FiscalNote's Strategic Focus and Capital Constraints Weigh on Financial Performance in 2025

FiscalNote continues to emphasize its core policy intelligence platform while managing liquidity and growth challenges.

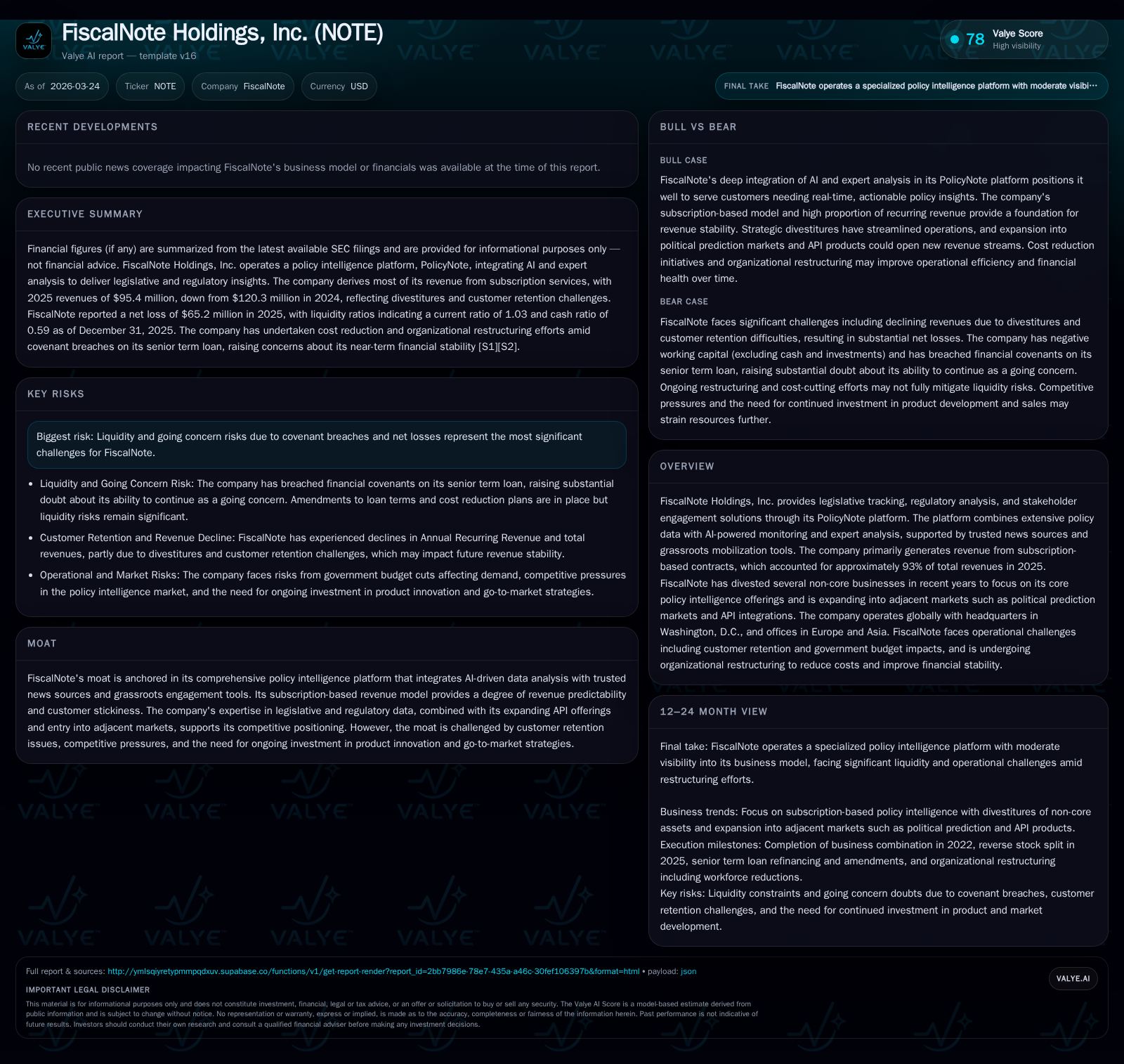

FiscalNote Holdings, Inc. specializes in AI-driven legislative tracking and policy intelligence through its flagship PolicyNote platform, generating the majority of revenue from subscription services. The company’s recent focus has shifted towards streamlining operations by divesting non-core assets and expanding into adjacent markets like political prediction and APIs. Despite efforts to rationalize costs, FiscalNote faces persistent operating losses and negative cash flows, with liquidity concerns magnified by covenant breaches on its senior term loan. Its competitive moat relies on integrating policy data with AI and grassroots tools, but customer retention issues and macroeconomic factors constrain growth prospects.

Company Overview and Business Model

FiscalNote Holdings, Inc. operates primarily through its PolicyNote platform, an AI-powered legislative tracking and regulatory analysis solution that integrates extensive policy data with expert insights and grassroots mobilization tools such as VoterVoice [S1][S24]. Subscription-based contracts dominate its revenue mix, contributing approximately 93% of total revenues in fiscal year (FY) 2025 [S24]. The platform is designed to provide customers—primarily enterprises and government entities—with real-time visibility into evolving political and regulatory landscapes, leveraging proprietary AI models combined with trusted news sources including CQ and Roll Call.

The company undertook strategic measures over recent years to shed non-core businesses like Dragonfly, Oxford Analytica, Board.org, and Aicel Technologies to streamline operations and sharpen focus on core policy intelligence offerings [S24][S39]. Additionally, FiscalNote is advancing into adjacent markets such as political prediction markets and enhancing its agentic API offerings to allow customers to embed policy intelligence within internal systems [S24]. This reflects a broader industry trend where clients increasingly demand integrated tech solutions beyond standalone data feeds.

Historical Financial Performance

FiscalNote's financial results reflect ongoing challenges balancing investment-led growth against costs and operational efficiency:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -65 | -11 | -50 | 7 | -785.6% |

| 2024 | 10 | -5 | -32 | 9 | +108.2% |

| 2023 | -115 | -35 | -98 | 8 | +47.1% |

| 2022 | -218 | -73 | -88 | 11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -19 | -105.3 | |

| 2024 | -14 | 9.7 | |

| 2023 | 88000 | -43 | -265.7 |

| 2022 | 88000 | -84 | -150.8 |

Source: SEC companyfacts cache [F1].

Revenue declined sharply by about 20% year-over-year in FY25 while operating losses deepened by approximately 55%, signaling contraction pressures alongside higher costs. [F1]

Subscription revenue fell significantly from $111 million in FY24 to about $89 million in FY25 indicating either customer churn or reduced new business momentum [S24]. Advisory, advertising, books, and other revenues represent a minor portion of total sales.

The company’s operating cash flow remained negative at $-11.4 million despite cost controls implemented over the period; capital expenditures related primarily to software development consistently consume roughly $7–9 million annually [F1][S25]. Maintaining robust R&D investments is essential given the competitive nature of AI-driven policy technology.

Return metrics are weak with an approximate ROE near negative 105% for FY25—a result of sustained losses coupled with declining equity levels [F1]. Goodwill on the balance sheet stands at nearly $123 million but was impaired by $12.4 million during Q4’25 following recalibrations of expected future cash flows driven by deteriorating operational performance [S12][F1].

Revenue Geography and Customer Concentration

Geographically, FiscalNote generates the bulk of revenues from North America—the U.S.—which accounted for almost $85.6 million or nearly 90% of total sales in FY25 compared to about $95.5 million in FY24 [S15]. European revenue dropped sharply from $21.8 million to roughly $9.2 million over the same period due primarily to divestitures and reduced market footprint abroad.

The company also serves some clients in Australia ($0.6M) while Asia recorded no revenue contribution for FY25 after prior modest amounts [S15]. The shrinkage outside North America reflects deliberate business decisions aimed at focusing resources on higher-margin core markets.

FiscalNote’s subscription offerings are generally annual contracts that provide predictable top-line visibility through Annual Recurring Revenue (ARR), which is monitored internally though actual collections can vary based on customer behavior including renewals or cancellations [S17]. Maintaining ARR above lender requirements has been challenging as evidenced by recent covenant breaches.

Capital Structure and Liquidity Position

The firm carries substantial indebtedness following multiple financing rounds aimed at extending runway post-business combination activities:

- At December 31, 2025 gross debt stood at approximately $131.9 million including a cornerstone $74.1 million senior term loan due August 2029 secured by first liens on most assets [S5][F1].

- Other debt consists primarily of convertible notes totaling around $57 million related to prior funding cycles [S6][S23].

- The senior term loan carries a high variable interest rate linked to SOFR plus margins initially set at +7% or +8%, with effective rates above double digits due to recent SOFR increases; interest expense for FY25 related to this facility was ~$3.5 million with amortization of issuance costs further impacting financials [S26][F1].

The company breached its minimum ARR covenant as of January 31, 2026 but secured a waiver from lenders along with adjustments that increased interest rates further and modified other covenant terms through March 2027 [S6][S26]. This highlights ongoing liquidity risks which are mitigated somewhat by approximately $24 million cash & equivalents ending FY25 yet underscore precarious financial flexibility going forward.

Cash flow from operations remains negative driven both by operating losses and working capital outflows; combined with CapEx results in negative free cash flow exceeding -$18 million annually raising concerns about continued funding needs absent improved earnings or asset sales [F1][S20].

No dividends have been declared or paid since inception given accumulation of historical net losses exceeding $870 million as of end-2025; no share repurchase programs are currently active either reflecting focus on preserving capital for operational resilience rather than capital returns [S14][F1].

Strategic Focus and Growth Outlook

FiscalNote’s strategy emphasizes strengthening its core PolicyNote subscription service ecosystem combining AI data analytics with actionable legislative insights supplemented by trusted media partners such as CQ/Roll Call plus grassroots engagement capabilities through VoterVoice [S24]. In parallel, it is pursuing extensions into adjacent areas including political prediction markets—a field attracting attention for deploying crowd-sourcing models against geopolitical forecasting—and expanding API functionality enabling clients bespoke integrations into internal workflows.

Management identifies growth opportunities primarily around:

- Cross-selling additional modules within existing enterprise customer accounts,

- Expanding penetration among government entities globally,

- Monetizing new product innovations such as APIs embedding policy intelligence across client platforms,

- Leveraging increasing adoption curves for AI-enabled regulatory technologies.

However, headwinds persist in the form of stiff competition from other legislative tracking firms employing both organic tech development and M&A tactics alongside tougher government budgets that may cap spending particularly amid macroeconomic uncertainty [S24][N1]. Moreover, noted challenges retaining customers affect ARR stability—a key metric scrutinized closely by debt providers—and necessitate ongoing investments in product enhancement plus sales force optimization.

Recent Corporate Actions & Organizational Moves

During FY25 FiscalNote divested non-core segments including Dragonfly ($15+ million sale proceeds), Oxford Analytica, Aicel Technologies (~$9+ million proceeds), aiding immediate liquidity though reducing total revenue base [S24][S39]. Headcount reductions amounted to nearly 150 full-time positions reflecting cost rationalization aligned with business simplification efforts that started earlier following a significant reverse stock split executed mid-2025 aimed partly at boosting share price metrics [S14][N1].

Despite these adjustments, impairment charges including goodwill write-downs indicate pressure on reported asset quality linked to softness in forecasted cash flows under conservative market assumptions initiated during annual impairment testing periods near year-end.

Risks Summary

Key risks identified by management center heavily around liquidity constraints exacerbated by covenant breaches leading to potential acceleration risks under loan agreements if remedial measures fail [S9][S11]:

- The requirement to maintain minimum ARR targets aligns directly with ability to renew subscriptions yet faces weakness given current customer retention metrics.

- Interest payments tied to SOFR indexes expose FiscalNote to rising cash outflows amid climbing Fed rates creating refinancing cost pressures.

- Operational execution risks linked to competitive marketplace require investment balance between innovation spending versus financial discipline.

- Macroeconomic volatility affecting governmental clients may limit budgetary allocations thus restricting contract renewals or expansions.

- Potential legal or intellectual property disputes remain remote but possible reputational risks exist inherent in technology sectors reliant upon proprietary data algorithms.

What To Watch (Analysis)

In absence of explicit out-year guidance from management this filing cycle, monitoring FiscalNote’s trajectory involves:

- Quarterly ARR trends will be critical for assessing ability to sustain subscription revenues;

- Cash burn levels vis-à-vis debt servicing obligations especially under amended covenant conditions;

- Progress integrating new product lines such as political prediction markets into commercial pipelines;

- Impact of further cost optimization measures including any additional workforce adjustments or geographic contractions;

- Market reception towards API services indicating successful entry into platform-centric consumption models among large institutional clients;

- Development status of technological enhancements including AI capabilities relevant to legislative data parsing accuracy plus timely updates;

- Any strategic transactions that may provide capital relief or portfolio repricing opportunity beyond recent divestitures.

Conclusion

FiscalNote's operating environment throughout FY25 reflected ongoing adaptation toward refocused policies emphasizing core product strength amid pronounced financial headwinds mainly driven by declining revenues and elevated debt burdens compounded by adverse macroeconomic influences impacting customers' willingness or capacity to spend on policy intelligence services.

While its comprehensive AI-based platform combining multi-source policy content offers differentiation potential sustaining competitive moat elements — notably given entrenched subscription relationships — clear execution risks exist tied principally to liquidity management challenges underscored by covenant waivers necessary early in FY26.

Moving forward success will depend heavily on improving customer retention dynamics alongside deliberate measured investments targeting sustainable growth pathways such as adjacent market expansion balanced against operational cost discipline required by current financial obligations.

This report is prepared solely for informational purposes based on publicly available documents dated up to March 24, 2026 including SEC filings and credible news sources; it does not constitute investment advice nor recommendation regarding FiscalNote Holdings' securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments