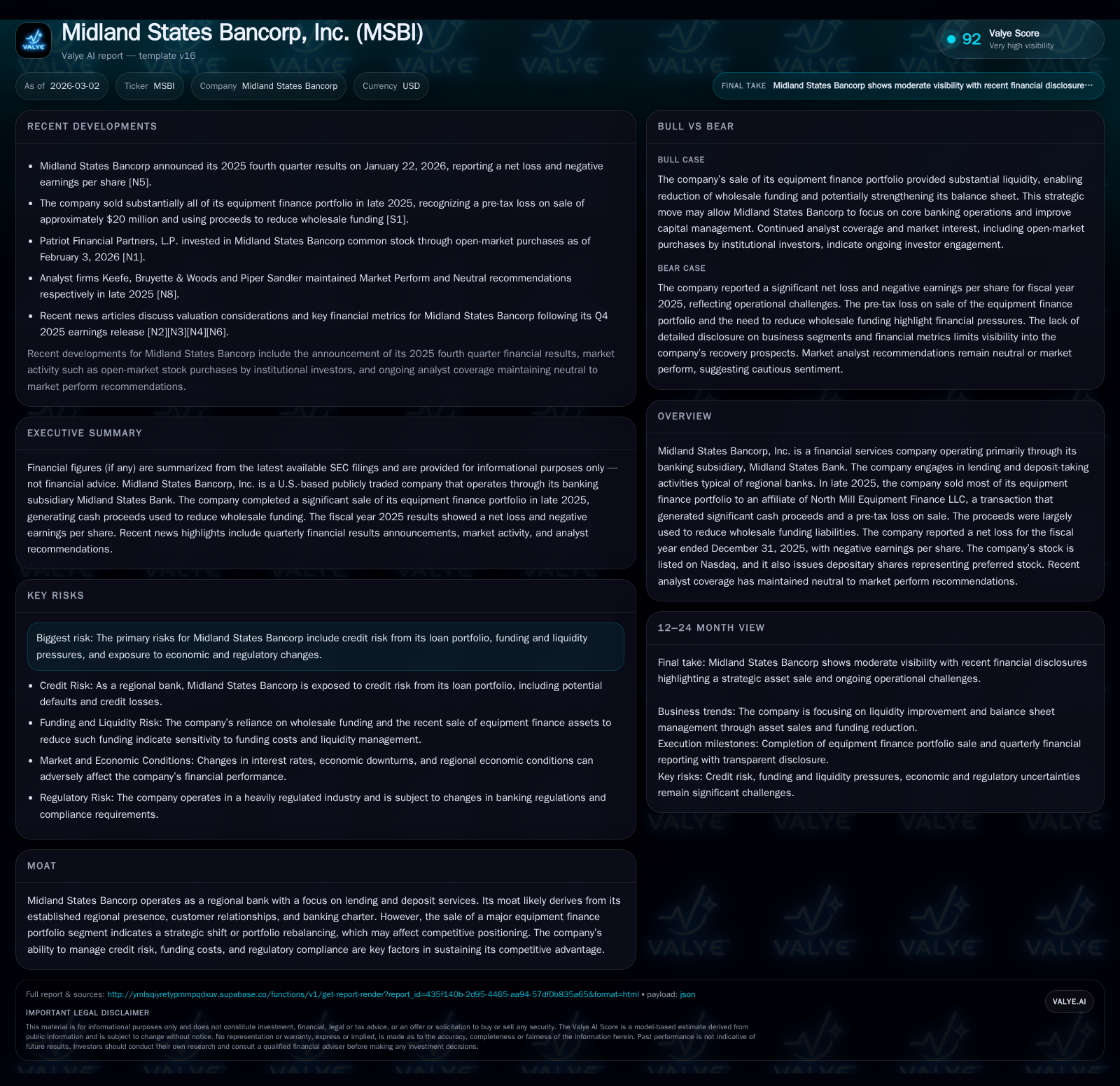

Midland States Bancorp’s Strategic Shift and Capital Realignment in 2025

The sale of a major equipment finance portfolio and wholesale funding reduction marked a pivotal recalibration for Midland States Bancorp during 2025.

In late 2025, Midland States Bancorp executed a significant divestiture of its equipment finance portfolio, generating substantial cash but recording a pre-tax loss of approximately $20 million. The proceeds were primarily deployed to reduce about $350 million in wholesale funding liabilities, reflecting a strategic refocusing on liquidity and balance sheet optimization. Despite this capital realignment, the company reported a net loss for the full year, sharply contrasting with prior profitable years and indicative of earnings volatility amid portfolio reshaping. Dividend payments persisted amidst cautious share buybacks, highlighting a balanced approach to capital allocation during ongoing sector risks.

Historical Performance and Earnings Volatility

Midland States Bancorp's financial trajectory through recent years reveals pronounced earnings volatility culminating in a stark FY2025 net loss of approximately $124 million [F1]. This represents a severe deterioration from positive net incomes of $38 million in 2024 and upwards of $75–99 million in the two preceding years, amounting to a net income decline exceeding 426% year-over-year. The precipitous drop is largely attributable to the pre-tax loss related to the strategic equipment finance portfolio sale finalized late in 2025.

Operating cash flow (CFO) similarly contracted, falling by close to 29% from about $177 million in FY2024 to nearly $126 million in FY2025, signaling constrained internal liquidity generation alongside the earnings pressures [F1]. Nonetheless, CFO remained comfortably positive, underpinning day-to-day operational needs even as headline earnings faltered.

Capital expenditures showed a modest decline of roughly 22.5% year-over-year to around $5.3 million in FY2025 from $6.9 million previously, reflecting conservative investment amid rebalancing [F1]. Total equity also diminished from approximately $711 million at end-2024 to about $565 million entering 2026, lowering estimated return on equity negatively toward -22% given net losses [F1]. Dividends maintained steady payouts near $27.7 million despite profitability challenges, whereas share repurchases moderated notably after peaking earlier, totaling less than $10 million in FY2025 [F1]. These dynamics collectively illustrate a company enduring material income disruption while preserving core operational cash flow and cautiously managing shareholder returns.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -124 | 126 | 5 | -426.7% |

| 2024 | 38 | 177 | 7 | -49.6% |

| 2023 | 75 | 155 | 9 | -23.8% |

| 2022 | 99 | 237 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 28 | 10 | 120 |

| 2024 | 27 | 5 | 170 |

| 2023 | 27 | 18 | 146 |

| 2022 | 26 | 1 | 233 |

Source: SEC companyfacts cache [F1].

Data sourced from FY filings [F1]. Negative net income in FY2025 reflects strategic divestiture impacts.

Strategic Divestiture: Equipment Finance Portfolio Sale

Midland executed a significant divestiture in late November and early December of 2025 by selling most of its equipment finance portfolio to an affiliate of North Mill Equipment Finance LLC [S7][S12][N3]. The transaction encompassed approximately $599 million in loans and leases outstanding gross ($565 million net of the allowance for credit losses), excluding retained loans approximating $75 million that Midland held back [S7]. Additionally, it included operating leases summing around $21 million within other assets.

The sale generated roughly $502 million in upfront cash proceeds subject to customary adjustments [S12], though Midland recognized an approximate pre-tax loss of about $20 million on the sale in its Q4 results reflecting transaction costs and book value write-downs [N3][S7]. This acknowledged loss underscores that while cash influx was substantial, it came at an earnings cost impacting full-year profitability.

This marked divestiture signals a clear strategic pivot away from equipment finance exposure — traditionally a higher-risk lending niche — toward streamlining the bank’s balance sheet composition [S12]. Correspondingly, the transaction aimed chiefly at bolstering liquidity and reducing dependence on more expensive wholesale funding sources.

Liquidity Management and Funding Optimization Efforts

Following the portfolio sale, Midland applied the majority of sale proceeds toward retiring approximately $350 million in wholesale funding obligations by early Q1 2026 [S7][S9][S10][S13]. Wholesale funding had posed elevated liquidity risks due to concentration and cost volatility inherent to such liabilities within regional banking models.

This liability reduction effort reflects deliberate liability management targeted at optimizing Midland’s funding profile by substituting high-cost debt with stronger deposit franchise reliance where possible [S7][S13]. While wholesale funding remains part of Midland’s capital structure, these repayments materially lower refinancing risk and improve liquidity ratios ahead of tighter regulatory scrutiny affecting regional banks broadly [S4][S5].

Recent SEC filings highlight continuing active management via periodic disclosures on debt reductions including potential maturities or issuances reported through successive Form 8-K releases [S8][S9][S10][S13], underscoring ongoing efforts beyond the one-time liability paydown tied directly to the portfolio sale.

Operational Cash Flows and Capital Expenditure Trends

Despite adverse earnings due primarily to accounting recognition related to asset sales rather than core operations' deterioration, Midland’s operational cash flow resilience stands out with positive CFO near $126 million for FY2025 [F1]. This contrasts favorably against shrinking net income showing divergence between accrual-based profit measures and actual cash generation capacity.

Capital expenditures contracted modestly relative to prior years from about $6.9 million down to $5.3 million (-22%) consistent with conservative reinvestment under current strategic caution [F1]. Computing free cash flow (CFO minus capex) yields about $120 million—demonstrating ongoing capacity for internally funded operations and potential capital returns even amid restructuring [F1].

This cash flow strength affords Midland flexibility as it navigates reduced revenue bases post-divestiture while allowing maintenance of dividends [F1] and measured share repurchases [F1], aligning capital deployment prudently with operational realities.

Future Growth Prospects: Opportunities and Headwinds

Looking ahead, Midland's growth prospects are impacted materially by its pivot away from equipment finance lines into core regional banking products mainly consisting of commercial loans and deposits [N1][N2][N4][S1][S4]. While shedding higher-risk credit segments could stabilize future loss trends over time, it concurrently removes revenue streams that had supported previous growth.

Credit risk navigation remains paramount given broader tightening conditions across lending markets influenced by inflationary pressures and changing consumer/business behaviors highlighted by company disclosures [N1][N2][S4]. The bank’s loan origination capabilities, deposit acquisition strategies, and competitive positioning within its regional footprint will be tested amid tougher macroeconomic climates.

Regulatory shifts imposing heightened capital requirements or enhanced stress testing criteria for regional lenders represent additional headwinds constraining aggressive expansion or risk-taking appetite at Midland [S4][S5]. The bank's focus appears weighted toward prudent risk management paired with bolstered liquidity rather than rapid top-line growth currently.

Analyst commentaries echo neutral-to-market perform stances reflecting cautious optimism grounded more in stabilization potential post-transformation rather than rebound scenarios at scale yet evident [N4].

Capital Allocation: Balancing Dividends, Buybacks, and Equity

Throughout FY2025’s challenging environment including net losses stemming from strategic transactions, Midland maintained relatively steady dividend disbursements paying approximately $27.7 million compared with prior years’ distributions near $27 million levels [F1][S15][S17][S22][S23]. This suggests confidence in core cash flow sustainability supporting shareholder returns despite profitability setbacks.

Conversely, share repurchases fell sharply from historical highs—dipping below $10 million—from previous years’ levels which reached close to $18 million or more before strategic adjustments commenced [F1]. Such moderation reflects prioritized capital preservation amid uncertainties rather than aggressive equity buybacks.

Equity capital balance dropped decisively correlating closely with recorded losses alongside book value effects originating from asset sales trimming total shareholders’ equity by roughly $145 million between FY2024-FY2025 [F1]. This contraction implies ROE turning negative but aligns with one-time accounting impacts flagged explicitly by management disclosures concerning divestiture charges.

Overall, Midland’s capital allocation approach evidences calibrated stewardship balancing visible dividend continuity against careful buyback tempering aligned with ongoing restructuring risk considerations.

Risk Profile: Credit, Funding, and Regulatory Factors

Per the latest Form 10-K filings focusing on risk factors impacting Midland States Bancorp, key concerns remain centered on credit risk embedded within its reconfigured loan portfolio; allowance for credit losses must be actively managed given shifted asset compositions following portfolio sales coupled with economic uncertainty across loan sectors [S4][S6].

Funding concentration risk persists despite deleveraging efforts targeting wholesale liabilities; dependence on volatile non-deposit sources sustains some degree of refinancing risk vulnerability warranting continued monitoring beyond initial reductions accomplished late-2025 [S7][S13].[S9]

Regulatory compliance inertia continues presenting challenges as evolving capital adequacy standards reflect growing supervision intensity faced by midsize regional banks amid sectorwide scrutiny; these factors necessitate sustained capital buffers limiting rapid growth levers or planning trajectories too optimistic under present regulatory frameworks [S4][S5].[S6]

These intertwined risk elements underscore why Midland adopted its recent strategic shift focused on liquidating selectively non-core portfolios while bolstering balance sheet resiliency acknowledging sector pressures common among comparable banking franchises.

What to Watch: Key Catalysts and Milestones Ahead

Investors should track several critical upcoming events shaping Midland States Bancorp’s path forward:

- Quarterly earnings releases throughout calendar year 2026 will reveal whether credit performance stabilizes following removal of bulk equipment finance exposure and will clarify margin trends post-funding adjustments preserving profitability outlooks [N3][N1].[N2]

- Additional liability management actions or opportunistic debt refinancings highlighted sporadically via SEC Form8-K filings could alter funding costs or liquidity profiles further[S9].[S10]

- Analyst coverage updates reflecting evolving market sentiment toward Midland’s revised business model provide useful gauges given their role influencing institutional interest dynamics[N4].[N6]

- Board-level governance changes such as recent directorship appointments tied to financial expertise hint at repositioning managerial oversight conducive to execution discipline during transformation phases[S17]

- Progress against deposit growth targets serves as another key metric since rebuilding retail/commercial deposit franchises can significantly mitigate repayment risks linked historically to wholesale fundings. Monitoring these factors should help contextualize Midland’s trajectory amidst strategic reset unfolding through early- to mid-2026 horizon.

This report synthesizes publicly available data sources including SEC filings dated through March 2nd, 2026,[F1], news releases,[ N#]and regulatory disclosures,[ S#]with no forward-looking estimates beyond those explicitly stated therein. It reflects an analytical perspective without investment advice or price forecasts regarding Midland States Bancorp's financial position or stock performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments