Ring Energy Confronts Liquidity Pressures Despite Operational Focus in Q1 2026

Ring Energy's latest quarter reveals ongoing liquidity challenges alongside management initiatives to stabilize operations amid sector volatility.

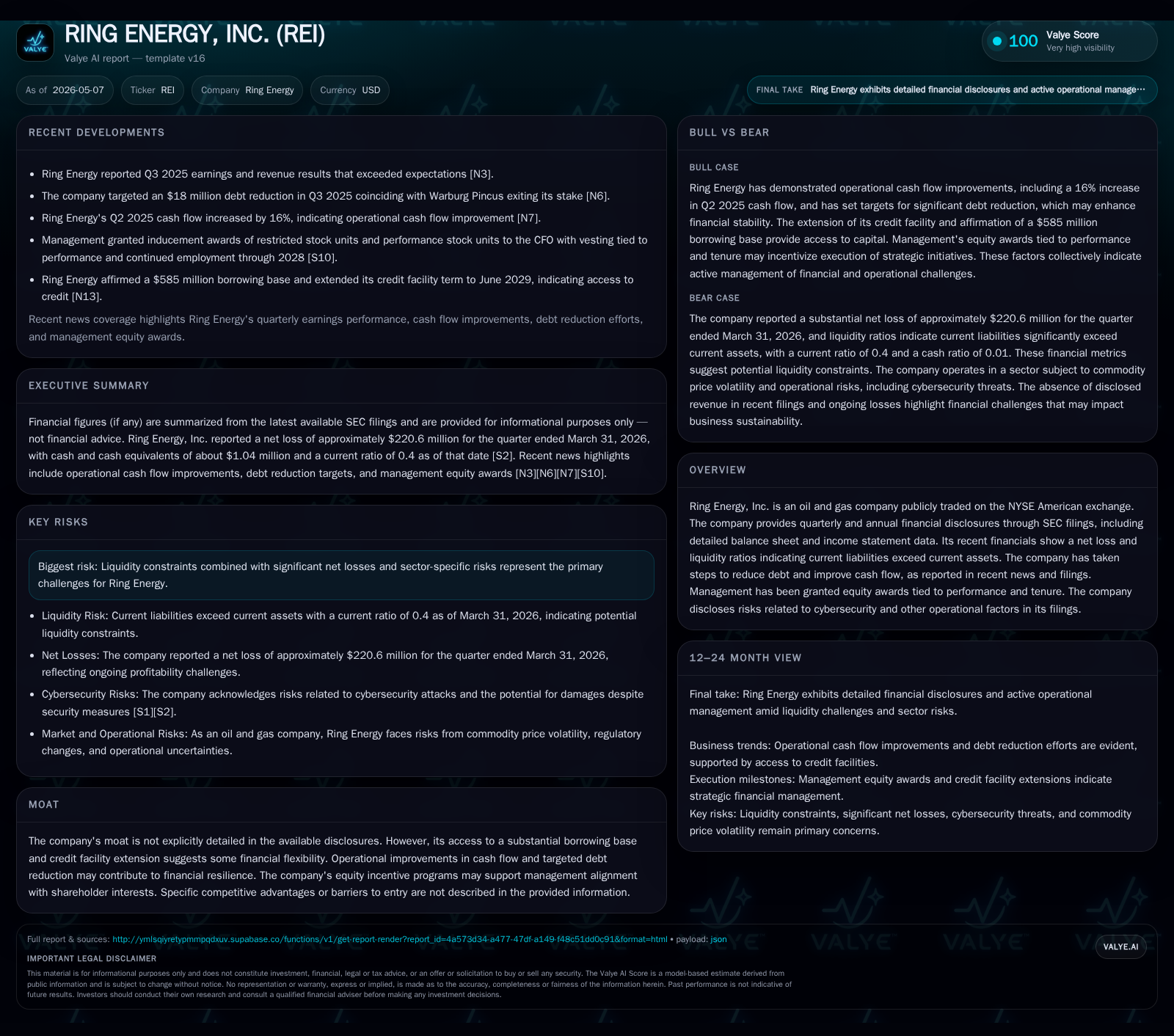

In its Q1 2026 filing, Ring Energy reported continued financial strain characterized by a low current ratio and net losses, yet management has executed actions targeting cash flow enhancements and debt reduction. The company’s core business remains anchored in oil and gas production, but it faces significant industry headwinds including commodity price volatility and narrow financial flexibility. Equity-based performance incentives signal a push for operational discipline. Key risks include liquidity constraints and cybersecurity exposures, while growth hinges on efficient asset utilization and capital structure management.

Latest Quarterly Operating Update and Why It Matters

Ring Energy’s Q1 2026 Form 10-Q filing dated May 6 reveals ongoing liquidity stress with $59 million in current assets against $148 million in current liabilities, delivering a notably weak current ratio of approximately 0.4 [S2], [F1]. Despite holding zero reported long-term or total debt per the latest available balance sheet metrics, the company's meager cash position — about $1 million — constrains operational flexibility [F1]. This predominantly working-capital imbalance underscores tight short-term financial conditions.

The filing details management's focus on mitigating these pressures through cost control and enhanced cash flow management strategies. Concurrently, the company granted equity inducements comprising restricted stock units (RSUs) and performance stock units (PSUs) to its newly appointed Executive Vice President and Chief Financial Officer as part of a long-term incentive plan designed to tether leadership compensation to measurable results through 2028 [S23], [S24]. These awards reflect an effort to foster alignment with shareholder interests amid a challenging operating environment.

The immediate significance lies in Ring Energy’s attempt to navigate near-term liquidity constraints without fresh leverage while signaling a governance strategy emphasizing performance accountability. However, persistent net operating losses highlight fragility in returning to profitability at current operational scales.

Business Model and Product Quality Assessment

Ring Energy operates primarily as an upstream energy company engaged in crude oil exploration and production activities. Revenue flows stem from selling produced hydrocarbons into commodity markets; however, reported top-line figures have shown a prolonged absence of meaningful revenue generation as evidenced by the latest period data indicating nil revenue recognized at least since mid-2011 [F1]. This lack of revenue recognition suggests either asset shuttering or minimal production volumes materially impacting top-line intake.

The company's asset base involves significant capital equipment deployed for extraction activities, requiring ongoing investment to maintain production capacity given natural depletion rates typical in oil fields. Operating income and net income data from recent years confirm sustained losses, likely tied to both market headwinds like depressed oil prices during certain intervals and inherent fixed costs burdening scalability [S1], [S4].

Economically, margins appear constrained without evidence of proprietary technology or differentiated resource bases that would confer significant competitive advantage or pricing power. Contractual arrangements tend toward spot sales or short-tenor agreements typical in onshore independent operators.

Industry Context and Competitive Standing

Ring Energy participates in a competitively dense US oil & gas sector marked by pronounced cyclicality due to commodity price fluctuations driven by macroeconomic factors and geopolitical events. The company faces direct pressure from larger integrated peers benefiting from better capital access, diversified portfolios, and economies of scale. Recent peer earnings reports such as Devon Energy (DVN) and Northern Oil & Gas (NOG) show better-than-expected profitability enabled by scale efficiencies and hedging programs that partially insulate against price swings [N1], [N2].

Ring Energy’s disclosures do not identify a clear moat or differentiated advantage beyond operational footprint; reliance on a borrowing base supported credit facility provides some financial runway but limited liquidity reflects tighter covenant capacity or reduced lender appetite given loss patterns disclosed previously [S1], [S3]. Furthermore, regulatory compliance costs and cybersecurity risk exposures represent ongoing headwinds that can intermittently disrupt operations or add unplanned expenditures [S7], [S29].

The industry supply chain complexities—including volatile labor costs, equipment availability constraints post-pandemic era supply challenges—further complicate upstream operator execution precision.

Growth Catalysts and Strategic Opportunities

In the absence of clear volume expansion or major acquisitions revealed recently, growth prospects hinge on improved operational efficiency gains reflected through tighter capital allocation discipline evident from management’s incentive-linked RSU/PSU programs awarded early 2026 targeted at aligning executive priorities with shareholder returns over three years[S23],[S24].

Operationally, streamlined cost structures aim at enhancing free cash flow generation which may create incremental optionality for reinvestment or debt reduction actions[S2],[S3]. Additionally, portfolio rationalization via divestitures or selective drilling could optimize asset quality though no explicit plans have been outlined recently.

Commodity market rebounds remain an exogenous factor capable of enhancing realized pricing, thus elevating throughput economics especially if combined with derivative hedging policies updated in presentations last quarter[S3],[S11].

Risks, Challenges, and Financial Constraints

Chief among risks is the stark liquidity mismatch apparent as the firm carries nearly triple the amount of current liabilities versus current assets[F1],[S2]. This raises solvency concerns absent substantial capital injections or restructuring moves. Ongoing net losses exacerbate erosion of retained capital buffers limiting turnaround runway[S2],[F1].

On operational dimensions, cybersecurity vulnerabilities acknowledged within filings imply potential for material disruptions or information security breaches which could impair financials directly via remediation costs or indirectly through reputational damage[S7],[S29].

Commodity price volatility remains perennial risk given dependency on external market forces beyond company control. Additionally, potential regulatory changes heighten compliance uncertainty especially as governmental policies evolve around carbon emissions regulation impacting upstream activities[S7],.

Investor Watchlist: Upcoming Milestones and Signals

Investors should track Ring Energy’s forthcoming quarterly filings to gauge progress on cash flow stabilization amid existing negative equity trends[S2],[S3]. Any announcements on restructuring initiatives or refinancing transactions would be notable triggers indicating strategic shift.

Key performance indicators such as reserve replacement ratios, production volumes if reported distinctly will be critical markers of operational health alongside any updates on derivative hedge positions which could moderate commodity price impacts[S3],[S11]. Management commentary around debtor negotiations or credit facility amendments could preempt liquidity inflection points.

Peer comparative performance especially dividends or share repurchase signals within US independent E&P space also contextualizes Ring Energy’s positioning across broad market cycles[N1],[N2].

Financial Snapshot: Current Balance Sheet and Liquidity Analysis

Data as of March 31, 2026 reveals acute working capital strain despite absence of outstanding debt[S2],[F1]. Although holding no recorded total debt eliminates interest burden risk currently[F1], the cash runway implied by this balance sheet necessitates rapid improvement in operational cash generation for sustainable solvency.

These figures underpin significant near-term financial risk despite management’s recent actions aimed at alignment incentives and streamlining expenditure.

Disclaimer: This report is prepared solely for informational purposes based on publicly filed SEC documents and news sources as of May 2026. It does not constitute investment advice or recommendations regarding securities. Readers should conduct independent analysis before making investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments