Andretti Acquisition Corp. II's Path to Its Business Combination: Growth Prospects and Execution Risks

An analysis of Andretti Acquisition Corp. II’s SPAC financial baseline, strategic approach, and risks ahead of its September 2026 merger deadline.

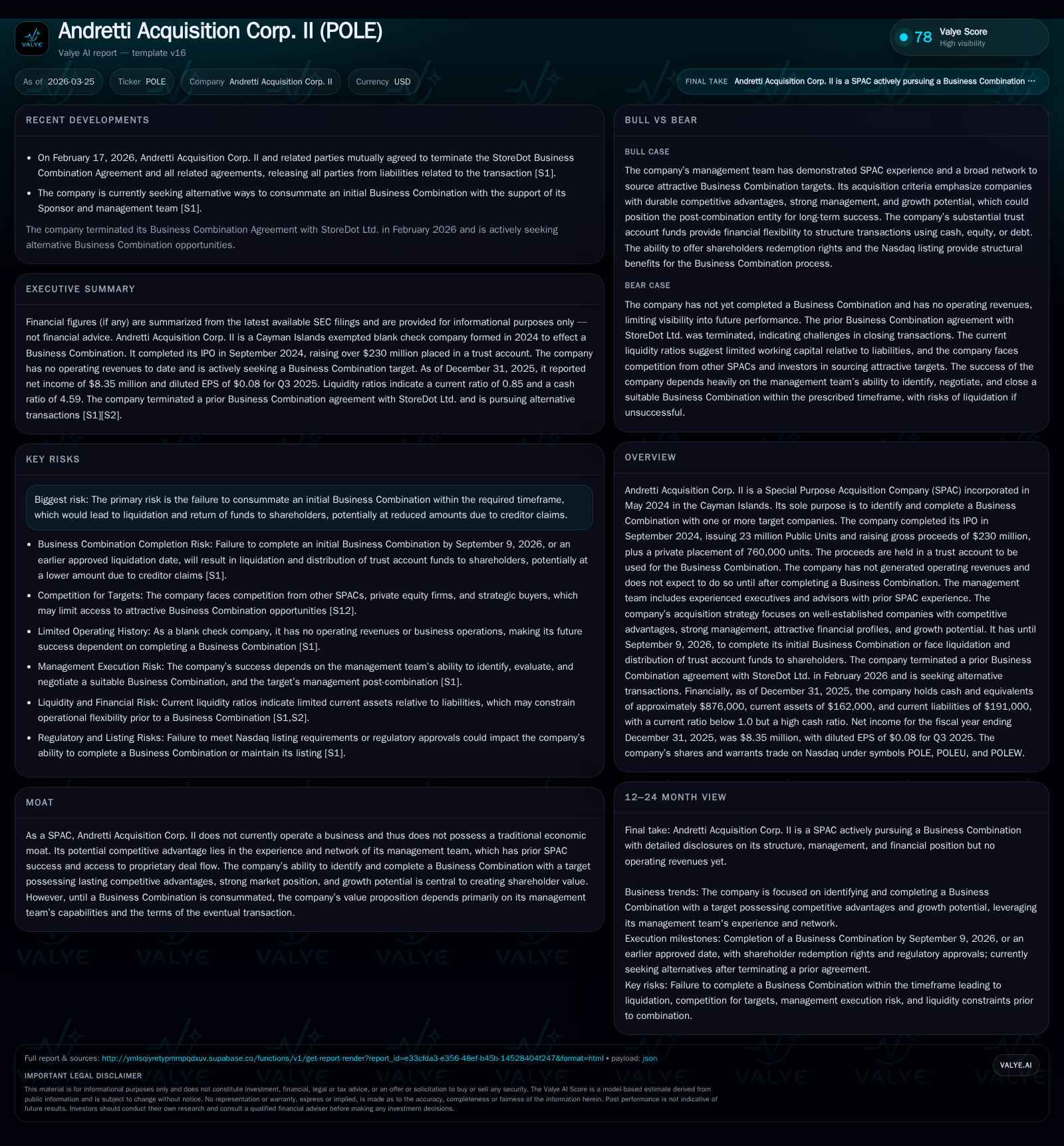

Andretti Acquisition Corp. II, a Cayman Islands-based SPAC formed in May 2024, raised approximately $237.6 million through its IPO and private placement, all held in trust pending a business combination. The company has no operating revenues to date and reports a widening operational loss alongside rising net income driven mainly by non-operating factors. The management team's industry experience and proprietary deal sourcing underpin value creation efforts as the September 2026 combination deadline approaches. Structural risks include mandatory liquidation if no deal is consummated on time, shareholder redemption dynamics, and regulatory requirements.

SPAC Performance Since IPO: Financial Metrics and Operational Activity

Andretti Acquisition Corp. II was incorporated in May 2024 as a Cayman Islands exempted company with the purpose of completing a business combination within 24 months following its IPO in September 2024 [S1]. The IPO raised gross proceeds of $230 million through issuance of 23 million units at $10 each—including full overallotment exercise—and was complemented by a private placement of 760,000 units totaling $7.6 million from the Sponsor and BTIG. Approximately $231.15 million of these proceeds were placed into a trust account managed by Continental Trust Company as trustee [S1]. This trust preserves principal for eventual use in an approved business combination.

As typical for blank check companies structured as SPACs, Andretti Acquisition Corp. II has generated no operating revenues since inception or during this pre-combination phase and does not expect to do so until after consummating a business combination [S1][S26]. Operating expenses reflect organizational costs, administrative expenses related to public listing, legal fees for transaction negotiations, and due diligence activities.

Financial metrics through fiscal year-end 2025 illustrate these characteristics:

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 8 | -1199985 | -1410877 | +174.1% |

| 2024 | 3 | -391548 | -303225 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -81.4 |

| 2024 | -34.5 |

Source: SEC companyfacts cache [F1].

Source: [F1]

The increasing operational losses are primarily due to rising costs associated with regulatory compliance and acquisition preparation [F1]. Positive net income stems largely from non-operating financial activities such as warrant revaluations typical for SPAC accounting before closing transactions [F1]. Negative operating cash flow deepened accordingly.

The negative equity position reflects accumulated losses relative to initial capital plus deferred underwriting fees; this is common among SPACs prior to completing merger transactions that reset financial statements under combined entities.

Management Team’s Role in Target Identification and Deal Sourcing

Leadership includes Executive Chairman William J. Sandbrook and CEO William M. Brown dedicating full-time effort toward deal origination [S1][S6]. Advisors Mario Andretti and Michael M. Andretti provide brand recognition and strategic networks.

The team leverages broad relationships across private equity sponsors, investment bankers, corporate strategists, and intermediaries—yielding proprietary deal flow outside standard auction processes—providing access to acquisition prospects often unavailable to competing SPACs [S5][S6].

Due diligence encompasses meetings with incumbent management teams; document reviews; possible site inspections; customer/supplier interviews; and comprehensive legal and financial scrutiny prior to structuring deals [S9]. This mitigates information asymmetry risks inherent in transitioning private businesses public.

Sponsor expertise also supports flexible capital structures post-combination including debt or equity financing options critical for growth acceleration within targeted sectors [S6].

Business Combination Criteria and Strategic Priorities

While open sector targeting is maintained per IPO structure flexibility, acquisition criteria emphasize:

- Lasting competitive advantage via exclusive technologies or proprietary distribution channels enabling defensible market positions;

- Market leadership potential including sizable market share or capacity for dominance through consolidation;

- Experienced management teams amenable to partnership leveraging combined expertise post-combination;

- Attractive financial profiles reflecting historical profitability or clear paths thereto with scalable cost structures supporting sustainable cash flow;

- Growth trajectories aligned with organic expansion supported by bolt-on acquisitions enhancing scale or geographic reach.

These criteria aim at businesses positioned for stability coupled with strategic acceleration post-listing—where transparency and capital access can enhance shareholder value materially [S5][S9][S29].

Capital Allocation Framework and Shareholder Implications

Trust funds are segregated ensuring principal protection until deployment toward approved combinations [S1][S4]. The Sponsor holds Founder Shares (~2 million) plus Private Placement Units purchased at IPO price but waives redemption rights on founder shares if dissolution occurs without merger closing—a structural alignment incentivizing deal execution over liquidation [S8][S12].

Public shareholders enjoy statutory redemption rights upon initial business combination completion allowing cash-out at about $10.58 per share plus accrued interest based on trust valuation less taxes—irrespective of voting position—via shareholder meeting proxy votes or tender offer processes depending on management discretion under Nasdaq listing rules and securities law [S7][S10][S11]. Redemptions are subject to caps without sponsor consent outside bilateral agreements limiting blocking stakes [S24].

Management may purchase public shares from redeeming shareholders pre- or post-combination complying with SEC Rule 10b-18 safe harbor conditions except when holding material nonpublic information—transactions intended to mitigate excessive redemptions that could jeopardize deals or stabilize liquidity post-announcement [S13][S19].

No dividends or share repurchases occur pre-combination due to lack of operating cash flow; operational costs are covered from funds outside the trust account with limited reserves covering administrative expenses during search phases [F1][S4][S26].

Risks Surrounding Combination Deadline and Liquidation Scenarios

September 9, 2026 marks the end of the Combination Period per amended articles; failure to close a qualifying business combination mandates liquidation distributing trust funds pro rata back to public shareholders less administrative costs estimated near $48K plus creditor claims prioritized under Cayman Islands law governing exempted companies offshore [S1][S12][S28].

Sponsor-held Private Placement Units lack redemption rights or liquidating distributions if no transaction closes—exposing insiders’ invested capital without downside protection afforded public units but aligning incentives toward successful mergers [S8]. Extensions require shareholder approval with dissenters retaining redemption rights offering quasi-call protection but introducing uncertainty near deadlines regarding timing or structural changes proposed during extensions [S11].

Additional risks include valuation uncertainties that may impede independent Board fair market value conclusions required for Nasdaq’s "80% Test" mandating minimum fair market value coverage of trust assets post-combination; conflicts could arise given Sponsor ownership stakes though mitigated partly via independent fairness opinions when conflicts manifest explicitly amid affiliated party transactions flagged under SPAC governance best practices [S15][S29].

Investor Milestones to Monitor Ahead

With zero operating revenues so far as expected in blank check status alongside substantial net income growth rooted in non-cash effects ([F1]), attention should focus on disclosure events signaling deal progress:

- Announcement(s) identifying target candidates meeting stated criteria;

- Filing of proxy solicitation materials or tender offer documents detailing merger structure including cash consideration components;

- Redemption request volumes indicating investor sentiment impacting transaction feasibility;

- Extension amendment proposals requiring shareholder approval;

- Capital raises via PIPEs, debt placements or backstops enhancing liquidity tied directly to deal execution;

- Insider purchases of shares off-market possibly signaling confidence;

- Regulatory Form 8-K filings outlining material transaction developments or contingencies affecting timelines.

SPAC strategy hinges on management’s ability not only to identify attractive targets consistent with mandates but also navigate complex shareholder reconciliation mechanics alongside regulatory frameworks essential to avoid forced liquidation that would dilute stakeholder value drastically.

This analysis synthesizes SEC-sourced data alongside industry standard knowledge regarding blank check companies without offering investment advice nor speculating beyond documented facts. Investors should consider company disclosures holistically while monitoring evolving timelines given fundamental dependencies shaping ultimate outcome viability.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments