Polomar Health Services Struggles with Early-Stage Risks and Financial Strain

Recent contractual terminations and tight liquidity challenge Polomar Health’s growth ambitions in pharmaceutical compounding.

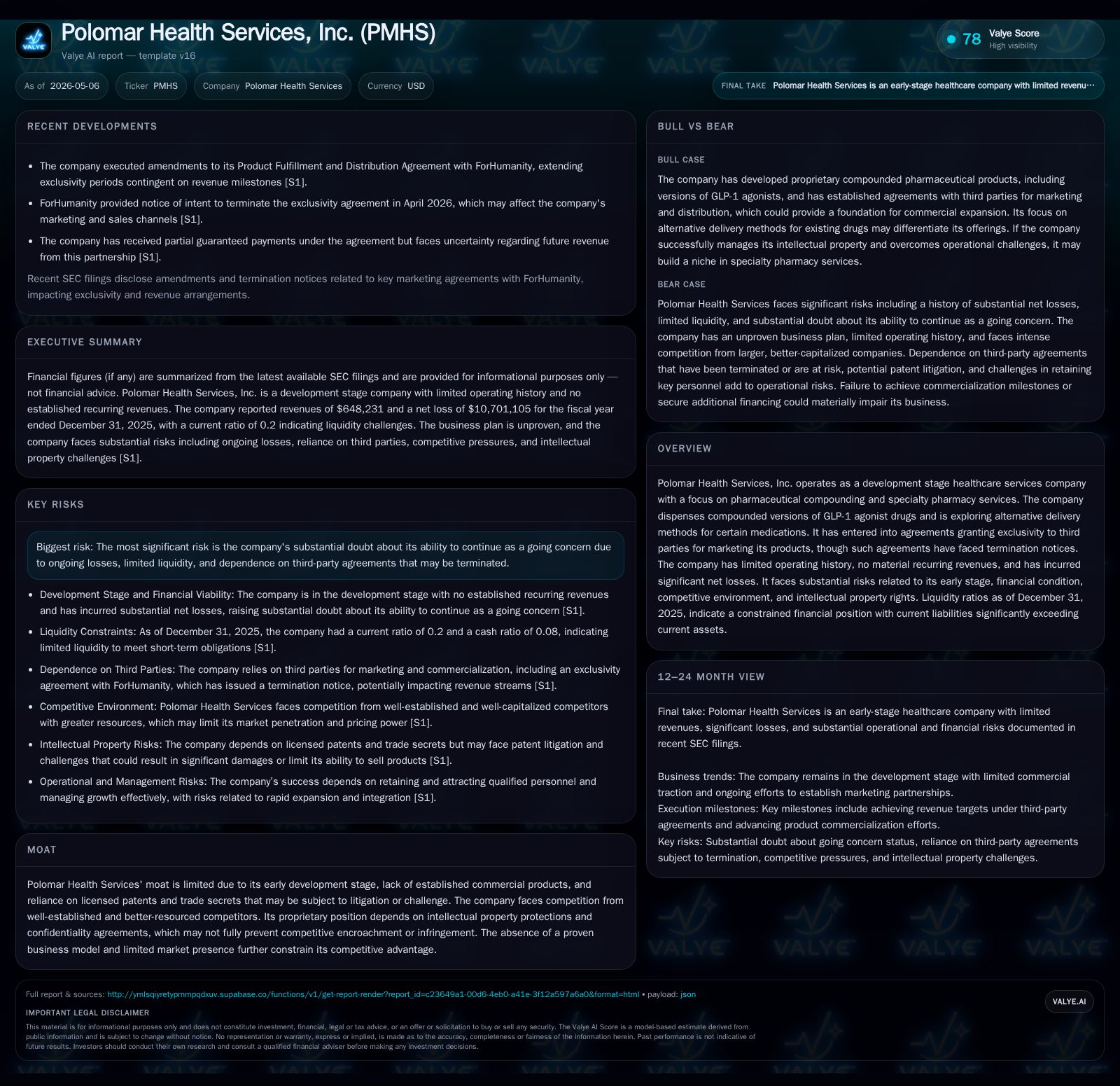

Polomar Health Services, a development-stage healthcare company focused on compounded GLP-1 agonists and specialty pharmacy services, recently saw the termination of a key fulfillment agreement and currently relies heavily on a licensing arrangement with ForHumanity for near-term revenue. The early-stage firm faces significant operational and financial constraints, including a low current ratio, high current liabilities, and recurring net losses exceeding $10 million. While it is exploring alternative drug delivery methods and potential licensing extensions contingent upon revenue milestones, its lack of scale, competitive pressures, and IP-related risks constrain its commercial viability and growth trajectory.

Recent Operating Developments: Contractual Shifts and Revenue Commitments

Polomar Health Services’ latest quarterly filing (10-Q dated November 25, 2025) coupled with the April 29, 2026 8-K event report reveal key near-term operating changes that materially affect its commercial prospects [S2][S3]. The company’s prior Product Fulfillment and Distribution Agreement with ForHumanity was terminated, a significant shift since this had been a primary distribution channel for its compounded pharmaceutical products. Despite this termination effective earlier in 2025 after multiple amendments, Polomar maintains an exclusivity licensing agreement granting ForHumanity sole rights to market its products through June 30, 2026.

This license comes with substantial contractual terms designed to underpin revenue flows: a guaranteed payment totaling $750,000 (of which half has been paid), conferring the initial exclusivity term of forty-two months subject to automatic renewals contingent on meeting defined gross revenue benchmarks [S3]. Specifically, ForHumanity can extend exclusivity through December 31, 2026 by delivering at least $1.75 million in gross revenue to Polomar during the first half of calendar year 2026. Further extensions obligate progressively higher revenue thresholds.

The termination of the fulfillment agreement represents a contraction in secured sales channels; however, the licensing deal’s design offsets this somewhat by tying exclusivity directly to ForHumanity’s performance. This structure effectively places future revenues — vital for the company’s survival — on meeting these external sales milestones.

Business Model and Product Portfolio: Compounded Drugs and Specialty Pharmacy

Drawing from the latest full annual filing (2026 form 10-K), Polomar operates as a developer of compounded pharmaceutical preparations focusing notably on GLP-1 agonist drugs [S1]. Such compounds represent an innovative corner within healthcare services where formulations are customized beyond mass-produced pharmaceuticals to meet specific patient needs or improve therapeutic profiles.

Besides compounding injectable GLP-1 analogs — drugs increasingly pivotal in diabetes management — the firm is exploring alternative delivery modalities intended to enhance patient compliance or expand indications. The business model primarily involves manufacturing these specialized compounds and dispensing them via specialty pharmacy services.

Revenue generation follows a licensing-centric framework whereby rights to market these compounded formulations can be exclusively granted to third parties (as exemplified by ForHumanity). Payments include upfront guaranteed fees plus ongoing royalties or milestone-based payments tied to sales volumes. This arrangement allows capital-light operations without direct marketing infrastructure but renders financial outcomes deeply dependent on licensees’ market execution.

Given its nascent commercial stage and limited recurring revenues reported so far, Polomar's business lacks established scale or diversified income streams. Margins remain heavily pressured by research investments, regulatory compliance costs related to compounding practices under FDA oversight nuances, and supply chain management for raw materials.

Competitive Environment: Early Stage Challenges in a Crowded Pharma Market

Polomar faces an intensely competitive landscape dominated by established pharmaceutical firms equipped with broad development pipelines, extensive marketing capabilities, and deep R&D resources [S1]. Its positioning is challenged by several structural disadvantages:

- First-mover access: Larger competitors have secured formulation patents or have vertically integrated specialty pharmacy divisions.

- Intellectual property fragility: Reliance on licensed patents combined with trade secret protections exposes Polomar to potential infringement disputes or patent invalidation risks.

- Scale disadvantages: Limited sales history curtails negotiating leverage across suppliers and distribution networks.

The specialty pharmacy sector itself is undergoing consolidation amid heightened regulatory scrutiny around compounding standards (USP <800>, FDA enforcement discretion clarifications) that pose entry barriers but also elevate compliance cost burdens for smaller players like Polomar.

Moreover, consumer adoption of compounded alternatives often requires overcoming physician prescribing inertia favoring branded GLP-1 products backed by large pharma advertising budgets. The emerging telemedicine interfaces utilized by licensees such as ForHumanity may facilitate broader reach but come with integration execution complexity.

Growth Drivers: Licensing Potential, New Delivery Methods, and Market Expansion

Key growth levers center on expanding commercial adoption via exclusive licensing partners meeting contractual revenue targets. The staged renewal design incentivizes licensees like ForHumanity to scale sales quickly while offering Polomar incremental exclusivity extensions up through mid-2027 assuming continual gross revenue achievement [S3][S26][S27].

Progress in alternative drug delivery exploration — referenced broadly in the annual disclosure — could diversify product offerings beyond injectable compounds to oral formulations or novel devices. These avenues may unlock larger patient populations or better adherence metrics.

Fundamental KPIs linked tightly to growth execution include:

- Gross revenues generated under licensing agreements,

- Renewal of exclusivity rights based on hitting $1.75M then up to $5M annual revenue thresholds,

- Introduction timelines for new delivery modalities,

- Expansion into complementary therapeutic segments within metabolic disorders.

Given the lack of direct marketing capacity internally, broader market penetration hinges critically on third-party licensees’ ability to deploy telemedicine networks effectively alongside pricing structures competitive against incumbent providers.

Risks and Constraints: Financial Stress, Contract Dependency, and IP Vulnerabilities

The company faces stark challenges tied to its continuation as a going concern given persistent net losses ($10.7 million loss reported for FY2025) and fragile liquidity reflected by a dangerously low current ratio of approximately 0.2 [F1][S1][S21]. Current liabilities surpass current assets by nearly fivefold ($1.6 million vs $323 thousand), exposing vulnerability to creditor pressures.

Contract dependency risk is acute since major near-term revenues derive from the relationship with ForHumanity. Termination notices alleging fraudulent inducement raise uncertainty over enforceability despite company assertions disputing these claims [S27]. Failure of this partner relationship would drastically reduce revenue inflows.

Additionally, intellectual property protections constitute another material risk vector. The firm relies heavily on licensed patents plus trade secret covenants vulnerable to legal challenge or circumvention [S10][S11]. Litigation outcomes are unpredictable but could impose substantial damages or operational injunctions impairing product commercialization.

Operational capacity limitations compound these effects given early-stage status lacking robust manufacturing scale or diverse distribution channels absent successful licensee partnerships.

What to Monitor Next: Revenue Milestones, Contract Renewals, and Liquidity Trends

Critical near-term indicators shaping Polomar’s outlook include:

- Whether ForHumanity achieves minimum gross revenues (~$1.75 million) during H1 2026 enabling extended exclusivity clauses through December 2026,

- Progress toward higher revenue milestones potentially extending partnership terms up through mid-2027,

- Updates regarding resolution of termination claims made by ForHumanity or any legal proceedings modifying contract terms,

- Regulatory approvals or public communications around new drug delivery technologies under development,

- Management hiring/retention status amid growth plans.

Tracking these execution points will illuminate whether contractual dependencies translate into tangible top-line improvement or if financial stressors intensify requiring capital raises or strategic pivots.

Latest Financial Overview: Cash Position, Liabilities, and Operating Losses

A concise snapshot from fiscal year-end December 31, 2025 underscores the precarious financial position facing Polomar Health Services [F1]:

| Metric | Latest Figure |

|---|---|

| Cash & Equivalents | $132,150 |

| Current Assets | $322,727 |

| Current Liabilities | $1,612,372 |

| Current Ratio | 0.2 |

| Operating Income | -$10,550,264 |

These figures chart difficult terrain with cash reserves insufficient compared to near-term payables obligations thus constraining flexibility for marketing expansion or R&D intensification without new funding sources. Operating income deficits reflect continuing investment phases typical for developmental-stage biopharma entities yet heighten existential questions absent rapid commercialization progress.

In sum, Polomar's strategy depends heavily on leveraging niche compounding expertise coupled with third-party marketing exclusives that condition future growth trajectories on external partners' ability to generate meaningful revenues amidst challenging competitive dynamics and internal financial vulnerabilities.

This analysis is based solely on publicly filed SEC documents as of May 2026 detailing Polomar Health Services’ operational developments and financial disclosures without recommending any investment action.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments