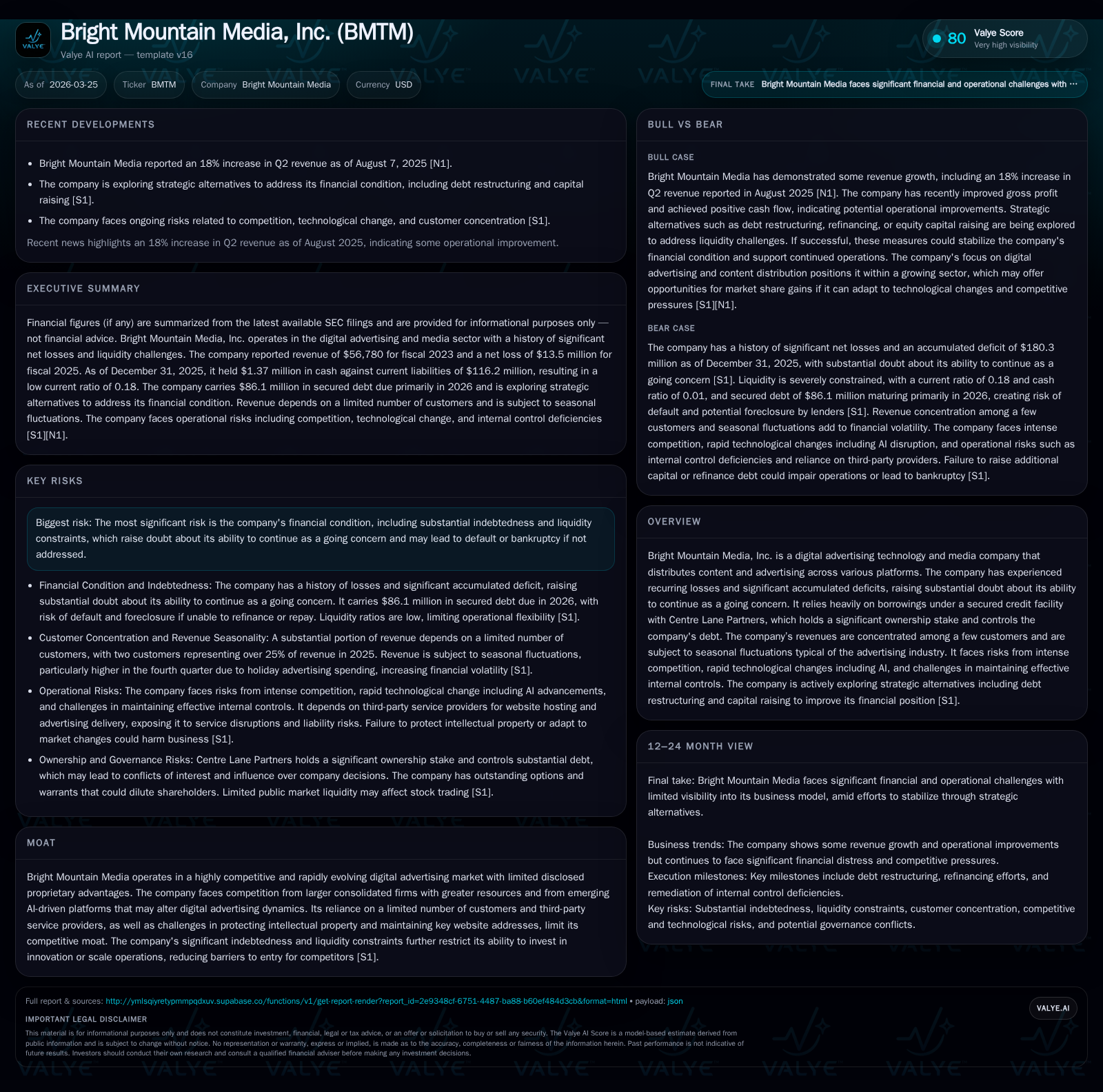

Bright Mountain Media’s Revenue Collapse and Mounting Debt Challenge Future Viability

Sharp revenue decline and heavy secured indebtedness raise serious doubts about Bright Mountain Media's sustainability amid competitive digital advertising shifts.

Bright Mountain Media, Inc. has experienced a precipitous fall in revenues, from nearly $1.7 million in 2018 to just over $56,000 in 2023, accompanied by ongoing net losses and a deeply negative equity position. Despite some recovery in operating cash flow in 2025, the company faces severe liquidity constraints with $86.1 million of secured debt maturing mostly by year-end 2026, controlled by Centre Lane Partners. The highly concentrated customer base and seasonal advertising patterns add volatility to revenues. Intense competition, rapid AI-driven market changes, legal disputes including a $1.7 million judgment, and material weaknesses in internal controls further challenge its prospects. Management is pursuing strategic alternatives such as debt restructuring to improve financial stability, yet sizable refinancing needs remain critical milestones for investors to watch.

Historic Performance: Sharp Revenue Decline Despite Operating Loss Improvements

Bright Mountain Media’s financial history reveals a dramatic contraction in its top line alongside persistent losses extending through fiscal year 2025. Annual revenues plummeted from approximately $1.74 million in FY2018 to just under $57 thousand in FY2023 — a near-97% reduction indicating severe erosion of the company’s core business activity [F1]. Concurrently, while operating income remained negative across this interval, the loss narrowed considerably in FY2025 to about -$1.43 million from an operating loss of -$4.92 million the prior year, reflecting roughly a 71% improvement year-over-year [F1].

Net income continued deeply in deficit territory at -$13.45 million for FY2025 but slightly improved by around 21% compared to FY2024’s -$17.02 million loss [F1]. Notably, operating cash flow transitioned into positive territory last year with approximately $1.25 million generated versus negative cash flows previously; this was achieved alongside a modest increase in capital expenditures which nevertheless remain minimal ($111k in FY2025) relative to historical levels [F1]. The emerging ability to generate operational cash supports limited financial flexibility despite ongoing net losses.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -13 | 1 | -1 | 111000 | +21.0% |

| 2024 | -17 | 2 | -5 | 14000 | +52.1% |

| 2023 | -36 | -5 | -27 | 14000 | -337.7% |

| 2022 | -8 | -3 | -5 | 14000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1 | 17.6 | |

| 2024 | 2 | 26.9 | |

| 2023 | 0 | -5 | 76.2 |

| 2022 | 5000 | -3 | 57.7 |

Source: SEC companyfacts cache [F1].

This table summarizes Bright Mountain Media's annual revenue collapse paired with improving operating loss trajectory and increasing positive operating cash flow as of FY2025.

Revenue Concentration and Seasonality: Customer Dependence Risks

Revenue concentration poses significant operational risks for Bright Mountain Media. As reported for FY2025, two customers accounted for roughly one-quarter of total revenues — specifically about 13.6% and 11.9% respectively — underscoring dependence on a limited client base with material impact on quarterly results if relationships deteriorate or contracts are terminated [S5],[S2],[S11]. Moreover, customer contracts permit termination with relatively short advance notice (not exceeding thirty days), magnifying volatility potential in an already unstable revenue environment.

Adding complexity is pronounced seasonality consistent with industry norms; advertising demand typically spikes during the fourth quarter tied to holiday marketing cycles [S16]. Such fluctuations intensify pressure on forecasting accuracy and working capital management given that other quarters may underperform materially.

These interrelated factors—high client concentration combined with seasonal patterns—amplify earnings unpredictability and complicate the firm’s ability to build sustained revenue growth absent broadening its customer portfolio or locking-in longer-term engagements.

Debt Profile and Going Concern Doubts

The company faces severe liquidity challenges driven chiefly by outstanding secured indebtedness totaling approximately $86.1 million as of December 31, 2025, primarily owed to Centre Lane Partners under a senior secured credit facility [S4],[S7]. The debt amortization schedule concentrates payments heavily within calendar year 2026: $1.4 million due June and September each followed by a balloon payment exceeding $81 million due December 20, 2026 [S4]. Failure to meet these obligations or refinance effectively could trigger default events giving Centre Lane rights including foreclosure on company assets — heightening bankruptcy risk.

Financial metrics reflect this stress starkly: the current ratio stands at an extremely low ~0.18 (current assets of roughly $20.7 million versus current liabilities above $116 million) indicating acute short-term liquidity constraints [F1]. Auditors have issued a going concern opinion explicitly citing substantial doubt regarding the company’s ability to continue without securing fresh capital or successful restructuring measures [S7]. This debt burden restricts operational flexibility because compliance with lender-imposed covenants limits incurrence of further leverage or allocation of resources without approval.

Centre Lane’s dominant creditor position—not only controlling the debt but also owning large equity stakes—creates governance complexities that may influence strategic decisions disproportionately towards lender interests over minority shareholders’ preferences [S25].

Strategic Alternatives and Capital Raising Efforts

Management acknowledges the precariousness of their financial stance and is actively exploring multiple strategic alternatives including refinancing or restructuring existing debt obligations as well as seeking additional equity capital infusions [S1],[S3],[S7]. However, no binding agreements for such capital raises currently exist.

Given the constrained trading volumes and depressed market valuation of common shares traded OTCQB Market—and absence of robust secondary market support—the likelihood of prompt sizable equity raises appears limited absent significant operational turnaround or creditor concessions [S15]. The persistent net losses and weakened revenue base further challenge fundraising prospects.

Additionally, asset sales or operational downsizing may form part of contemplated strategies though concrete execution plans remain undisclosed publicly and should be monitored closely as potential catalysts or liquidity relief paths.

Competitive Pressures in Digital Advertising Technology

Bright Mountain operates within an intensely competitive digital advertising ecosystem marked by rapid technology evolution particularly involving AI innovations reshaping user engagement channels and advertiser behaviors [S29],[S16]. Larger consolidated firms possess greater capital resources able to acquire emerging technologies or drive scale efficiencies that BMTM cannot match currently.

AI-driven content delivery platforms threaten traditional open internet ad models by redirecting consumer attention away from publisher websites thus compressing traffic monetization opportunities—a core revenue driver for BMTM’s publishing partners [S16]. The resulting shifts could diminish demand for conventional display advertising solutions offered by independent ad tech providers like Bright Mountain.

Moreover, persistent risks around online ad fraud detection efficacy, intellectual property protection shortcomings, reliance on critical third-party web hosting services susceptible to outages, plus difficulties maintaining key website domains all exacerbate competitive vulnerabilities faced by BMTM relative to better-resourced market peers [S24],[S17],[S20].

Legal Challenges Impacting Financial Outlook

The company remains entangled in critical litigation notably with Ladenburg Thalmann & Co., arising from disputes over investment banking fee claims related to prior acquisitions and financing transactions [S6],[S8]. Ladenburg secured a court judgment awarding damages totaling around $1.7 million against Bright Mountain; efforts to overturn this via motion were denied leading to an appeal proceeding scheduled for early April-2026 at the Eleventh Circuit Court of Appeals.

While outcomes remain uncertain by report date they pose contingent liabilities weighing on financial planning—necessitating bond arrangements obtained via Centre Lane credit amendments to stay execution temporarily pending appeal resolution [S6],[S8]. Other smaller litigious matters exist but are individually immaterial though collectively may influence operational distractions and costs.

Internal Controls and Operational Risks

Material weaknesses persist in Bright Mountain’s internal control over financial reporting derived primarily from historical deficiencies identified under Sarbanes-Oxley Act requirements; remediation efforts continue but are not concluded successfully yet [S1],[S7]. These lapses risk mismatches or errors in financial disclosures undermining stakeholder trust—particularly relevant given the company's liquidity stress conditions where transparent communications are vital.

Inadequate disclosure controls could allow delayed identification or correction of reporting errors impacting quarterly filings reliability which could compound difficulties attracting capital or investor interest during restructuring phases.

Capital Allocation: The Absence of Dividends amid Negative Equity

Reflecting ongoing liquidity preservation imperatives combined with recurring losses, Bright Mountain has ceased dividend payments entirely since at least FY2022 where nominal dividends disappeared after small payouts prior years; no share repurchase programs have been undertaken recently either [F1],[S14].

Equity holders face diluted claims given deeply negative shareholders’ equity approximating -$76.6 million as of end-2025 driven principally by accumulated deficits exceeding $180 million reflecting extensive historical earnings erosion—highlighting significant balance sheet impairment that will require meaningful operational recovery before capital return policies resume plausibility [F1].

Financial Milestones to Watch: Debt Maturity and Refinancing Needs

Critical near-term dates revolve around repayment deadlines embedded within the Centre Lane Senior Secured Credit Facility: incremental installments totaling nearly $2.8 million spread over Q2-Q3-2026 and a substantial balloon maturity payment exceeding $81 million due by December 20, 2026 are principal liquidity determinants governing survival outlook [S4],[S25]. Failure to refinance or extend these maturities would trigger default permitting Centre Lane foreclosure rights likely culminating in bankruptcy proceedings given limited asset coverage otherwise.

Investors should closely monitor developments around any debt amendments announced through periodic filings along with management commentary addressing refinancing progress as these events constitute pivotal junctures dictating operational continuity or restructuring necessity.

Disclaimer: This report synthesizes publicly available information including SEC filings without speculation beyond documented facts; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments