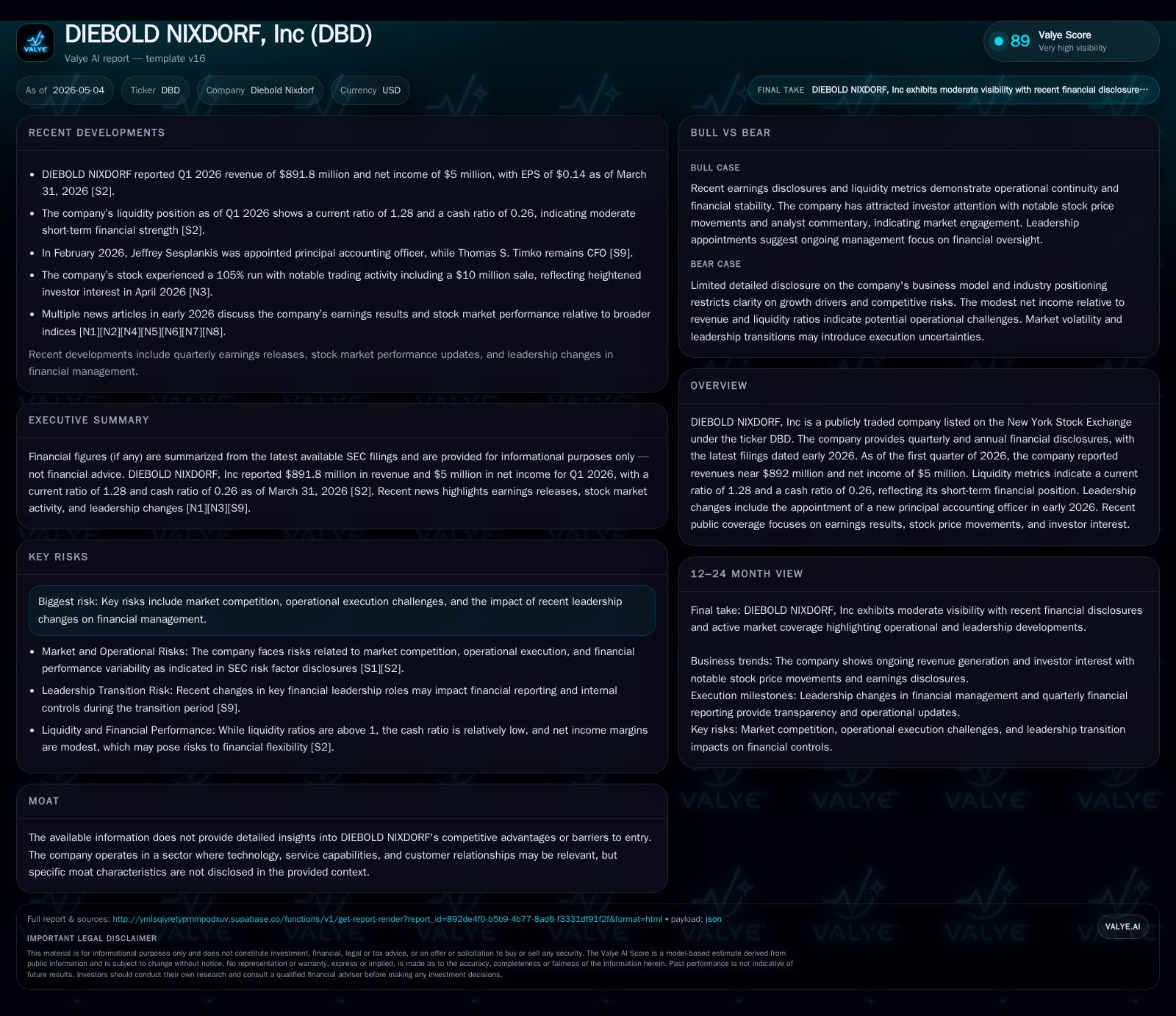

Diebold Nixdorf’s Q1 2026 Results Reveal Operational Headwinds and Strategic Shifts

The latest quarter highlights challenges in profitability despite stable liquidity, alongside leadership updates and strategic emphasis on software and services.

Diebold Nixdorf reported first-quarter 2026 revenues near $892 million with net income of $5 million, reflecting ongoing operational pressures amid competitive market dynamics. Liquidity remains adequate with a current ratio of 1.28, while a new principal accounting officer appointment underscores management's focus on financial discipline. The company's business model integrates hardware and software payment solutions with services targeted at banks and retailers, but commoditization of hardware and competitive fintech entrants constrain pricing power. Growth hinges on expanding digital service contracts and geographic reach, yet risks include operational execution and leverage levels limiting flexibility.

Q1 2026 Operating Update: Key Changes and Implications

Diebold Nixdorf’s first quarter of 2026 illustrates the ongoing balancing act between managing operational headwinds and repositioning its business strategically. The company reported revenue close to $892 million with net income narrowly positive at $5 million—a sign that while top-line activity persists, margin pressure remains acute in an evolving competitive landscape [S2], [F1]. Liquidity fundamentals appear solid; cash and equivalents ended the quarter at about $359 million with a current ratio of 1.28 signaling reasonable short-term asset coverage against liabilities [F1].

A notable corporate development during this period was the appointment of Jeffrey Sesplankis as principal accounting officer in February 2026, an internal reshuffling that retained Thomas Timko as CFO but points to a sharpened focus on robust financial governance amid transitional challenges [S9], [S3]. This leadership update suggests an intention to strengthen internal controls and accounting oversight that could support disciplined execution on growth initiatives.

These recent quarterly results must be contextualized within a framework of cautious optimism. The slim profit margin reflects cost pressures likely tied to competitive pricing in hardware sales combined with ongoing investment in software platform development and service capabilities.

Business Model and Product Offering: Payments Technology Meets Services

Diebold Nixdorf operates at the intersection of hardware manufacturing and financial technology services. Its business model pivots around the design, production, deployment, and servicing of automated teller machines (ATMs), integrated payment solutions, point-of-sale terminals, and related software platforms aimed primarily at banks and retail chains worldwide [S1].

The company employs a two-pronged revenue approach: upfront hardware sales supplemented by longer-term service contracts that offer managed maintenance and software subscriptions. This hybrid model partially offsets the commoditization trends in ATM sales by locking customers into ecosystem-based platforms that integrate device management with analytics-driven payment processing software.

Strategically, Diebold Nixdorf leans into delivering end-to-end solutions blending physical infrastructure with cloud-enabled services—a move intended to increase switching costs by embedding proprietary technology deeply into client operations. The recurring revenue stream from service contracts provides some margin stability amidst fluctuating hardware demand cycles.

Competitive Positioning Within the Financial Technology Industry

Within its sector niche encompassing payment systems providers for banking institutions and retailers, Diebold Nixdorf contends with a diverse set of competitors ranging from legacy industrial suppliers to nimble fintech startups offering purely digital payment alternatives [S1].

Hardware commoditization significantly restricts pricing power on ATMs as clients can source devices from multiple vendors globally. Thus, margins on this front are thin compared to what software licensing or long-term service contracts yield. Regulatory pressure encouraging digital payments adoption also introduces a paradox: while boosting demand for software platforms, it reduces cash use—and hence need for traditional ATM infrastructure.

Diebold Nixdorf's competitive edge lies in breadth of installed base coupled with expertise in integrating hardware/software solutions plus comprehensive service support—characteristics not easily replicated by fintech entrants focused solely on app-based or cloud-native payments.

Nonetheless, the competitive landscape enforces continuous innovation investment; retaining incumbents requires balancing cost efficiency with enhancements to platform functionality such as remote diagnostics or enhanced cyber security measures embedded within service contracts.

Drivers Shaping Growth Prospects in a Dynamic Market

Key growth opportunities center on accelerating adoption of Diebold Nixdorf’s software platforms that promote digital transformation in retail banking—transitioning customers toward full-service managed environments where analytics guide cash logistics or fraud prevention features add value beyond basic transactions [S2], [N1].

Service contract expansion is pivotal; gains here contribute more stable recurring revenues less susceptible to the cyclical fluctuations inherent in hardware orders. Geographic expansion into emerging markets where digital infrastructure investments accelerate also offers incremental upside.

Measured KPIs to watch include an increasing proportion of total revenue attributable to software platform penetration and extension or renewal rates on service agreements—signals that would validate customer retention strength alongside demand momentum for integrated solutions.

Continuous enhancements targeting user experience improvements (e.g., contactless payment integration) also underpin the firm’s ability to maintain relevance amidst evolving consumer expectations.

Risks and Constraints Facing Execution and Profitability

Despite some positive demand drivers, several risks loom large over Diebold Nixdorf's path forward. Intense competition compresses hardware margins while compelling ongoing R&D expenditures increase cost bases without guaranteed commercial success [S8], [S14]. Leadership transitions within finance functions could temporarily unsettle execution rhythm even as they aim to strengthen discipline long term [S9].

Leverage remains considerable; net debt stands near $607 million given total debt approximating $966 million less cash balances around $359 million, potentially constraining capital flexibility needed for innovation investments or opportunistic acquisitions that might enhance competitive positioning [F1].

Regulatory landscapes governing payment technologies impose compliance burdens; any adverse changes could disrupt deployment timelines or increase costs. Further threat emerges from accelerating fintech disruption that may undercut traditional ATM reliance more rapidly than anticipated.

Upcoming Milestones and What Investors Should Monitor

Looking ahead, key milestones include execution fidelity on announced product launches enhancing software capabilities, tangible progress in service contract renewals reflecting customer satisfaction levels, and early indicators from new management initiatives targeting operational turnaround efforts documented during earnings calls and filings [N1], [S2], [S3].

Investor attention should also track updates related to geographic expansion initiatives which may open fresh revenue pools if successfully penetrated.

Monitoring guidance revisions or adjusted forecasts will provide further clues about market reception to strategic shifts as well as the company’s agility confronting ongoing industry upheaval.

Latest Financial Snapshot: Summary of Liquidity, Debt, and Profitability

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $359mm | |

| 2026-03-31 | ||

| Current assets | $1800mm | |

| 2026-03-31 | ||

| Current liabilities | $1404mm | |

| 2026-03-31 | ||

| Current ratio | 1.28x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This snapshot reaffirms a fundamental picture where liquidity buffers absorb short-term uncertainties but subdued profitability coupled with meaningful leverage requires careful management prioritizing enhanced operational efficiency over aggressive growth spending at this juncture.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available SEC filings and news sources as cited. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments