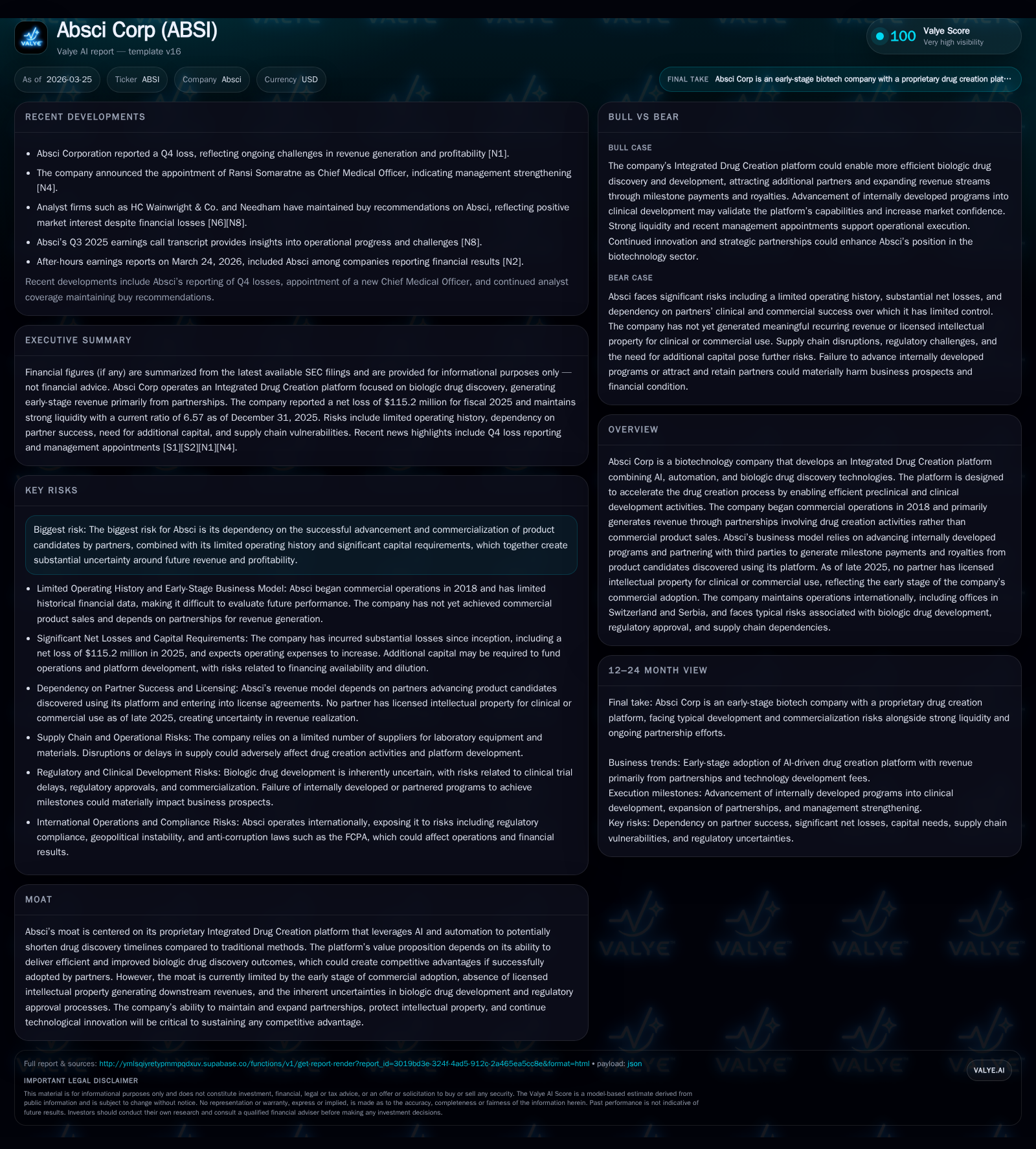

Absci Corp’s AI-Powered Drug Creation Platform Spurs Early Growth Amid Clinical Stage Challenges

Absci leverages AI-driven biologic discovery to accelerate pipeline development while confronting early-stage commercialization and financial strain.

Absci Corp employs a proprietary Integrated Drug Creation platform combining AI and automation to expedite biologic drug discovery, focusing on underexplored targets with high unmet need. Since commercial operations began in 2018, growth has been driven primarily by partnerships rather than product sales, leading to revenues plateauing below $6 million annually amid increasing R&D expenses. The lead candidate ABS-201 is advancing through Phase 1/2a trials for androgenetic alopecia with interim data expected in H2 2026, alongside plans for a Phase 2 trial in endometriosis. Absci faces significant operating losses exceeding $115 million in 2025, heavy cash burn, and absence of royalties from licensed products, underscoring challenges in translating platform innovation into sustainable profitability. Critical upcoming milestones center on clinical readouts and partner engagements that could validate the platform’s commercial potential.

Accelerated Growth Through Platform Innovation: Historical Financial Performance and Key Drivers

Absci Corp entered commercial operations in 2018 offering an integrated drug creation platform that synthesizes AI-powered generative design with automated lab-in-the-loop validation to expedite biologic drug development. This innovative approach targets molecular design efficiencies well beyond conventional timelines—advancing preclinical programs from concept to Investigational New Drug (IND) filing within approximately two years at a fraction of industry-average costs [S1].

However, revenue generation remains tethered largely to service-based partnerships providing technology development fees rather than product royalties or sales. As a result, top-line growth has been relatively flat but pressured recently due to clients' adoption pace.

The historic financials reveal a declining revenue trajectory with $5.7 million recognized in FY2023 down to $4.5 million by FY2024—a 20.7% year-over-year decline [F1]. Meanwhile, operating losses have deepened each year given escalating investments into internally developed programs and platform expansion: operating losses increased from approximately $106.8 million in FY2022 to $120.3 million in FY2025 [F1]. Net income mirrored this trend with losses exceeding $115 million most recently.

Negative operating cash flow persists at -$92.9 million for FY2025 alongside modest capital expenditures relative to total spending ($1.1 million capex), reflecting prioritization of R&D over physical asset build-out [F1]. These dynamics underscore the infancy of commercial adoption juxtaposed against aggressive innovation spend.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -115 | -93 | -120 | -11.7% | ||

| 2024 | 5 | -103 | -72 | -109 | -20.7% | +6.7% |

| 2023 | 6 | -111 | -65 | -116 | -0.5% | -5.4% |

| 2022 | 6 | -105 | -81 | -107 | +20.2% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -94 | -60.8 |

| 2024 | -73 | -57.6 |

| 2023 | -65 | -62.8 |

| 2022 | -98 | -38.2 |

Source: SEC companyfacts cache [F1].

Note: Revenue shown only where available; several years reflect modest revenue consistent with collaboration fees.

Clinical Advancements and Pipeline Development: Status of Internal Programs and Strategic Implications

Absci’s clinical-stage identity solidifies around ABS-201—an anti-prolactin receptor (PRLR) monoclonal antibody engineered for extended half-life enabling patient-friendly dosing intervals [S1]. The PRLR target is notably underexplored yet mechanistically promising for diseases lacking disease-modifying options.

ABS-201 is concurrently being developed for androgenetic alopecia (AGA) and endometriosis:

The HEADLINE™ Phase 1/2a trial (NCT07317544) addressing AGA has completed dosing initial single ascending dose cohorts demonstrating favorable safety thus far [S1]. Interim proof-of-concept data including exploratory efficacy endpoints are expected by the second half of calendar year 2026 [S1]. Given that no currently approved therapy offers durable hair regrowth at scale—with standard care limited by poor compliance—success here could carve a distinct therapeutic category.

Endometriosis development anticipates Phase 2 initiation by Q4 2026 contingent upon prior data review and regulatory inputs [S1,N4]. This indication affects about 10% of women globally and currently lacks FDA-approved disease-modifying treatments [S1]. Targeting PRLR may intercept pathophysiological lesion formation as well as neuropathic pain signaling pathways offering potential advantages over hormonal or surgical interventions.

The strategic emphasis on underexplored mechanisms coupled with capital-efficient clinical advancement is central to Absci’s approach; internal programs reportedly reached IND equivalents two years post-design for an investment near $15 million each versus standard timelines surpassing four years at $50 million-plus [S1]. This rapid trajectory exemplifies the platform’s intended disruption of traditional biologics R&D cycles.

Partnership Model Evolution and Commercial Adoption Challenges

Since initial commercial activity commencement in 2018 incorporating drug creation collaborations and co-development agreements with external biopharma entities [S1,S2], Absci primarily generates revenue through early-stage service fees related to technology deployment—not through clinical or commercial milestone royalties or IP license income.

As of late 2025 no partner has licensed intellectual property emerging from partnered programs for clinical or commercial exploitation reflecting the nascency of broad platform validation and market penetration [S1,S2]. This absence constrains predictable royalty streams typically foundational to biotech valuations beyond pure research services.

The company’s business model hinges on successfully progressing internally developed programs like ABS-201 to pivotal clinical stages serving as proof points potentially catalyzing wider acceptance—and incentivizing partners toward licensing engagements ultimately generating milestone payments and royalties. Meanwhile integration hurdles remain as prospective partners seek reproducible efficacy improvements over entrenched discovery techniques before committing long-term licensing rights [S1,S2].

Capital Structure, Cash Flow, and Capital Allocation Review

As of December 31st, 2025 Absci maintains substantial liquidity with approximately $20 million cash and equivalents set against current assets near $150 million leading to a strong current ratio exceeding 6.5 times—a cushion against short-term obligations totaling roughly $23 million [F1,S4,S5].

Nevertheless operating cash flow remains deeply negative—falling close to negative $93 million last fiscal year—outstripping relatively minimal capital expenditure investing around $1.1 million consistent with a technology-heavy model prioritizing R&D spend over fixed assets [F1]. Free cash flow consequently registers near negative $94 million highlighting considerable burn assembling clinical programs and expanding platform capabilities.

Net equity stands close to $189 million despite accumulated deficits surpassing $620 million illustrating significant historical net losses incurred primarily investing into technology development and pipeline maturation without offsetting commercial returns yet achieved [F1]. Return on equity approximated negative sixty-one percent underscores ongoing profitability challenges common among early clinical-stage developers focused on product discovery innovation.

No dividends or share repurchases have been declared nor are planned due primarily to operational cash requirements directed toward research expansion; this capital allocation strategy aligns with SEC filings indicating retained earnings redeployed into R&D efforts supporting future value creation pathways [S12,S23].

Capital raising efforts have historically included private placements combined with equity offerings securing necessary funding streams supporting multi-year burn rates while maintaining operational flexibility despite general macroeconomic tightening risks outlined around credit availability uncertainties [S4,S5,S19,S22].

Risks and Uncertainties: Technology Adoption, Regulatory Hurdles, and Funding Needs

Absci faces biotechnology sector-specific risks amplified by its early-stage status:

- The company depends heavily on successful progression and commercialization of product candidates by partners who have yet to license intellectual property rights; delays or failures upstream could materially reduce future milestone payment prospects [S1,S2,S6].

- Regulatory approval processes remain inherently uncertain especially targeting novel indications lacking precedent such as PRLR modulation's disease-modifying effects in AGA and endometriosis; any unexpected regulatory hurdles could delay development timelines or increase costs substantially [S9,S14,S16].

- Patent infringement litigation risk exists within crowded biologics IP landscapes; navigating third-party patent claims could require substantial resources or limit technology deployment scope [S17,S21].

- Financial market volatility compounded by macroeconomic stressors imposes funding access challenges potentially forcing dilutive financings or unfavorable partnership terms limiting long-term shareholder value creation [S19,S22].

- International expansion exposes Absci to complexities including anti-bribery compliance burdens like FCPA considerations which could affect operations outside the US framework [S6,S24].

- Absence of marketed products means revenues remain dependent on partnership successes rendering financial performance volatile subject to partners’ pipeline advancement decisions [S1,S2,S20,S25].

Mitigation attempts include focusing clinical efforts on indications with obvious unmet needs supporting compelling efficacy narratives and leveraging internal AI-native platform differentiation designed for capital efficiency reducing traditional costly discovery development bottlenecks.

Milestones Ahead: Pipeline Readouts, Regulatory Initiatives, and Partnership Expansions to Watch

Market attention should focus intensely on forthcoming catalyst events including:

- Interim data from the ongoing HEADLINE Phase 1/2a trial evaluating ABS-201 for androgenetic alopecia slated for release during the second half of calendar year 2026 aims to provide critical early proof-of-concept validity leveraging exploratory efficacy signals alongside safety profiles measured from initial cohorts dosed [S1,N4].

- Planned initiation of Phase 2 study evaluating ABS-201’s therapeutic potential in endometriosis targeted around Q4 2026 contingent upon prior efficacy dataset appraisal and regulatory feedback remains pivotal for confirming non-hormonal durability potential addressing pain pathways fundamental to this sizeable underserved population segment [S1,N4].

- Watch also partner acquisition announcements or licensing deals signaling acceptance thresholds crossed transitioning Absci’s platform offerings beyond early stage services toward sustainable royalty-bearing contracts.

Achieving these milestones may unlock incremental revenue growth avenues while catalyzing broader ecosystem confidence in AI-powered biologics discovery driving next-gen drug pipelines derived from Absci’s Integrated Drug Creation paradigm.

This analysis relies solely on documented corporate financial disclosures and official sources without speculative forecasting or investment advisements. Understanding Absci’s evolution requires balancing their technologically ambitious framework against tangible progress indicators typical within an innovator still verifying early clinical stage potential amid significant resource consumption characteristic of biotech pioneers.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments