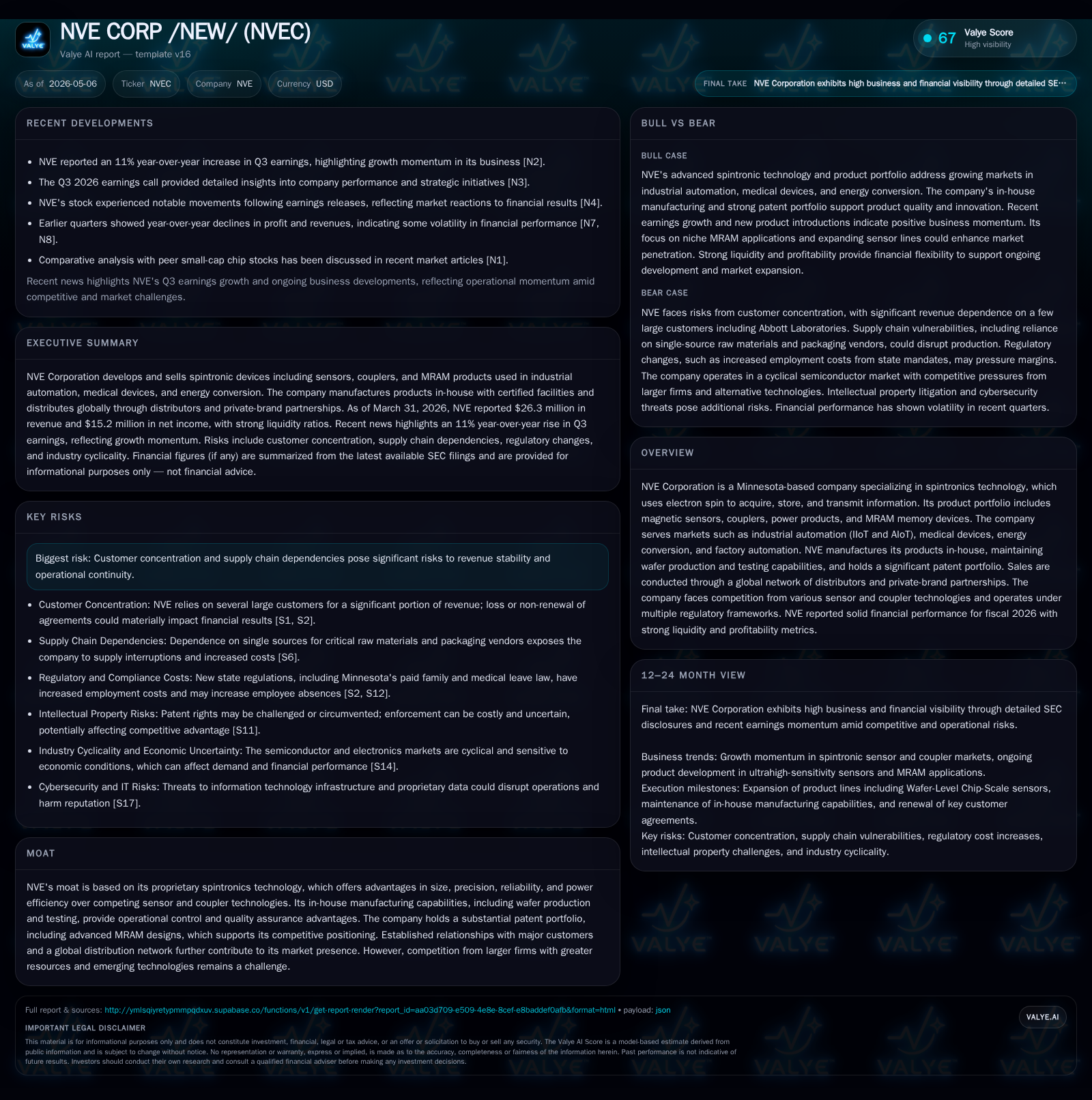

NVE Corporation Boosts Shareholder Value with Strong Fiscal 2026 and Strategic Dividend

NVE Corp delivers solid fiscal 2026 results and initiates a $1.00 quarterly dividend, underscoring financial strength amid supply chain and customer renewal risks.

In its latest 8-K filing, NVE Corporation announced fiscal year 2026 results demonstrating robust profitability and liquidity, accompanied by the initiation of a $1.00 per share quarterly dividend. The company’s proprietary spintronics technology underpins its competitive advantages in magnetic sensors, couplers, and MRAM memory devices, supporting growth in industrial automation, medical, and energy sectors. However, supply chain dependencies on single-source wafers and critical customers present risks that require monitoring. Upcoming contract renewal milestones and product development progress will be key demand markers to watch.

Latest Operating Update: Quarterly Results and Dividend Initiation

NVE Corporation took a decisive step to enhance shareholder value by announcing a quarterly cash dividend of $1.00 per share payable on May 29, 2026. This move was disclosed in the company’s May 6th 8-K filing alongside the fiscal year ended March 31, 2026 results [S3]. The dividend signals management's confidence in sustained cash generation capacity backed by a strong balance sheet.

The company reported revenue of approximately $26.3 million for FY26 with operating income at $15.9 million—manifesting healthy margins reflective of efficient operations within a niche technology arena [F1]. Net income stood at $15.2 million.

By approving this dividend following consecutive strong quarters including Q4 FY26 results reported earlier in January’s 10-Q [S2], NVE demonstrates commitment to returning capital without sacrificing investment in growth initiatives.

Business Model and Product Differentiation: The Role of Spintronics

At its core, NVE's business model exploits proprietary spintronics—a nanotechnology manipulating electron spin rather than conventional electron charge—to design magnetic sensors, couplers for data transmission, and MRAM memory solutions [S1]. Unlike traditional semiconductor products that rely on changes in voltage or current magnitude alone, spintronic devices sense magnetic states with far less power consumption and offer compact form factors.

Manufacturing is vertically integrated: NVE operates wafer fabrication cleanrooms with specialized equipment for depositing sub-five nanometer layers required to realize giant magnetoresistance (GMR) or tunneling magnetoresistance (TMR) effects foundational to its products [S13]. This control over critical front-end processing combined with back-end testing enables superior quality assurance compared to competitors outsourcing wafer production.

Revenue is generated primarily through sales of these high-performance devices via established global distributor networks servicing over 75 countries plus private-label partnerships with integrated device manufacturers which broaden market reach [S16][S13]. Key applications include position/speed detection in factory automation robots (IIoT/AIoT), energy-efficient isolated DC-to-DC converters for battery storage systems, and implantable medical sensing devices requiring unrivaled sensitivity and reliability.

Competitive Positioning Within the Magnetic Sensor and Coupler Industry

NVE sits within a competitive landscape populated by sensor producers offering Hall-effect or AMR sensors as well as alternative communication couplers such as optical or inductive variants [S26]. However, NVE emphasizes differentiation by leveraging its intellectual property portfolio exceeding 50 U.S. patents including advanced MRAM innovations like magnetothermal designs that rival traditional memory technologies on performance and tamper resistance grounds [S26].

The company's vertical manufacturing paradigm affords cost control benefits alongside quality advantages. This integration also supports rapid iteration cycles for next-generation product development—important given intensifying competition from better-funded rivals potentially eroding pricing power over time.

Global distribution through major players like Digi-Key complements direct customer channels while compliance with ISO standards bolsters credibility when bidding for high-specification industrial or medical contracts [S13][S16]. However, threats persist from competitors potentially narrowing NVE's performance gaps as market maturity drives price compression—a structural challenge ongoing in semiconductor-related niches.

Growth Drivers: Expanding Markets in IIoT, Medical, and Energy Efficiency

Demand for precision sensing underpins much of NVE’s growth thesis. Industrial factory automation continues accelerating adoption due to labor cost pressures and quality improvement needs globally—environments where reliable digital data pathways such as those provided by NVE’s couplers gain traction given their size efficiency and noise immunity properties. Likewise, the shift to smart connected devices boosts requirements for low-power magnetic sensors widely used in medical implants or portable diagnostic tools where longevity is paramount [S1].

Energy conversion markets represent another promising avenue where isolated DC-to-DC converters facilitating battery management systems are integral as electric vehicles and renewable integrations rise worldwide.

Moreover, MRAM remains a fledgling but potentially transformative segment offering nonvolatile memory options resistant to radiation or sabotage ideal for military-grade or industrial mission-critical applications—though broad market penetration still hinges on cost scaling improvements relative to CMOS technologies [S13].

NVE’s strategy to broaden sensor varieties including newly introduced angle rotation sensors and high-sensitivity TMR variants aligns directly with these expanding end-market requirements providing tangible near-term impetus to revenue streams [S16].

Risks and Constraints: Supply Chain Dependencies and Customer Concentration

Despite technological strengths, NVE’s operational continuity faces notable vulnerabilities stemming from supply chain concentration risks. The firm depends heavily on single-source suppliers for raw silicon wafers integral to wafer fabrication—a potential bottleneck compounded by geopolitical uncertainties affecting international logistics or tariff impositions [S1][S18]. Although some inventory buffers exist, alternative qualified sources remain limited making disruption scenarios impactful.

Packaging vendors present additional dependence constraints due to product-specific complexity involving unique magnetic characteristics limiting interchangeability among suppliers without costly qualification efforts [S1].

Customer concentration particularly around Abbott Laboratories—a major account governed by an agreement currently extended through December 31, 2027—poses revenue risk should renewal negotiations falter or demand decline materialize post-contract expiration [S2][S16]. While historical precedent shows continued shipments beyond prior agreement lapses are possible, formal renewal terms remain uncertain.

Furthermore, newly effective Minnesota state mandates for paid family leave increase employment cost structures with possible effects on labor availability cited explicitly in the January 2026 quarterly report as emerging operational headwinds affecting margins incrementally [S2].

Lastly, broader semiconductor industry cyclicality coupled with increasing competition from larger firms possessing deeper resources constrains pricing flexibility causing potential margin pressure if sustained competitive intensity intensifies [S15].

Strategic Outlook: Upcoming Milestones and Market Adoption Signals

Looking ahead into FY27 and beyond, key milestones revolve around product pipeline progress including next-generation ultralow power sensors targeting hearing aid markets plus enhanced MRAM offerings for anti-tamper applications being prioritized within ongoing R&D programs [S16][S1]. These innovations aim to secure incremental market share gains alongside expanding use cases.

Monitoring renewal outcomes of critical customer agreements —especially Abbott Laboratories’ supplier contract—will be paramount given their proportionate impact on revenue stability starting late calendar year 2027 horizon. Likewise, distributor relationship sustainment amid varying regional demand cycles remains pivotal.

Indicators such as rising orders for industrial automation components tied to IIoT deployments or successful qualification of novel sensor parts for implantable medical devices would act as leading signals validating growth strategy execution. Capex effectiveness in maintaining wafer fab competitiveness also bears watching since bottlenecks here could impair responsiveness relative to faster-moving competitors [S2][S1].

Continued legal diligence over intellectual property enforcement will be necessary given evolving infringement challenges customary within semiconductor tech sectors that indirectly influence competitive dynamics [S20].

Financial Snapshot: Liquidity, Profitability, and Capital Allocation

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1714040 | |

| 2026-03-31 | ||

| Current assets | $32mm | |

| 2026-03-31 | ||

| Current liabilities | $1141326 | |

| 2026-03-31 | ||

| Current ratio | 28.21x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD) | Period End |

|---|---|---|

| Revenue | 26.3 million | |

| 2026-03-31 | ||

| Operating Income | 15.9 million | |

| 2026-03-31 | ||

| Net Income | 15.2 million | |

| 2026-03-31 | ||

| Cash & Equivalents | 1.7 million | |

| 2026-03-31 | ||

| Current Assets | 32.2 million | |

| 2026-03-31 | ||

| Current Liabilities | 1.1 million | |

| 2026-03-31 | ||

| Current Ratio | 28.21x | |

| 2026-03-31 |

NVE’s financial foundation entering FY27 is notably sound; exceptionally high current ratio underscores ample short-term liquidity cushioning working capital needs while cash balances support dividend payouts without encroaching capital earmarked for R&D investments or operational sustenance [F1][S3]. Operating margins exceeding 60% reflect efficient cost management enabled partly by vertical integration advantages discussed earlier.

Capital allocation prudence is evident through initiation of dividends balanced against continuous technology development funding signaling deliberate shareholder value focus alongside long-term growth prioritization.

Disclaimer: This analysis is based on publicly filed SEC documents supplemented by sector expertise; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments