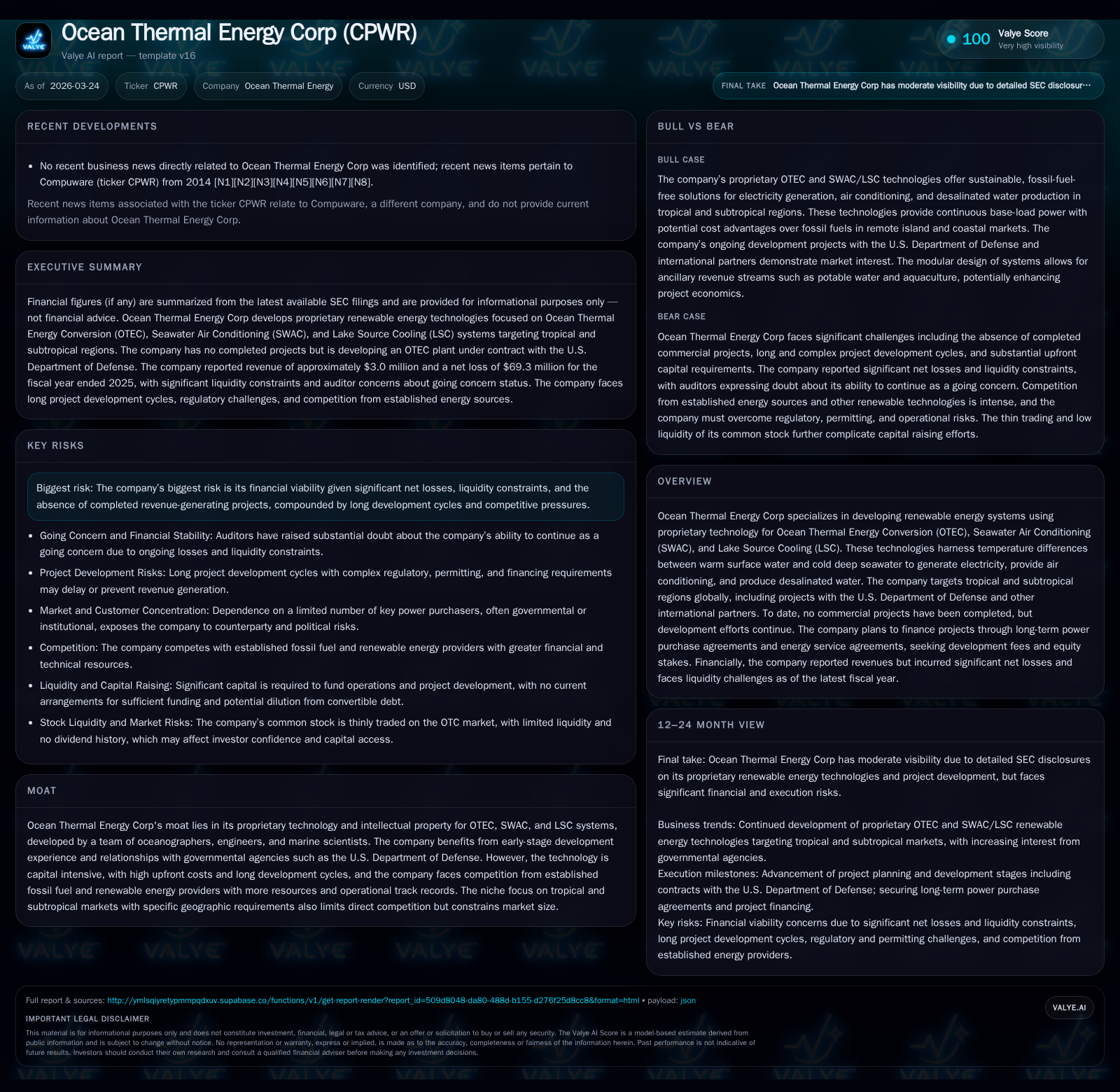

Ocean Thermal Energy Corp's Financial Struggle and Technology Promise in Emerging Renewables

The company pursues commercialization of proprietary ocean thermal energy conversion technologies while grappling with severe liquidity constraints and extended project development timelines.

Ocean Thermal Energy Corp (CPWR) operates in a niche renewable energy segment focused on harnessing ocean temperature differentials for power, cooling, and desalination. Despite pioneering proprietary technologies like OTEC, SWAC, and LSC targeted at tropical and subtropical markets—including U.S. military installations—the company has yet to finalize a commercial project. Financially, CPWR recorded its first revenues in FY2025 but continues to show deep net losses and critical liquidity challenges, underscoring capital dependency. The $3.6 million U.S. Army contract represents a proof-of-concept milestone; however, successful negotiation of long-term power purchase agreements remains uncertain. Capital intensity and long development cycles present ongoing risks against a competitive renewable energy backdrop.

Proprietary Ocean Technologies and Market Focus

Ocean Thermal Energy Corp’s core value proposition revolves around the commercial application of Ocean Thermal Energy Conversion (OTEC), alongside Seawater Air Conditioning (SWAC) and Lake Source Cooling (LSC) technologies [S1][S4][S6]. These systems exploit the natural temperature gradient between warm surface seawater and cold deep water—typically at depths of about 3,000 feet—to generate electricity, provide efficient air conditioning, and desalinate water without reliance on fossil fuels.

Their proprietary technology suite was developed by an in-house team of oceanographers, marine engineers, and scientists specializing in this unique marine energy niche [S1]. The company targets tropical and subtropical regions globally where year-round temperature differentials exceed 20 degrees Celsius—conditions essential for OTEC viability [S24]. CPWR aims at institutional clients including governments, utilities, large resorts, hospitals, educational facilities, and notably the U.S. Department of Defense whose bases in the Asia-Pacific region are strategic candidates for energy independence using sustainable sources [S1][S20].

Unique components such as large-diameter deep-water intake pipes sourced primarily from specialized manufacturers in the U.S. and Norway and cutting-edge heat exchangers constitute the technological moat that raises barriers to entry [S9]. Furthermore, their registered trademark TOO DEEP® exemplifies integrated intellectual property rights covering design concepts through economic modeling [S6]. This specialization limits direct competition but confines addressable markets to specific geographies consistent with ocean temperature profiles.

Historical Performance: Revenue Emergence Amid Staggering Losses

Reflecting the pre-commercial status of its technology stack and projects under development—with no operational plants generating power or other outputs—CPWR’s financial profile over recent years evidences substantial investment phases resulting in sizable losses offsetting nascent revenues.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -69 | -93395 | -172103 | -5747.0% |

| 2024 | -1 | -562627 | -1576610 | |

| 2022 | -7 | -327213 | -1518607 | -158.8% |

| 2021 | -3 | -542630 | -1981881 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 61.1 |

| 2024 | 2.7 |

| 2022 | 19.1 |

| 2021 | 8.9 |

Source: SEC companyfacts cache [F1].

Numbers from [F1]

Starting from zero revenue during FY2017 through FY2024 due to lack of operating plants—typical for capital-intensive renewables at early development—the company recorded approximately $3 million revenue in FY2025 stemming largely from contracts such as the U.S. Army engagement discussed below [F1][S7]. Operating income improved dramatically but remained negative by nearly $172k; however net income deteriorated sharply reflecting substantial non-cash charges like asset impairments or financing costs totaling over $69 million [F1]. Operating cash flow remains negative though improving year-over-year indicating continued burn subsidized by external funding.

These results underscore the long gestation period required before breakeven plant operation; CPWR’s present financial state characterizes a technology developer yet to cross into commercial revenue generation.

Project Development Pipeline and Contractual Positioning with U.S. Military

One prominent tangible contract spanning engineering design and financial feasibility work is the $3.6 million Small Business Innovation Research (SBIR) agreement with the U.S. Army via Johnson Controls Government Systems [S1][S7]. This effort focuses on formulating a comprehensive Basis of Design for an OTEC plant at a remote South Pacific military installation.

This engagement serves triple purposes: validating OTEC technological concepts within rigorous military standards; refining potential commercial models targeting base-load sustainable electricity combined with desalinated water supply; and establishing a strategic platform potentially leading to long-term Power Purchase Agreements spanning 25-30 years [S1][S7]. However, CPWR cautions no assurance exists that such PPAs will be successfully negotiated or signed.

Beyond this contract are exploratory discussions with other government agencies underscoring international footholds but absent binding commitments [S1]. The protracted sales cycles typical in large-scale infrastructure projects combined with political/regulatory complexities extend timelines.

Capital Structure, Liquidity Pressures, and Financing Dependencies

The company’s balance sheet exhibits acute financial stress threatening continuity absent fresh capital infusion [F1][S7][S10]. As of FY2025 end:

- Current assets totaled roughly $1.48 million contrasted starkly against current liabilities exceeding $114.8 million resulting in an alarmingly low current ratio near 0.01.

- Shareholders’ equity plunged into deep negatives around minus $113 million indicating extensive accumulated losses outweighing assets.

- Convertible debts tied to legacy financing arrangements pose dilution risks if converted to common stock.

Management acknowledges reliance on external equity or debt issuances with no assurances of successful capital raises amidst thin trading liquidity on OTC markets [S7][S16][S22]. Recent settlements with creditors such as DCO Energy over unpaid loans illustrate ongoing covenant pressures that require cautious cash management [S8].

This precarious position places considerable uncertainty on continuation without restructuring or new partnerships extending runway.

Project Economics: Cost Structure, Capacity Factor, and Pricing Model

CPWR details high capital intensity associated with OTEC projects reflective of novel marine engineering efforts [S5][S4]:

- A representative 20-MW OTEC facility carries an estimated construction cost around $445 million comprising approximately $301 million hard costs related to power system equipment including deep-water pipe installation (

68%) plus $144 million soft costs including design fees & permits (32%). - SWAC/LSC projects have somewhat lower budgets approximating $150 million per plant but require similarly thorough design/permitting steps.

- Plants anticipate a capacity factor near 95%, implying near-continuous full operation aside from scheduled maintenance every five years; notably higher reliability compared to typical ~90% factors seen in fossil-fuel generating plants due to simpler mechanical systems without fuel combustion complexity [S5][S12].

Revenue models emphasize two main streams:

- Development fees pegged roughly at 3% of total project costs payable upon successful closing of project financing.

- Long-term contract revenues via either energy-only pricing per kilowatt-hour or hybrid arrangements including monthly capacity payments combined with consumption-based charges over contracts typically lasting between two to three decades [S4][S12].

Additional upside may derive from ancillary outputs such as desalinated freshwater production supporting agriculture/fish farming industries especially critical in target tropical regions where potable water scarcity exists.

Risks from Long Development Cycles and Competitive Renewable Landscape

CPWR faces multifaceted risks detailed extensively by management auditors [S3][S8], chief among them:

- Lengthy multi-year project development cycles encompassing site identification through permitting requests materially delay revenue realization timelines even upon securing initial contracts.

- Technological disruption risk remains potent given fast-paced advances in renewables such as solar PV improvements or battery storage cost declines potentially offering lower-cost alternatives.

- Regulatory permitting hurdles vary widely across jurisdictions adding complexity plus environmental stakeholder opposition may surface given scale/sensitivity of marine ecosystem interactions.

- Competitors include entrenched fossil fuel generators enjoying established infrastructure plus larger renewable developers benefiting from government incentives/scaled project execution capabilities limiting CPWR’s market share growth potential outside its targeted niche.

- Auditor emphasis on going concern highlights existential threat requiring sustained capital access to avoid shutdowns.

Moreover geopolitical volatility especially stemming from unstable emerging markets complicates operational predictability alongside material contractual counterparty credit risk due to limited diversification in individual plant off-takers [S19][S24].

Evaluating Potential Returns: Forecasts, Milestones, and Investment Hurdles

Explicit financial forecasts remain unpublished beyond recent contract milestones; prospective investors must monitor key developmental signposts referenced by management including feasibility study completions for military projects or demonstration plants achieved through SBIR contract phases [S1][S4].

Returns hinge substantially on executing Power Purchase Agreements cementing stable revenue streams over extensive lives coupled with maintaining majority equity stakes (~51%) enabling upside participation beyond upfront fees [S12]. However absence of operational plants precludes meaningful assessment of internal rates of return until commissioning succeeds.

ROE calculated from latest annual net income (-$69M) over shareholders' equity (-$113M) suggests approximate return measure near 61%, though this reflects accounting losses rather than profitability consistent with developmental status [F1].

Strategic Outlook: What To Watch in Financing and Project Commercialization

Going forward critical milestones encompass:

- Securing additional working capital through equity issuance or structured partnerships tailored to unlock sustainable development funding given current liquidity shortages [S7][S22].

- Advancement through regulatory approval pipelines across multiple jurisdictions signaling tangible readiness for physical construction deployments.

- Formalizing long-term PPAs or ESAs anchoring revenue models particularly via governmental entities stepping into renewable procurement mandates.

- Technological validation through pilot plant success measures reinforcing credibility versus incumbent energy sources subject to pricing volatility impacts detailed below.

In summary Ocean Thermal Energy Corp embodies the juncture faced by frontier renewable developers balancing transformative technical promise against stark financial fragility amid intense competitive dynamics. Sustained investor patience dependent on meaningful contract closures coupled with incremental technical-commercial successes will shape ultimate viability prospects.

This report is prepared solely for informational purposes based on available public disclosures without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments