UTG Inc's Earnings Volatility Reflects Concentrated Insurance Operations and Strategic Capital Allocation

UTG Inc operates a focused life insurance subsidiary, balancing legacy policy servicing with cautious capital deployment and investment concentration.

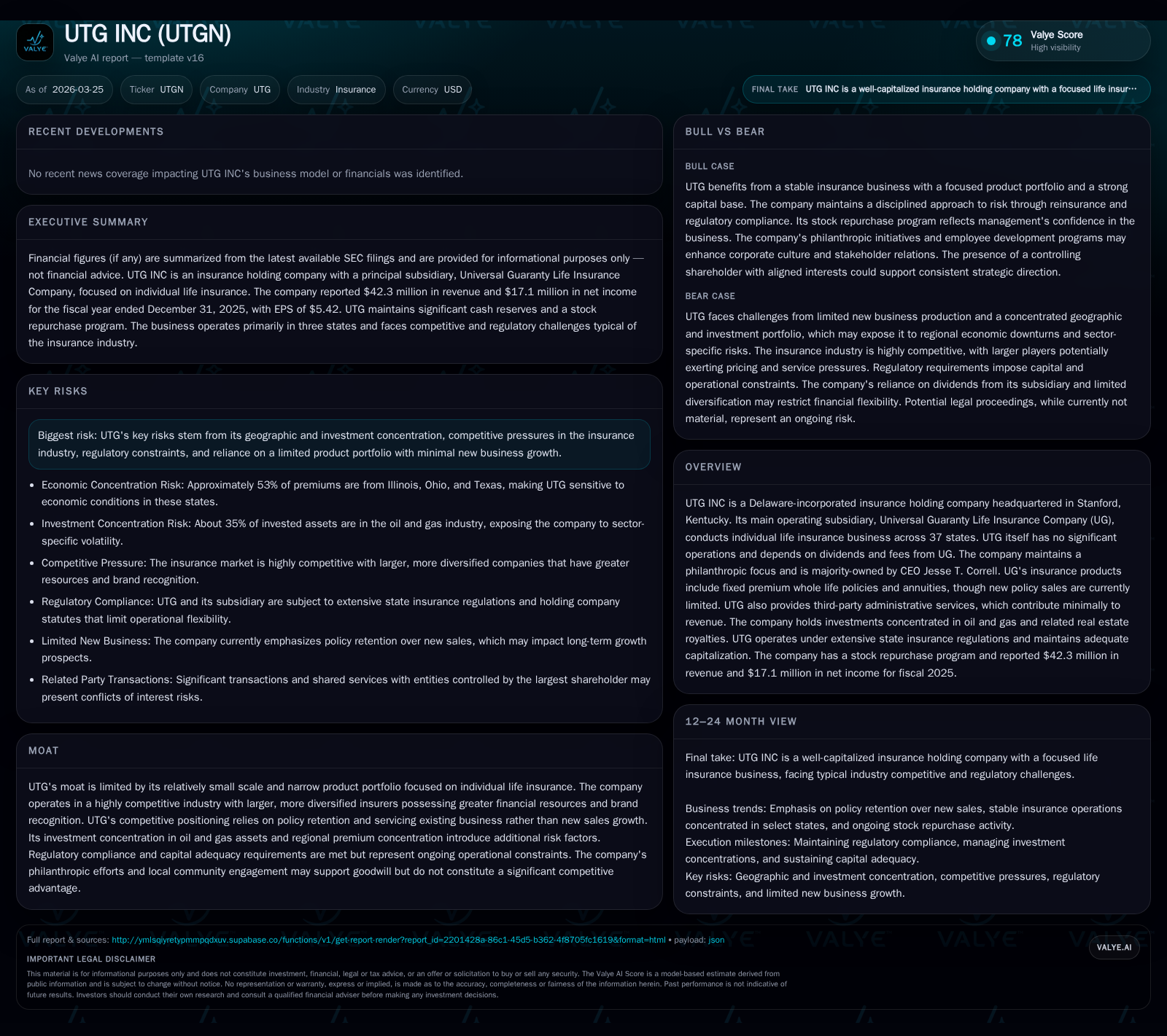

UTG Inc is a Delaware-based insurance holding company whose principal subsidiary, Universal Guaranty Life Insurance Company (UG), conducts individual life insurance business across 37 states. The company's revenue and net income have exhibited significant volatility over recent years, influenced by its strategy of limiting new policy sales and dependence on retaining existing policies. Core risks include geographic premium concentration and sizable exposure to oil and gas investments. Capital allocation initiatives include a consistent stock repurchase program and philanthropic commitments, while regulatory compliance and adequate capitalization remain foundational pillars. Future growth is constrained by limited new business issuance but supported by administrative fees and policy servicing.

Company Overview

UTG Inc is an insurance holding company incorporated in Delaware with headquarters in Stanford, Kentucky. Its primary operating unit is Universal Guaranty Life Insurance Company (UG), an Ohio-domiciled insurer licensed across 37 states that focuses predominantly on individual life insurance policies including fixed premium whole life plans and annuities [S1][S4]. UTG itself performs no significant direct operations but depends on dividends, fees, and distributions from UG for cash flow [S1].

Established in 2005, the company maintains a philanthropic culture centered on support for Christ-based organizations as well as aiding disadvantaged populations [S1]. Jesse T. Correll serves as CEO, Chairman, and majority owner with roughly 69% ownership stakes through affiliated entities [S1][S14].

Historical Financial Performance

UTG's recent financial results demonstrate notable fluctuations attributable to its strategic posture favoring policy servicing over new premium generation. Total revenue peaked at $84.9 million in FY2024 but halved to $42.3 million in FY2025 [F1]. This drop corresponds with restrained issuance of new policies—UG currently limits new policy sales—and continuing focus on managing the existing portfolio rather than expanding it aggressively [S4][S9].

Net income exhibited pronounced variability as well: rising sharply from under $2 million in FY2023 to ~$49.3 million in FY2024 before contracting again to $17.1 million in FY2025 [F1]. Operating cash flows have been persistently negative for multiple years (-$6.5 million most recently) despite reported profits, indicating timing mismatches between earnings recognition and actual cash collections or outflows related to claims, reserves, or administration [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 42 | 17 | -7 | -50.1% | -65.4% |

| 2024 | 85 | 49 | -2 | +234.0% | +2419.6% |

| 2023 | 25 | 2 | -10 | -63.5% | -94.3% |

| 2022 | 70 | 34 | -5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 782812 | 7.4 |

| 2024 | 648152 | 23.5 |

| 2023 | 881966 | 1.2 |

| 2022 | 685808 | 21.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue dipped significantly from FY2024 to FY2025 as the company shifted away from new sales toward conserving the existing book.

Business Model & Industry Position

Universal Guaranty Life Insurance Company anchors UTG’s sole significant segment: individual life insurance in selected U.S. states [S1][S4]. Its product offerings comprise a limited array of fixed whole life policies featuring level premiums payable for life alongside a single premium annuity with a guaranteed minimum interest rate that is subject to adjustment [S6]. New issue activity is currently curtailed; management has prioritized retention of existing policyholders to maintain persistency rather than seek substantial top-line expansion — recognizing the high costs tied to acquiring new business relative to returns [S9].

In addition to underwriting life insurance contracts primarily targeted at individuals aged up to mid-70s (issue age up to 75 for whole life products), UG also earns ancillary fees from third-party administration services for other insurers’ life insurance portfolios though this line contributes minor revenue [S9]. The heavy reliance on servicing legacy policies creates predictable but potentially limited growth opportunity.

Competition within this space is intense with a plethora of much larger insurers enjoying diversified product lines (including group policies and various annuity forms), extensive distribution networks including large agency forces or broker channels,and stronger brand awareness [S4]. UTG’s scale advantages lie more in localized niche focus plus specialized servicing agility rather than broad market penetration.

Investment Portfolio & Risk Concentrations

A distinctive feature of UTG’s asset base is its substantial investment concentration linked to the oil and gas sector — roughly one-third of invested assets are committed here including real estate royalties tied to petroleum operations (30% of real estate portfolio) [S4]. This exposure introduces pronounced commodity price sensitivity not typically observed among broad-life insurers that prefer diversified fixed-income portfolios.

Geographically too the premium stream exhibits concentration: approximately half of premiums come from three states—Illinois, Ohio and Texas—which subjects revenue inflows to those regions’ economic cycles [S4]. Such geographic concentration could impact persistency rates adversely if localized economic downturns reduce policyholder capacity to maintain premium payments.

Statutory regulation imposes caps on investments per issuer or asset class which UG complies with; maintaining required surplus levels ($2.5 million minimum statutory surplus) helps ensure solvency buffers against underwriting or market shocks [S13][S14].

Regulatory Framework & Capital Adequacy

UTG operates under extensive state-regulated frameworks typical of U.S.-domiciled insurers: licensing requirements govern underwriting activities while capital adequacy must be demonstrated annually via reporting standards such as those promulgated by the National Association of Insurance Commissioners (NAIC) [S13]. The regulatory landscape restricts aggregate investment concentrations and mandates reserve levels computed conservatively using prescribed mortality tables and discount rates reflective of upper-medium grade bond yields [S6][S18].

UG maintains risk-based capital ratios considered more than adequate under applicable formulas aimed at identifying companies needing regulatory attention but not for ranking well-capitalized firms [S13]. State guaranty assessments further protect policyholders by providing industry-wide funds funded by insurer contributions should insolvencies occur elsewhere.

Capital Allocation & Shareholder Returns

Capital deployment has reflected steady share repurchases sanctioned by the Board since inception of the buyback program with $26 million total spent acquiring common shares up through December 31st ,2025; during fiscal year 2025 alone about $783K was spent repurchasing approximately eighteen thousand shares at prices influenced by prevailing market conditions [F1][S13]. These buybacks exhibit management’s preference for returning excess capital when growth opportunities remain spotty.

Dividends do not appear prominent based on available disclosures; instead the company channels a meaningful portion of earnings into philanthropic activities aligning with its charitable mission documented in annual reports focusing on Christian service organizations [S1].

Executives receive compensation packages blending salary increments with annual bonuses tied loosely to operating results absent formal employment agreements — signaling a flexible but performance-sensitive remuneration philosophy [S26].

Growth Prospects & Strategic Constraints

Explicit guidance around revenue or new business targets is absent; current strategy favors preservation and renewal of existing policies over fresh customer acquisition given associated costs outweigh perceived benefits at this time [S9]. The fixed product line lacks modern diversification into indexed or variable products which could otherwise stimulate renewed sales momentum.

Potential drivers for growth could encompass opportunistic acquisitions within similar regional niches or expanding third-party administration services if scalable; however caution prevails due to regulatory scrutiny regarding transactions between affiliates given correlated ownership structures especially involving majority stakeholder Mr. Correll’s affiliated entities [S13][S7].

Risks constraining growth include regulatory constraints limiting investment flexibility alongside competition from large well-resourced players able to leverage analytics-driven marketing platforms plus multi-channel distribution arms.Significant exposure stemming from oil/gas investments adds macroeconomic sensitivity beyond standard underwriting risks affecting profitability.

Key Risks Summary

- Geographic premium concentration in three states heightens vulnerability to region-specific economic downturns.

- Investment portfolio concentrated heavily (~35%) in oil/gas-related assets increases commodity price risk.

- Limited product range focused almost exclusively on fixed whole life policies restricts market reach.

- Smaller scale compared to industry giants reduces bargaining power with agents/distributors lowering brand visibility.

- Regulatory oversight imposes capital/transactional restrictions that may slow adaptation or diversification efforts.

- Operating cash flows remain negative suggesting possible liquidity pressure despite accounting profits.[S7][F1]

Conclusions

UTG Inc emerges as a niche player relying predominantly on Universal Guaranty Life Insurance Company’s servicing of an established book of individual life policies disseminated mostly within three U.S states.[S9] Growth has stalled owing largely to management’s strategic choice not to focus on securing new insurance sales amid cost concerns.[S4] Nonetheless prudent capital management including active stock repurchases coupled with solid capitalization buffers ensures operational durability.[F1][S13] Investment concentration in oil & gas sectors distinguishes UTG from peers but also introduces unconventional risk vectors into its financial profile.[S4]

The absence of meaningful diversification both geographically among premium streams and product-wise suggests that UTGN faces formidable challenges scaling organically or offsetting cyclical downswings without transformative change.Monitoring developments around policy persistency metrics alongside trends in administrative services revenue may offer indicators regarding incremental growth opportunities absent broader strategic pivots.Analysts should also watch any shifts towards resuming new business production or pursuing acquisitions as clues about future trajectories.

This analysis is compiled solely for informational purposes based on publicly available SEC filings dated up to March 25th ,2026 ; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments