news sources without any investment advice offered.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments