Newmark Group’s Revenue and Profit Expansion Shape 2025 Momentum

Robust growth in leasing and capital markets, along with effective refinancing, propelled Newmark's fiscal 2025 surge.

Newmark Group reported a significant acceleration in revenue and operating income in fiscal 2025, driven by expanded leasing commissions, heightened capital markets activities, and broadened management services. The company strategically navigated competitive real estate service pressures through reinforced client relationships and a diversified service mix while executing key refinancing operations to optimize its capital structure. After years of cash flow challenges, 2025 marked a meaningful recovery with positive operating cash flow and disciplined capital allocation favoring share repurchases over dividends.

Strong Financial Surge: Newmark’s 2025 Performance Unpacked

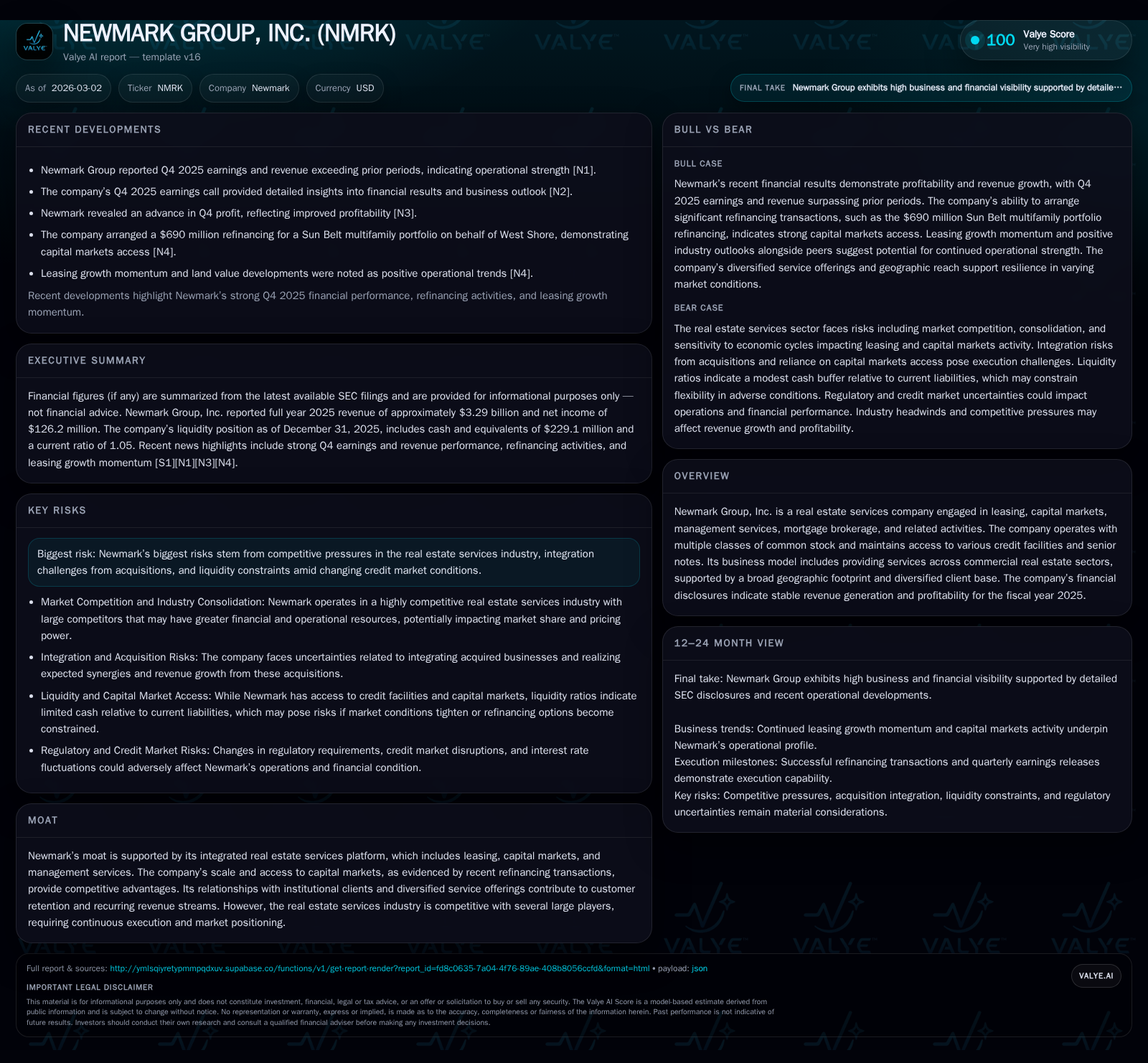

Newmark Group delivered $3.29 billion in revenue for fiscal year 2025, marking an increase of over 20% compared to $2.74 billion recorded in the previous year [F1]. This growth was primarily driven by intensified leasing commissions and capital markets transactions — core pillars of Newmark’s integrated commercial real estate service model.

Operating income rose to $234 million in FY2025 from $163 million in FY2024, reflecting a substantial 43.5% year-over-year increase [F1]. This improvement underscores enhanced commission velocity alongside effective margin management amid a competitive environment. Net income also increased significantly to $126 million — a rise of nearly 48% — demonstrating positive leverage on operating gains despite ongoing market pressures [F1].

A notable turnaround occurred in operating cash flow (CFO). After negative CFOs in recent years (-$9.9 million in 2024 and -$266 million in 2023), Newmark generated positive operating cash flow of $172 million in 2025 [F1]. This recovery indicates stabilized working capital management coupled with disciplined expense control aligned with strategic growth initiatives. Capital expenditures fell slightly by nearly 7% year-over-year to $29 million [F1], supporting free cash flow (FCF) of approximately $143 million (operating cash flow minus capex).

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3.3 | 126 | 172 | 234 | +20.3% | +47.6% |

| 2024 | 2.7 | 85 | -10 | 163 | +10.9% | +37.1% |

| 2023 | 2.5 | 62 | -266 | 125 | -8.7% | -25.1% |

| 2022 | 2.7 | 83 | 1196 | 186 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 127 | 143 | 8.6 |

| 2024 | 213 | -41 | 7.1 |

| 2023 | 37 | -321 | 5.0 |

| 2022 | 295 | 1134 | 7.0 |

Source: SEC companyfacts cache [F1].

The table above highlights Newmark's recovery path especially evident in top-line and profitability metrics.

Leasing, Capital Markets, and Service Lines: The Engines of Growth

Newmark’s diversified yet integrated services model drove its performance uptick. Leasing commissions benefited from higher transaction volumes combined with improved commission velocity—faster deal completions at healthier spreads—aligned with expanding institutional client relationships across multiple geographies [N1][N2][S1]. The firm also increased third-party property management contracts, contributing steady fee-generating recurring revenues that add stability amid transaction-based volatility.

Capital markets operations posted gains supported by stronger brokerage mandates involving debt placement, investment sales advisory, and structured finance solutions focused on multifamily assets [N1][S1]. These complex services require sophisticated underwriting expertise and access to institutional capital sources—a strength leveraged given Newmark’s scale.

This integrated approach creates cross-selling opportunities enhancing customer retention—a moat bolstered through lengthening contract durations as well as incremental revenue from ancillary services such as mortgage brokerage [S1]. The seamless interaction between leasing teams and capital markets specialists facilitates full-service coverage that competitors with narrower scopes may struggle to replicate.

Competitive Environment and Industry Challenges Facing Newmark

Newmark operates within a fiercely competitive landscape dominated by large players like CBRE and JLL alongside growing niche competitors [N7]. Technology-enabled service delivery innovation remains critical as pricing pressures persist amid industry consolidations shaping client negotiations [N7][S1]. Rigorous execution discipline is essential particularly around acquisition integration risks.

Recent commentary highlights challenges balancing volume-driven growth against margin maintenance—a delicate task reflected in Newmark's efforts to scale while preserving operational efficiencies [N7]. Its diversified geographic footprint provides resilience; however, shifts in leasing markets or tightening credit availability could constrain future growth.

Capital Structure Evolution: Refinancing Initiatives and Liquidity Profile

A key factor supporting Newmark's momentum was proactive debt maturity management through refinancing activities. In early calendar year 2026, the company arranged a $690 million refinancing for the Sun Belt multifamily portfolio on behalf of West Shore Realty Partners [N11]. This extended debt maturity while optimizing coupon costs amid an interest rate environment that remains elevated but stabilizing post-hike cycles.

SEC filings show Newmark maintains multiple revolving credit facilities alongside outstanding senior notes with staggered maturities providing liquidity flexibility [S4][S5][S10][S22]. These instruments support operational cash needs plus strategic investments or share repurchases.

Credit agreements include covenants typical for real estate services providers aimed at maintaining leverage ratios consistent with rating agency expectations—balancing growth funding availability with risk mitigation [S10]. Refinancings likely capitalize on tactical credit spread compression opportunities driven by improving investor sentiment toward commercial real estate after pandemic-related disruptions.

Returns and Shareholder Value: Balancing Buybacks against Cash Flows

From a shareholder perspective, return on equity approximated 8.6% in FY2025 based on net income relative to equity base [$126M net income / $1.46B equity = ~8.6%] [F1], indicating measured profitability within the business model.

The restoration of positive operating cash flow was critical after multi-year volatility marked by negative CFOs partly due to working capital swings linked to deal timing.

Consistent with peers prioritizing reinvestment over payout policies, dividends were not paid during recent years [F1]. Instead, share repurchases remained the primary mechanism for returning value—approximately $127 million repurchased in FY2025 versus over $212 million the prior year—reflecting prudent capital deployment amid macro uncertainties while aligning with shareholder interests [F1].

Looking Ahead: Key Indicators for Monitoring Newmark’s Trajectory

Several factors should be watched as indicators shaping future performance:

- Acquisition Integration: Execution success is vital for realizing synergies critical to scaling leasing velocity and capital markets footholds without margin dilution or service quality erosion [N2][S1].

- Leasing Market Dynamics: Contract renewal rates affect recurring revenue stability; new leasing activity signals pipeline strength amid economic cycles.

- Capital Markets Volume: Transaction activity including debt placements reflects investor appetite for commercial real estate exposure as well as interest rate impacts on underwriting spreads [N2].

- Liquidity Conditions: Access to revolving credit facilities and notes remains important amid any monetary tightening or market stress episodes.

- Competitive Positioning: Broad geographic coverage combined with technological platform enhancements will differentiate offerings within a crowded field.

In summary, Newmark’s strengthened financial foundation paired with targeted capital management provides encouraging momentum for sustaining growth despite anticipated industry headwinds. Close monitoring of operational KPIs will be essential for converting gains into lasting value creation.

This analysis is based solely on publicly available information as referenced; it does not constitute investment advice or recommendations regarding securities of Newmark Group, Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments