Natural Resource Partners LP Battles Persistent Market Glut and Shifts Distribution Strategy

Weak coal and soda ash markets have forced NRP to recalibrate distributions and make strategic capital investments amid continued oversupply.

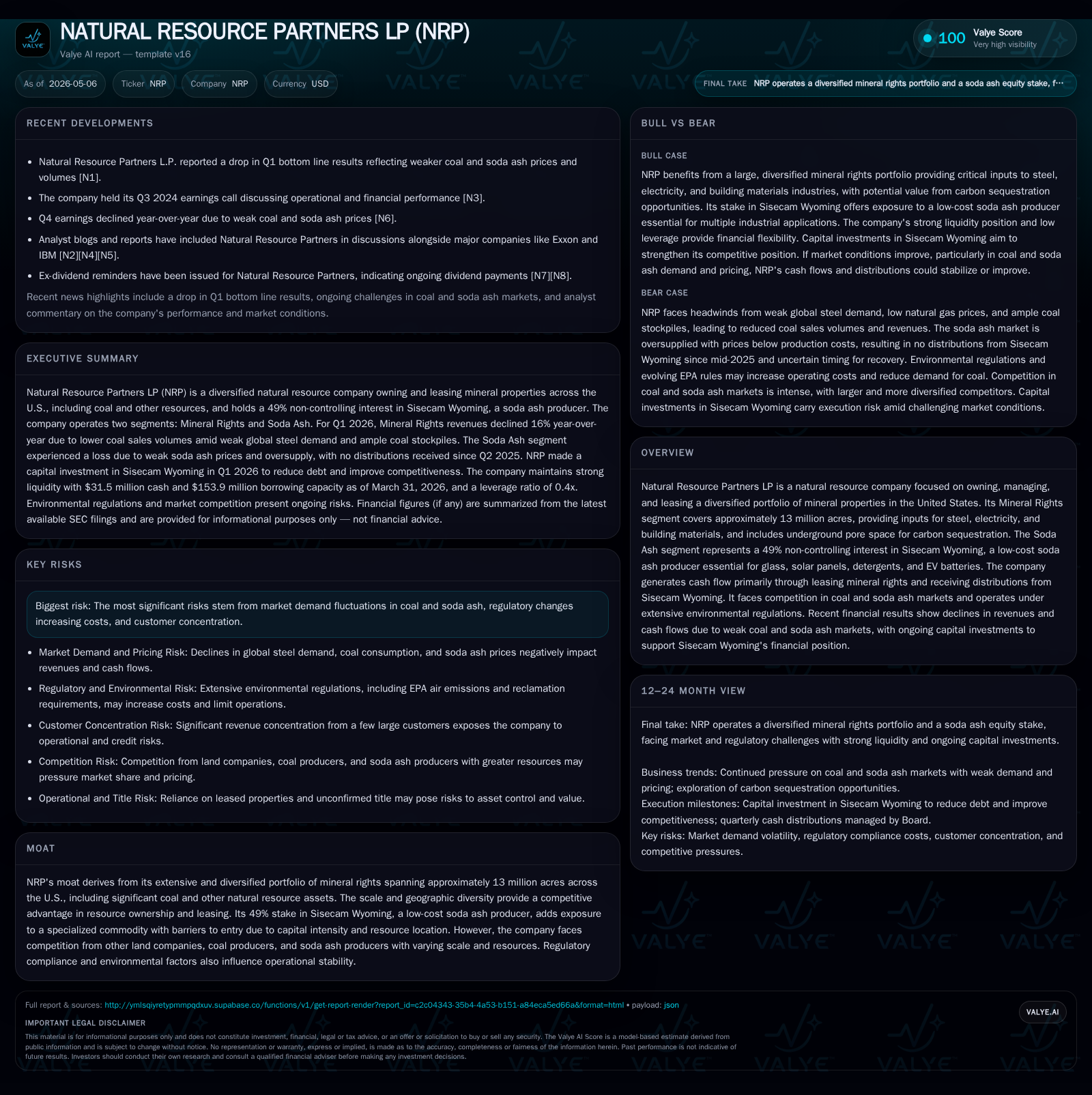

In its latest quarterly filing, Natural Resource Partners LP reported a decline in operating cash flow to $33.0 million for Q1 2026, heavily impacted by a prolonged oversupply in the soda ash market causing suspension of distributions from its Sisecam Wyoming investment. The company maintains liquidity of $185.4 million and a low leverage ratio of 0.4x, supported by a $39.2 million capital infusion into Sisecam Wyoming to stabilize credit. With mineral rights leasing revenues pressured by weak coal demand and international soda ash prices below production cost, NRP faces near-term cash flow headwinds but holds competitive advantages through its extensive acreage and diversified asset portfolio.

First Quarter Operating Update: Market Pressures and Capital Moves

Natural Resource Partners LP’s first quarter of 2026 reflects sustained headwinds stemming from commodity market weakness that have reshaped its near-term operating outlook and distribution strategy [S2]. The company generated operating cash flow of $33.0 million during Q1 but experienced a negative free cash flow of $5.4 million driven predominantly by a strategic $39.2 million capital investment into Sisecam Wyoming made alongside its managing partner. This infusion aimed to reduce debt under Sisecam Wyoming’s bank credit facility, positioning the joint venture better amid challenging conditions [S1], [S2].

A critical development disclosed is the absence of soda ash distributions received from Sisecam Wyoming since Q2 2025 due to an ongoing global oversupply that has pushed international soda ash prices below most producers’ cost of production with no short-term correction anticipated [S2]. This suspension marks a sharp departure from prior steady income streams tied to their non-controlling 49% investment.

Executives paid customary quarterly distributions including a $0.75 per common unit payment for Q4 2025 in February 2026, accompanied by a smaller special distribution intended to cover unitholder tax liabilities associated with ownership in 2025 [S2]. Going forward, distribution policies will shift to a discretionary quarterly determination considering profitability, available cash flow, debt service obligations, market outlooks, taxation factors, and reserve needs [S2]. This approach signals heightened uncertainty around predictable payouts.

Fundamental Business Model: Mineral Rights Leasing and Soda Ash Partnership

NRP's core business model pivots on owning about 13 million acres of mineral rights spanning key U.S. coal-producing regions, generating revenues primarily via long-term lease payments tied to underlying resource extraction activities [S1]. These leases provide overriding royalty interests on coal and other minerals like metallurgical coal used as essential inputs in steel manufacturing.

Lease payments depend on commodity prices realized by lessees who operate under intense market competition themselves, making royalty-based income vulnerable to external pricing pressure [S1]. Nevertheless, the company's expansive and geographically diverse acreage offers valuable scale advantages over smaller competitors or isolated holdings, underpinning its moat structure.

Complementing mineral rights exposure is the indirect participation via a non-controlling 49% stake in Sisecam Wyoming LLC — a trona mining and soda ash refining venture recognized for low production costs relative to other global players, [S1]. Soda ash is critical across various industrial applications including glass production, solar panels manufacturing, detergents formulation, and emerging EV battery components.

While this segment historically contributed meaningful cash distributions that supplement NRP’s overall cash flows, it currently contends with fundamental oversupply stemming from increased Chinese natural soda ash exports coupled with tepid flat glass demand worldwide [S2]. This dynamic constrains near-term revenue visibility despite the asset’s baseline cost advantage.

Industry Dynamics: Competitive Pressures, Regulatory Factors, and Commodity Cycles

The industries supporting NRP's operations are characterized by notable volatility reflecting commodity price sensitivity intertwined with cyclical end-market demand conditions.

Within coal leasing markets, competitiveness stems from both regional diversity of producers vying domestically and varying quality-price differentials influencing customer choice amidst alternatives like natural gas or renewables reducing thermal coal demand [S1]. The metallurgical coal subsegment also exposes the portfolio slightly more cyclically linked to global steel production levels.

Sisecam Wyoming operates within the capital-intensive global soda ash sector dominated by trona deposits whose extraction infrastructure creates high barriers to entry. Despite low-cost positioning within North America, competitive pressures escalate against large-scale incumbents in Europe and Asia with deeper pockets or integrated vertical presence. Notably, China's expanding export capacities exacerbate downstream pricing pressures globally.

Environmental regulation imposes additional constraints on operational flexibility especially concerning coal extraction activities where compliance costs can erode margins further [S1]. Meanwhile carbon capture initiatives exploring underground pore space utilization offer new regulatory-driven opportunities but presently contribute marginally.

Growth Drivers: Potential Catalysts Amid Challenging Markets

NRP’s medium-to-long term growth hinges on several contingent factors:

- Soda Ash Market Rationalization: Any consolidation or capacity curtailment among global producers could alleviate pricing pressure enhancing distributable profits from Sisecam Wyoming eventually [S2]. Advances in solar panel adoption or revived flat glass consumption could also stimulate demand.

- Mineral Lease Expansion: Incremental leases or lease renewals especially within metallurgical coal acreage may incrementally bolster base royalty revenue if steel industry activity gains momentum [S1].

- Carbon Sequestration Utilization: Leveraging underground pore space owned beneath mineral lands for carbon capture storage is an emerging potential catalyst supporting future diversified revenue streams.

Operational metrics such as resumption timing of Sisecam Wyoming distributions or upward inflections in mineral leasing royalties tied to commodity price recovery remain essential KPIs signaling potential inflection points.

Risk Factors and Operational Constraints

Several key risks temper the growth outlook:

- Prolonged Commodity Price Weakness: Extended depressed coal prices along with soda ash oversupply threaten sustained royalty revenue generation affecting distributable cash flows.

- Customer Concentration: Revenues significantly concentrated among customers like Alpha (coal customers) and Foresight intensify vulnerability should any key lessee reduce operations or default [S1].

- Regulatory Risks: Tightening environmental policies could elevate costs or restrict certain mining operations reducing asset utilization efficiency.

- Dependence on Managing Partner Alignment: Effective management of joint ventures such as Sisecam Wyoming depends heavily on partnership cooperation for capital calls or strategic decisions [S1].

- Reserve Estimation Limitations: Technical reserve data provided by third-party operators limit NRP’s independent verification capacity imposing some uncertainty over asset valuation robustness [S1].

Such constraints necessitate attentive monitoring of macroeconomic indicators alongside counterparty financial health.

Forward-Looking Indicators: Distribution Policy, Capital Spending, and Market Signals

Future operating visibility will be guided primarily by distribution policy updates announced each quarter by the Board considering updated financial results alongside commodity market developments [S2].

Capital deployment remains focused on sustaining core asset health with recent sizable contributions into Sisecam Wyoming aimed at credit quality preservation evidencing prudence against uncertain volume/margin trajectories.

Additionally monitoring principal debt repayments totaling roughly $14.3 million planned through 2026 is vital given ongoing fiscal discipline ensuring covenant adherence and liquidity maintenance [S2], [S1].

Market signals such as international soda ash pricing trends indicating supply-demand balance shifts or incremental recovery in U.S. and global metallurgical coal demand will act as early indicators influencing operational cadence.

Financial Overview: Liquidity Position and Debt Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $32mm | |

| 2026-03-31 | ||

| Total debt | $60mm | |

| 2026-03-31 | ||

| Net debt | $29mm | |

| 2026-03-31 | ||

| Current assets | $60mm | |

| 2026-03-31 | ||

| Current liabilities | $29mm | |

| 2026-03-31 | ||

| Current ratio | 2.09x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

NRP retains robust liquidity positioning entering Q2 2026 with total available resources amounting to $185.4 million composed of $31.5 million cash & equivalents plus $153.9 million undrawn borrowing capacity under the Opco Credit Facility [S2], [F1]. This buffer supports operational funding flexibility amid continued external pressures.

The leverage ratio stands conservatively at circa 0.4x as of quarter-end March 31, 2026 reflecting limited indebtedness relative to earnings capacity despite recent capital outlays focused on sustaining joint venture stability [S2], [F1].

Debt maturities including approximately $14.3 million remaining senior notes repayments across the remainder of the year align with manageable amortization schedules minimizing refinancing risks near term [S2], underscoring sound balance sheet stewardship despite volatile market backdrops.

| Metric | Amount (USD millions) |

|---|---|

| Cash & Equivalents | 31.5 |

| Available Borrowing Capacity | 153.9 |

| Total Liquidity | 185.4 |

| Total Debt | 60.4 |

| Net Debt | 28.9 |

| Leverage Ratio (Debt/EBITDA) | 0.4x |

This analysis is based exclusively on publicly available filings as of May 6, 2026 including SEC disclosures filed via Forms 10-Q (May 6), Annual Report Form 10-K (February 27), supplemental event Form 8-K (May 6), companyfacts XBRL data release (March quarter-end), and corroborating news sources referenced herein without extrapolation beyond verified data points. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments