Hour Loop Inc. Surges Profitability with Tech-Driven Wholesale Expansion

Leveraging proprietary software and scalable wholesale sourcing, Hour Loop navigates a sharply improved financial profile in a complex Amazon marketplace.

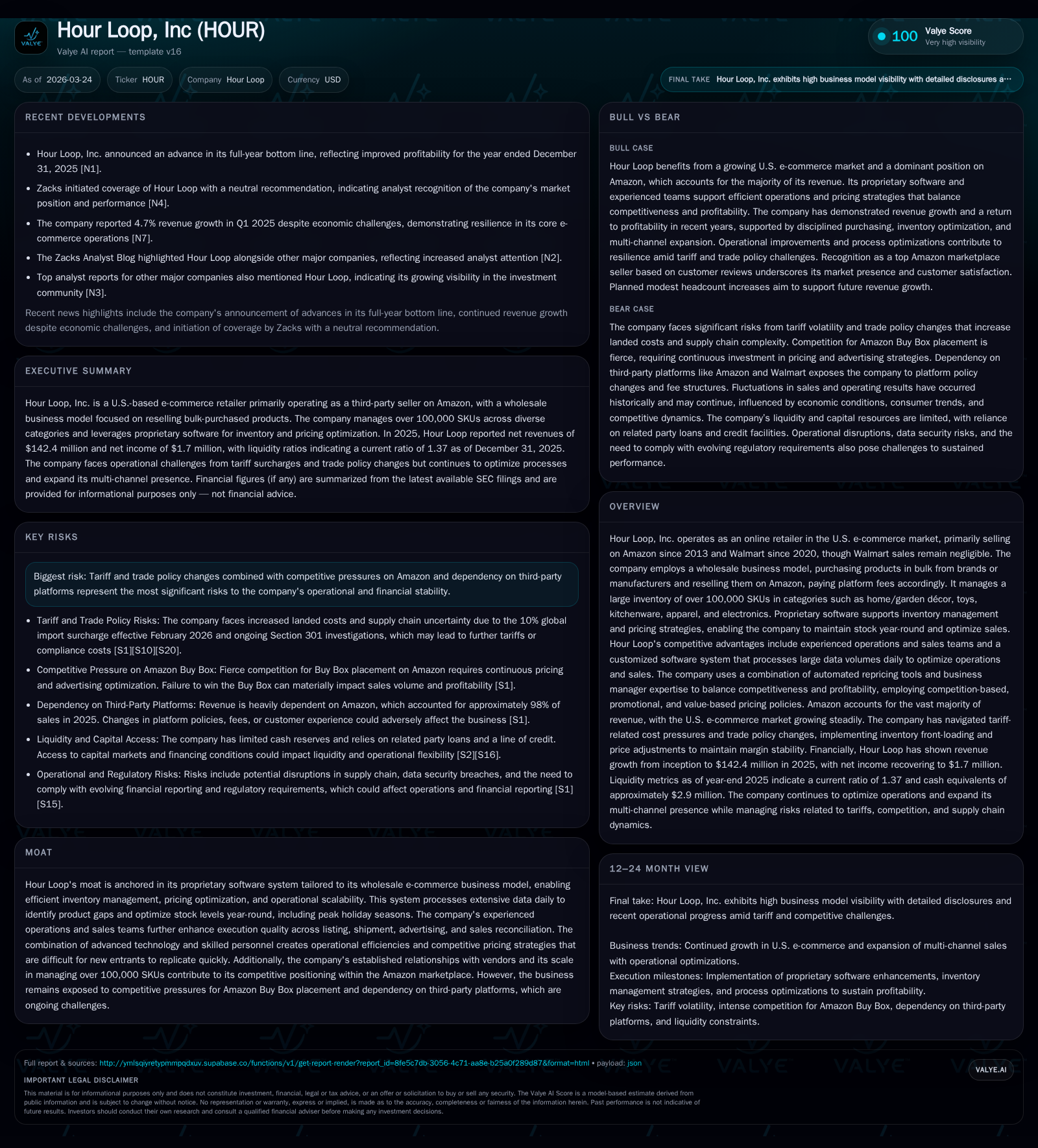

Hour Loop transitioned from multi-year operating losses to strong profitability by 2025, driven by sophisticated inventory and repricing technologies supporting over 100,000 SKUs primarily sold on Amazon. Their wholesale business model harnesses bulk purchasing advantages combined with data-driven pricing strategies to win competitive positioning amidst rising platform costs. While growth is supported by expanding SKU assortments and team scale, risks remain from heavy dependence on Amazon’s platform and recent trade policy shifts. The company's cash flow robustness and efficient capital use underpin a cautiously optimistic outlook for continued margin improvement.

Historical Growth Turnaround: From Multi-Year Losses to Positive Margin

Hour Loop’s financial journey underscores a remarkable pivot from persistent losses towards profitability. Operating income was deeply negative at -$1.92M in FY2022 and worsened to -$3M in FY2023 before recovering decisively to $0.73M in FY2024 and climbing further to $2.46M in FY2025—a staggering +236.7% YoY jump last year [F1]. This trajectory highlights effective operational leverage and scaling within their wholesale business.

Net income mirrored this pattern: after losses of -$1.48M in 2022 and -$2.43M in 2023, the company returned to profitability with $0.66M net income in 2024 and $1.7M net profit by end-2025 (+159.3% YoY) [F1]. Notably, operating cash flows reinforced this improvement, soaring from deeply negative figures (-$11.6M in 2022) to robust positive cash generation ($2.58M) by FY2025 (+724% YoY), signaling disciplined working capital strategies overcoming previous operating inefficiencies [F1].

Capital expenditures remain carefully managed within an asset-light footprint at $78K for FY2025 (up modestly from $36K prior year), consistent with usage of Amazon’s Fulfillment by Amazon (FBA) logistics network which mitigates fixed warehousing costs [F1],[S8]. Together these figures attest to a lean cost structure aligned with scaling ambitions.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 2 | 3 | 2 | 78113 | +159.3% |

| 2024 | 1 | 0 | 1 | 35996 | +127.1% |

| 2023 | -2 | -2 | -3 | 14823 | -64.4% |

| 2022 | -1 | -12 | -2 | 339518 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 3 | 24.4 |

| 2024 | 0 | 12.7 |

| 2023 | -2 | -54.6 |

| 2022 | -12 | -21.6 |

Source: SEC companyfacts cache [F1].

The Mechanics of Hour Loop’s Wholesale E-Commerce Model

Hour Loop operates predominantly as a wholesale reseller on Amazon since its inception in 2013 and more recently on Walmart since 2020 where revenues have been negligible but demonstrate intent for longer-term diversification ,[S5]. Its wholesale approach contrasts with private label or retail arbitrage common among e-commerce sellers.

Unlike private label models that require upfront product development or retail arbitrage taxing due diligence sourcing smaller quantities sporadically from varying channels, wholesale buying enables direct bulk purchase agreements with brands or manufacturers securing lower unit costs and stable supply commitments [S8]. Moreover, as a volume buyer managing over 100,000 SKUs across categories like home décor, toys, kitchenware, apparel, and electronics, Hour Loop benefits from broader vendor relationships that translate into expansive catalog depth enhancing Amazon Buy Box competitiveness.

Fulfillment is handled predominately through Amazon’s FBA program, which reduces fixed logistic overheads by offloading warehousing, inventory management, and shipping responsibilities to Amazon; however, as fees for these services rise this will pressure gross margins unless offset by operational efficiencies ([S8],[S11]). Sales fee payments to platforms like Amazon and Walmart are integral ongoing expenses that scale with revenue but also impose reliance risk. Such reliance compels continuous monitoring of listing health and customer satisfaction metrics critical for sustained Buy Box eligibility ([S1],[S11]).

Leveraging Proprietary Software as a Competitive Moat

A cornerstone of Hour Loop's market edge lies in its proprietary software tailored explicitly toward its wholesale e-commerce operations managing vast SKU volumes efficiently ,[S21],[S22]. This platform incorporates multi-dimensional data processing capabilities including automated price optimization algorithms integrating live market prices, inventory aging metrics, and projected sales velocity scenarios.

Such automation enables dynamic repricing strategies crucial for winning the Amazon Buy Box—an essential feature providing direct cart access to customers and significant sales uplift potential [S13],[S26]. The repricing engine balances aggressively competitive matching policies especially pertinent for price-sensitive categories like toys while preserving average ROI thresholds near or above industry norms of ~15%. Business managers augment algorithmic pricing with market context insights ensuring judicious margin versus volume tradeoffs.

Inventory planning also leverages software-driven gap analysis identifying stock shortages allowing proactive replenishment timing including critical Q4 holiday season stock readiness. This continuous data feedback loop fosters incremental process optimizations embedding scalability that new entrants or manual operators struggle to replicate readily.

The company states its architecture employs modern frameworks (JRuby on Rails hosted on AWS), facilitating secure multi-threaded performance aligned with operational growth demands ([S17]). These technological synergies combined with the experienced multicultural management team create substantial entry barriers anchored by scale and system integration rather than mere product offering alone.

Drivers Behind Recent Financial Performance and Operational Efficiency

The sharp improvement in operating income largely stems from both top-line expansion and rigorous cost controls as evidenced by reduced operating losses turning into profits within two years.[F1] A major driver includes scaling effects from increasing purchase volumes granting better supplier discounts offsetting inflationary pressures observed across logistics and labor markets ([N1],[N4]).

Simultaneously, the company's pricing strategy blends competition-based repricing ensuring Buy Box dominance while leveraging value-based pricing particularly during constrained inventory periods or peak demand spikes sustaining high gross margin per unit sold ([S11],[S26]). Monthly process reviews coupled with department-level KPIs help identify efficiency gaps enabling responsive expense reductions across marketing, advertising and logistics domains (). CFO trends further confirm enhanced working capital cycles reducing cash outflows evidenced by the +724% YoY improvement in operating cash flow to $2.58 million ([F1]).

However, rising Amazon fulfillment and storage fees pose margin headwinds necessitating ongoing optimization pushes to maintain profitability ledger positives.[S11],[N1] Despite this frictional cost environment, the company’s ability to maintain positive operational momentum validates its software-enabled execution model against competitors less digitally integrated.

Risks from Platform Dependency and Trade Policies

A salient vulnerability remains Hour Loop's concentrated revenue exposure via Amazon (~98%), leaving it significantly exposed to changes in platform policies affecting seller fees or listing permissions; any adverse policy change or loss of Buy Box status could materially impact revenues ([S1],[S11]). Furthermore, the recent imposition of a global import surcharge of approximately 10% effective February 24, 2026—addressing voided tariff regimes—has increased compliance burdens and cost bases unpredictably ([S9]). Section 301 investigations initiated subsequently into specific manufacturing labor practices introduce additional uncertainty around future duties though currently not expected to materially affect margins ([N1],[S9]). Termination of de minimis exemptions heightens customs compliance costs potentially disrupting inventory flow patterns tested over past years ([S9]). Labor cost pressures including minimum wage increases compound operational expenses impacting net margins if not effectively managed ([S7],[S24]). Lastly, data security vulnerabilities outlined pose reputational and financial risks should breaches occur given heavy reliance on proprietary digital infrastructure ([S19]).

Capital Allocation Profile: Cash Flow Strength and Shareholder Returns

With an estimated return on equity of roughly 24.4% as of FY2025—the ratio derived by dividing net income of $1.7 million by equity totaling approximately $7 million—the company demonstrates efficient capital utilization relative to its shareholder base ([F1]). Free cash flow stands near $2.5 million calculated as operating cash flow minus capex indicating robust internal funding capability for organic growth initiatives without pronounced external financing reliance ([F1]). Capex remains low reflecting effective outsourcing of logistics via FBA programs circumventing major fixed asset investments typical in traditional retail sectors ([F1],[S8]). As per available data,[N1] there is no mention of dividends or share repurchase programs suggesting retained earnings are primarily reinvested toward scaling operational capacity including software development enhancements or SKU expansion.

Growth Outlook: SKU Expansion and Platform Diversification Plans

Looking forward,the company signals intention to expand aggressively through increased SKU counts,fostering deeper vendor partnerships,and scaling headcount within business manager roles driving operational throughput.,[N1] While Walmart channel revenue contribution remains minimal today,the firm considers it a strategic secondary marketplace opportunity hinting at gradual diversification away from sole Amazon dependence([N1],[S5]). Underlying all growth ambitions is continued enhancement of their proprietary software tools which underpin competitive agility enabling rapid SKU onboarding,item-level margin analyses,and real-time repricing adjustments. Growth projections remain contingent on successfully navigating intensifying marketplace competition,rising platform costs,and evolving trade regulations. No explicit forward guidance is provided; hence monitoring execution against stated milestones remains paramount.

What To Watch: Marketplace Dynamics and Regulatory Landscape

Key near-term markers include potential Amazon fee structure modifications particularly regarding FBA fulfillment/storage fees which directly weigh on gross margin profiles([N1],[S11]). Tariff landscape evolution notably renewal or escalation beyond July 2026 of the Section 122 import surcharge could materially alter landed costs affecting pricing strategies([N1],[S9]). Vendor relationship stability also warrants attention given dependency on third-party manufacturers whose policy shifts could disrupt assortment continuity([S11]). Emerging labor regulation changes encompassing wage hikes or healthcare mandates may further pressurize operating expenses([S7]). Lastly,data security breach incidents would represent material risk events undermining customer trust permeating online reputation spheres([S19]). Tracking quarterly performance updates for shifts in operational metrics such as inventory turn rates,CFO fluctuations,and segment revenue breakdown will provide early signals of emerging headwinds or upside potentials.

This analysis is based exclusively on publicly disclosed financial data and regulatory filings dated up to March 24th, 2026,[F1][S#][N#] alongside Valye News proprietary sector insights contextualizing e-commerce wholesale dynamics without implying investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments