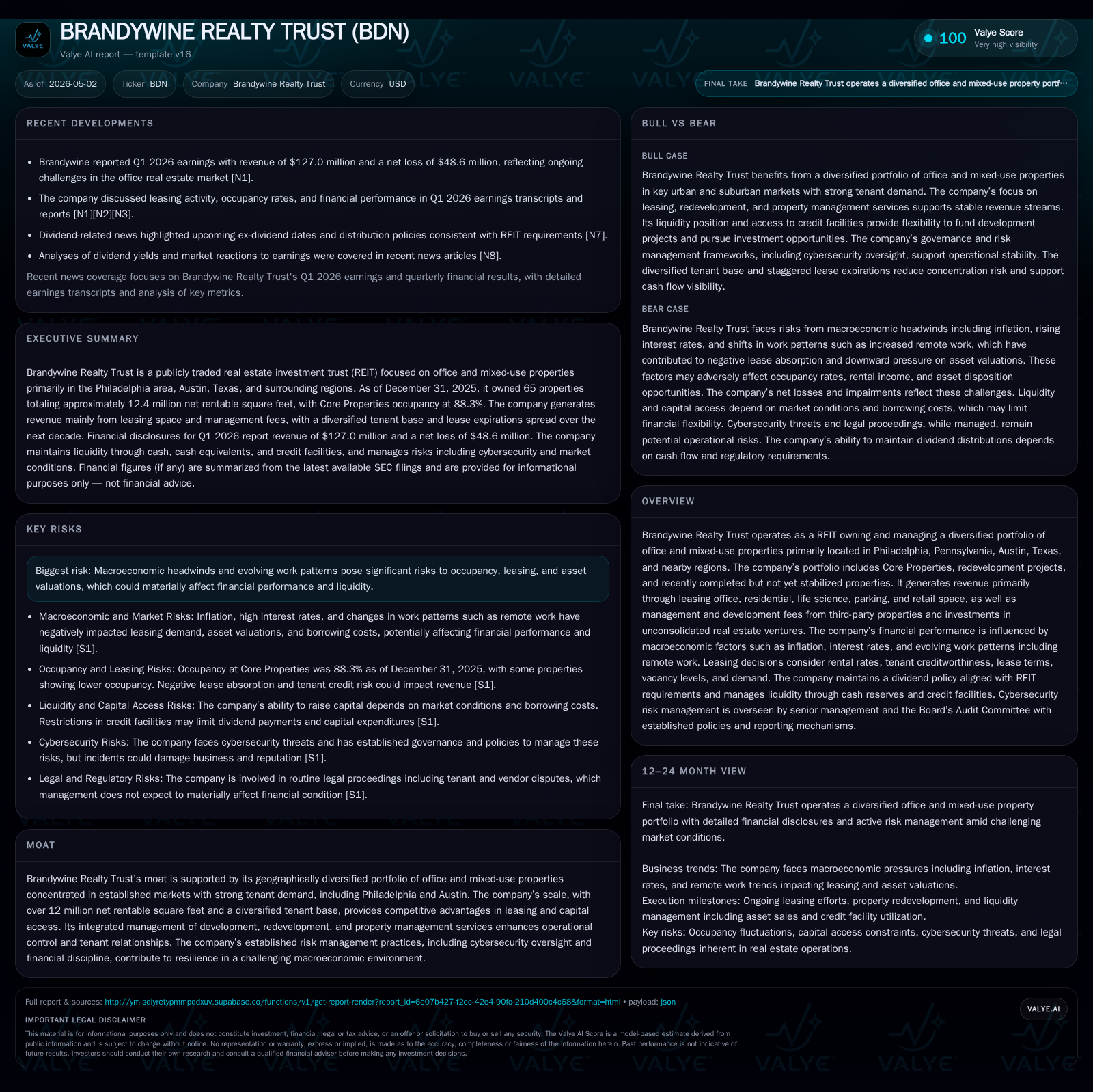

Brandywine Realty’s Portfolio Depth and Leasing Dynamics Define Its 2026 Growth Outlook

Brandywine Realty Trust’s latest quarterly filing reveals stabilizing occupancy amidst market pressures, supported by redevelopment initiatives and diversified leasing in core cities.

In Q1 2026, Brandywine Realty Trust reported a stabilization in occupancy rates with incremental leasing momentum in its Philadelphia and Austin properties, underscoring the resilience of its geographically focused portfolio. The REIT’s business model leverages a diversified asset base including office, life science, residential, and retail spaces, supplemented by fee income from property management and development services. While macroeconomic headwinds such as inflation and shifts in office usage remain challenges, Brandywine’s ongoing redevelopment projects and disciplined lease structuring support its growth trajectory. Close attention to lease renewals, stabilization of newly completed assets, and maintaining financial covenant compliance will be key near-term milestones.

Q1 2026 Operating Update Highlights

Brandywine Realty Trust’s latest Form 10-Q for the quarter ended March 31, 2026 [S2] indicates occupancy levels holding steady following a period of active leasing efforts during late 2025. While precise updated occupancy rates are not explicitly called out in the filing text extraction, narrative from accompanying earnings transcripts [N1, N2] clarifies that the company has made incremental progress on leasing newly completed but not yet stabilized properties.

Specifically, Brandywine emphasized continued demand within its core Philadelphia Central Business District (CBD) assets such as Cira Centre alongside absorption gains in Austin’s life science clusters. New leases and renewals have contributed to improved rental rate realization reflective of favorable credit quality among tenants. Management commentary reveals an ongoing balancing act managing inflation-related cost pressures while adapting leasing strategies to accommodate hybrid work patterns which continue to moderate office utilization demand.

The company continues to highlight the impact of macroeconomic factors—particularly inflation and elevated interest rates—as material considerations shaping short-term portfolio performance. Expense pass-through provisions embedded within most leases partially mitigate inflation risk; however, operating margins have experienced compression due to non-recoverable expenses [S1]. Notably, some properties remain in lease-up phases post recent completions or redevelopments creating temporary drag on overall occupancy metrics.

Core Business Model and Asset Quality

Brandywine Realty's business model centers on ownership and management of approximately 11.3 million net rentable square feet spanning office buildings and mixed-use complexes concentrated primarily in Philadelphia, Austin, and surrounding regions [S1]. The asset base includes stabilized Core Properties—primarily office-focused—with incremental contributions from residential units within mixed-use projects.

Revenue streams predominantly derive from leasing office space paired with ancillary residential, retail, parking facilities, and life science lab environments. Complementing this are recurring fees from third-party property management contracts and development or redevelopment service engagements. Investments in unconsolidated real estate ventures provide additional albeit minority income streams.

The lease portfolio is characterized by a high degree of diversification both across property types and tenant profiles. Around 97% of leases incorporate fixed or CPI-indexed annual rent escalations supporting price stability over time [S1]. Lease terms typically range across multi-year horizons with creditworthy tenants balancing turnover risk against rental rate resets.

Operationally, Brandywine benefits from integrated capabilities encompassing property management, redevelopment expertise, concession management, and capital deployment flexibility. This vertical integration facilitates tighter control over project timelines as well as tenant relationship management—a critical advantage amid a shifting office landscape marked by remote work adoption.

Competitive Landscape and Market Positioning

Brandywine’s geographic focus places it squarely within well-established market hubs that are driving resilient demand for quality offices: Philadelphia CBD commands premium rents due to limited new supply coupled with strong institutional tenant presence; Austin benefits from pronounced tech-sector expansion catalyzing life science growth segments.

Scale advantages emerge as Brandywine controls over 12 million net rentable sq ft (including ventures), allowing for portfolio-level risk dispersion as well as negotiation leverage in lease structuring and capital sourcing. The company’s ‘last mile’ local presence paired with sizable footprint enables tailored leasing solutions enhancing tenant retention rates compared to smaller regional landlords.

Barrier-to-entry factors include high replacement costs confronting new entrants seeking comparable locations paired with requisite expertise managing complex mixed-use developments integrating multiple asset types. Additionally, Brandywine’s underwriting rigor emphasizing tenant creditworthiness mitigates revenue volatility risks prevalent in cyclical downturns or when working through vacancy absorption periods.

Growth Drivers: Leasing Momentum, Redevelopment, and Fee Income

Key growth vectors revealed in recent filings [S2,S3] include:

- Leasing Absorption: Stabilization of several recently completed but unleased properties should incrementally support both revenue growth and margin improvement once occupancy thresholds are sustainably exceeded.

- Redevelopment Pipeline: Active redevelopment projects extend asset life-cycle values through modernization efforts enhancing building efficiencies aligned with ESG priorities such as energy reductions financed partly via C-PACE loans (e.g., $50.5 million loan at 3151 Market Street) [S16].

- Fee Income Expansion: Third-party property management contracts generate steady fee income less sensitive to occupancy cycles providing earnings diversification.

- Mixed-Use Diversification: Residential components within certain assets add cash flow stability given differing demand dynamics relative to pure office spaces.

Combined effect is expected to gradually underpin rental rate growth potential while cushioning downside from broader economic headwinds or changing workplace preferences.

Risks and Operational Challenges Ahead

Significant risks persist including:

- Macroeconomic Headwinds: Inflationary pressures elevate operational expenses beyond recovery thresholds despite lease structures; interest rate volatility increases borrowing costs impacting net spreads [S1].

- Office Demand Shifts: Hybrid work trends continue reducing space requirements per worker leading to longer re-leasing cycles or concessions needed to retain tenants.

- Tenant Credit Risk: Potential default or delayed payments can cause short-term liquidity stress especially if concentrated among larger tenants impacting leasing revenue line.

- Liquidity & Capital Structure: The company reported total debt of approximately $2.63 billion and cash & equivalents of about $36 million as of March 31, 2026 [F1].

Management commentary during investor calls around these timelines will be critical indicators of execution pace against strategic objectives.

Latest Financial Snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $36mm | |

| 2026-03-31 | ||

| Total debt | $2.6bn | |

| 2026-03-31 | ||

| Net debt | $2.6bn | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Cash & Equivalents | $36,203,000 | March 31, 2026 |

| Total Debt | $2,628,948,000 | March 31, 2026 |

| Net Debt | $2,592,745,000 | March 31, 2026 |

This snapshot underscores a sizeable debt load relative to liquid assets typical for REITs heavily invested in real estate operations requiring ongoing capital expenditures. The narrow cash buffer accentuates the importance of consistent operating cash flow generation alongside proactive refinancing strategies to maintain financial flexibility.

This analysis presents an operationally grounded perspective on Brandywine Realty Trust based strictly on SEC disclosures including Q1 2026 quarterly filing supported by recent public earnings commentary without speculative assertions. It highlights the interplay between portfolio composition, market dynamics, and macroeconomic influences shaping the company's near-term performance outlook while noting financially relevant balance sheet parameters.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments