Mobilicom Ltd Expands Design Wins and SaaS Ambitions Amid Persistent Losses

Mobilicom pursues scaling its end-to-end drone and robotics solutions with growing revenue but widening net losses.

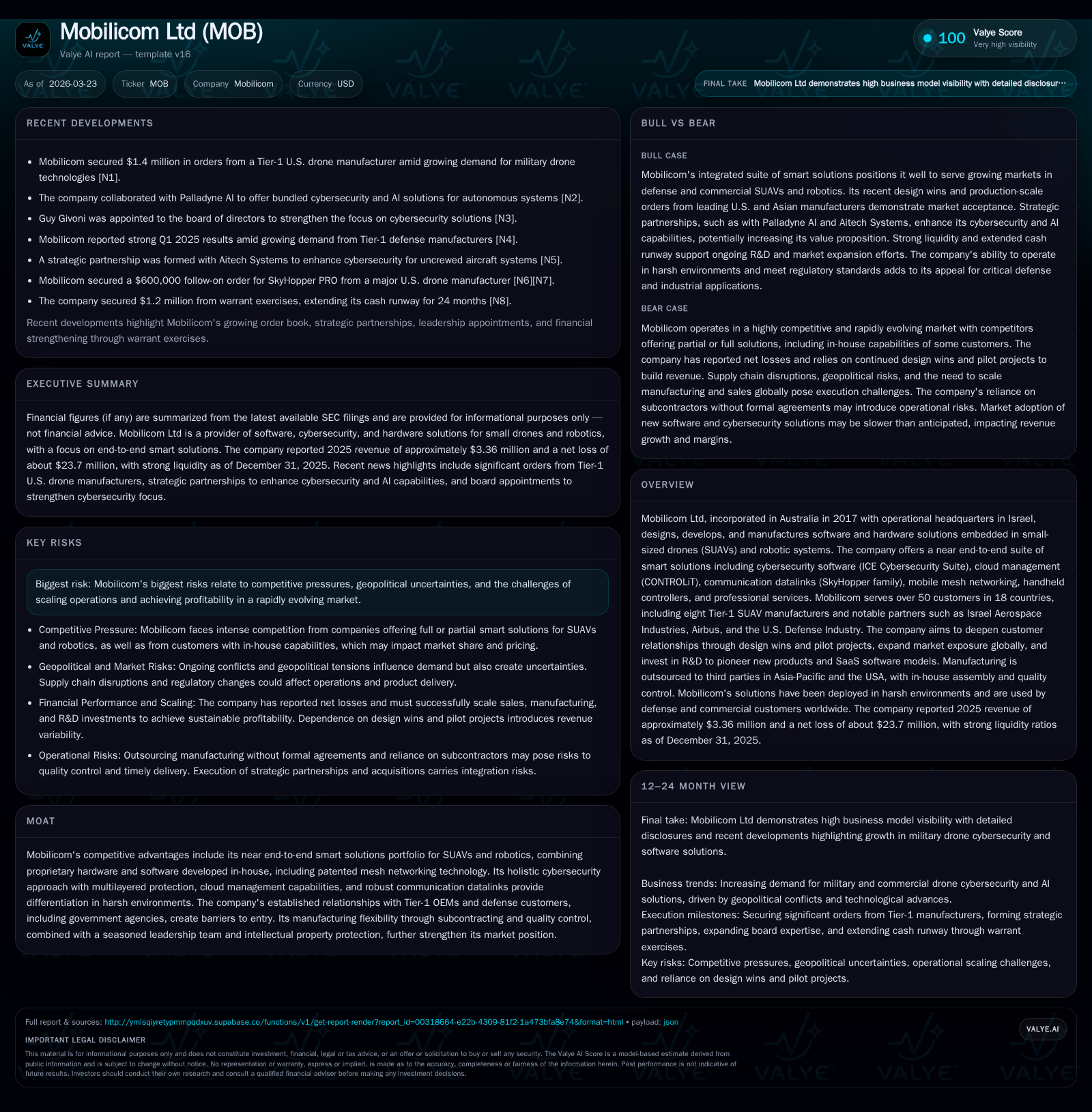

Mobilicom Ltd, an Australian-incorporated company operating primarily from Israel, develops integrated software and hardware for small drones and robotics, targeting defense and commercial sectors. The firm has seen steady revenue growth reaching $3.36 million in 2025 but continues to report substantial net losses exceeding $23 million, driven by heavy investment in R&D and expansion efforts. Its competitive moat is anchored in proprietary mesh networking technology, comprehensive cybersecurity suites, and relationships with Tier-1 SUAV OEMs. Future growth hinges on increasing design wins, scaling production through outsourced manufacturing, and transitioning toward SaaS models, yet profitability remains elusive amid intense competitive and geopolitical pressures.

Company Overview

Mobilicom Ltd operates at the confluence of the emerging small unmanned aerial vehicles (SUAVs) and robotics markets, providing an integrated portfolio of software and hardware solutions designed primarily for embedding into these systems. Although incorporated in Australia in 2017, Mobilicom's operational headquarters are situated in Israel—a global hub for defense technology innovation. Mobilicom’s product suite spans cybersecurity software (ICE Cybersecurity Suite), cloud network management (CONTROLiT), communication datalinks (SkyHopper family), mobile mesh networking units, handheld ground control stations, and professional services supporting operations.

The firm's customer base includes over 50 clients across 18 countries with significant penetration among eight Tier-1 SUAV manufacturers. Notable partners consist of Israel Aerospace Industries, Airbus, the U.S. Defense Industry, Rafael Technologies, ST Engineering among others [S9][S10].

Historical Financial Performance

Mobilicom's revenue trajectory over the past four years demonstrates consistent growth: from approximately USD 1.58 million in FY2022 rising to about USD 3.36 million by FY2025 [F1]. This represents a compound annual growth rate near 38%, fueled by increased deployment of products alongside expanded global marketing efforts.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 3 | -24 | +5.8% | -196.2% |

| 2024 | 3 | -8 | +40.8% | -70.4% |

| 2023 | 2 | -5 | +42.9% | |

| 2022 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -268.9 |

| 2024 | -198.9 |

| 2023 | -60.7 |

| 2022 |

Source: SEC companyfacts cache [F1].

*Note: Net income shown for FY2023 uses latest available data; exact figure may vary.

Despite revenue growth averaging nearly +5.8% year-over-year between FY2024 and FY2025 [F1], net losses expanded significantly due to sustained operating expenses emphasizing research & development (R&D), sales expansion initiatives and administrative costs. The net loss surged by nearly 196% year-over-year to approximately USD -23.7 million in FY2025 [F1]. This highlights ongoing investment stages rather than scalable profitability.

Equity declined from approximately $12.1 million at end-2022 to about $8.8 million at end-2025 reflecting capital consumption consistent with growth efforts [F1]. The company's current ratio remains robust above 8x as of end-2025 ($20.2m current assets vs $2.4m liabilities), supported by cash & equivalents totaling around USD $19 million [F1], indicating a manageable liquidity position.

Products and Technology Differentiation

Mobilicom positions itself as a near end-to-end solutions provider for SUAVs/robotics systems—integrating key subsystems that traditionally might be sourced separately:

- ICE Cybersecurity Suite: A multilayered automated security framework protecting drone platforms at device/communication/data levels in real time.

- CONTROLiT Cloud Management: Centralized fleet/network monitoring enabling device configuration oversight and live operational mapping.

- SkyHopper Datalink Family: Robust bi-directional data transmission supporting line-of-sight (LOS) / non-line-of-sight (NLOS) networks optimized for urban environments.

- Mobile Mesh Networking Units (MCUs): Enabling redundant communications within drone fleets or swarms critical for high-reliability deployments.

- Handheld Controller Systems: Ruggedized ground control stations supporting multi-payload operation tailored for flexible field uses.

- Professional Services: Integrated logistics support covering onsite/remote maintenance and safety assurance [S9][S14][S26].

A cornerstone differentiator is Mobilicom’s patented mesh networking modem technology protected under multiple US patents granted for unique coordination methods ensuring interference mitigation—a critical advantage when operating dense interconnected fleets [S18]. The company emphasizes operation durability under harsh environmental conditions frequently encountered in defense or industrial applications.

Competitive Positioning & Moat

The market Mobilicom addresses is characterized by rapid innovation cycles with players ranging from narrow component suppliers to large conglomerates offering complete UAV platforms. Three competitor archetypes challenge its position:

- Companies aspiring also to be end-to-end system integrators (e.g., UXV Technologies).

- Specialized providers addressing segments like cybersecurity (SkyGrid), cloud management (Auterion AG), datalinks (Silvus Technologies), or handheld controls (Kuta).

- Customers developing internally competing solutions (e.g., AeroVironment Inc., Elbit Systems).

Mobilicom claims differentiation through its broad portfolio enabling bundle sales improving system integration efficiencies leading to superior performance with reduced time-to-market and competitive pricing advantages [S5][S18]. Its deep engagement with leading Israeli defense contractors lends credibility through field-proven deployments ‘in the field’ with the Israeli Ministry of Defense [S7].

Its flexible manufacturing model—outsourcing assembly while retaining quality control supplemented by subcontractors across Asia-Pacific region and USA—supports scalability without heavy fixed asset commitments [S4].

Growth Drivers & Strategy

Mobilicom’s strategy centers on expanding its design wins—the adoption of their components embedded within customers’ UAV/robotics products—and pilot projects which serve as stepping stones towards volume orders. Success here should ramp recurring revenues as embedded systems become certified locally and marketed further downstream [S9]. Cross-selling across its product sets leverages these anchor relationships.

Geographically the company aims to build on its strong Israeli base while accelerating market access across the U.S., Europe and Asia via enhanced sales force presence along with marketing campaigns including trade shows & webinars [S9].

Research & development remains fundamental; Mobilicom invests heavily aiming to pioneer next-generation SaaS-based control platforms enhancing autonomous capabilities through partnerships such as with Palladyne AI Corp for neuro-symbolic AI integration announced mid-2025 [S10][S22].

New product launches like the SkyHopper Multiband datalink released early 2026 demonstrate continual update capabilities critical for communication reliability.

Capital Allocation & Financial Health

The firm’s balance sheet shows substantial equity erosion due to accumulated losses (-$23.7M net loss vs $8.8M equity translating into approximate -269% ROE in FY25) yet retains solid liquidity with over $19 million cash on hand enabling ongoing operations [F1][S17].

Capital expenditures remain modest (~$37k spent on fixed assets in FY25 mainly lab equipment) financed internally without reliance on debt indicating cautious capex stance aligned with early commercial ramp-up [S6][S11].

No dividends or share repurchases have been declared; capital allocation priorities focus on R&D reinvestment and scaling go-to-market capabilities essential for long-term value creation [S12][S20].

Notably, the December 2025 reverse stock split consolidated shares—from approximately one ADS representing 275 ordinary shares to one ADS representing one ordinary share—to improve share price stability ahead of Nasdaq Capital Market listing augmenting visibility and tradability [S6][S20].

Risks & Challenges

Key risks include intense competition from specialized vendors as well as customers' internal development capabilities [S15][S21]. Geopolitical instability may impact supply chains or government procurement budgets critical for defense applications [S15]. Regulatory export controls such as ITAR impose complex compliance burdens potentially limiting market access despite current certifications obtained [S15]. Cybersecurity threats remain material risks despite internal vigilance overseen by senior leadership; a breach could damage reputation given platform security claims [S21]. Scaling operational infrastructure efficiently without diluting quality standards challenges the young organization.

Outlook & What To Watch

While explicit formal guidance is not provided recently,the company highlights several indicators worth monitoring:

- Expansion pace of design wins becoming volume production orders particularly among U.S., European Tier-1 OEM customers.

- Growth trajectory of software/SaaS revenues from ICE Cybersecurity Suite and CONTROLiT cloud offerings shifting margin profile positively.

- Procurement of additional certifications or governmental approvals facilitating broader international deployments.

- Progression toward profitability through operating leverage improvements from scaled manufacturing agreements.

- Strategic partnerships or acquisitions augmenting product/service footprint enhancing end-to-end solution completeness. If Mobilicom successfully converts pilot projects into commercial traction while managing costs prudently it could signal inflection points toward sustainable growth phases.

Conclusion

Mobilicom Ltd stands out within the growing small drone/robotics ecosystem owing to its broad technologically integrated offerings combining patented communications networks with holistic cybersecurity layers delivered alongside versatile hardware platforms. The balance sheet shows financial strain due to current heavy investments but healthy liquidity cushions operations during this foundational growth stage. The ability to scale design wins internationally while navigating complex regulatory landscapes coupled with successful SaaS business model maturation will be critical pivots shaping its future trajectory amid challenging competition.

This analysis integrates publicly available disclosures reflecting detailed financial filings up to fiscal year-end December 31, 2025 without extrapolation beyond confirmed data points.[F1][S#]

Disclaimer: This report is intended solely for informational purposes based on available data without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments