Omnicell's Financial Turnaround and Automation Edge in Medication Management

Omnicell pursues modest profit recovery leveraging its integrated automation platform amid healthcare budget pressures and operational challenges.

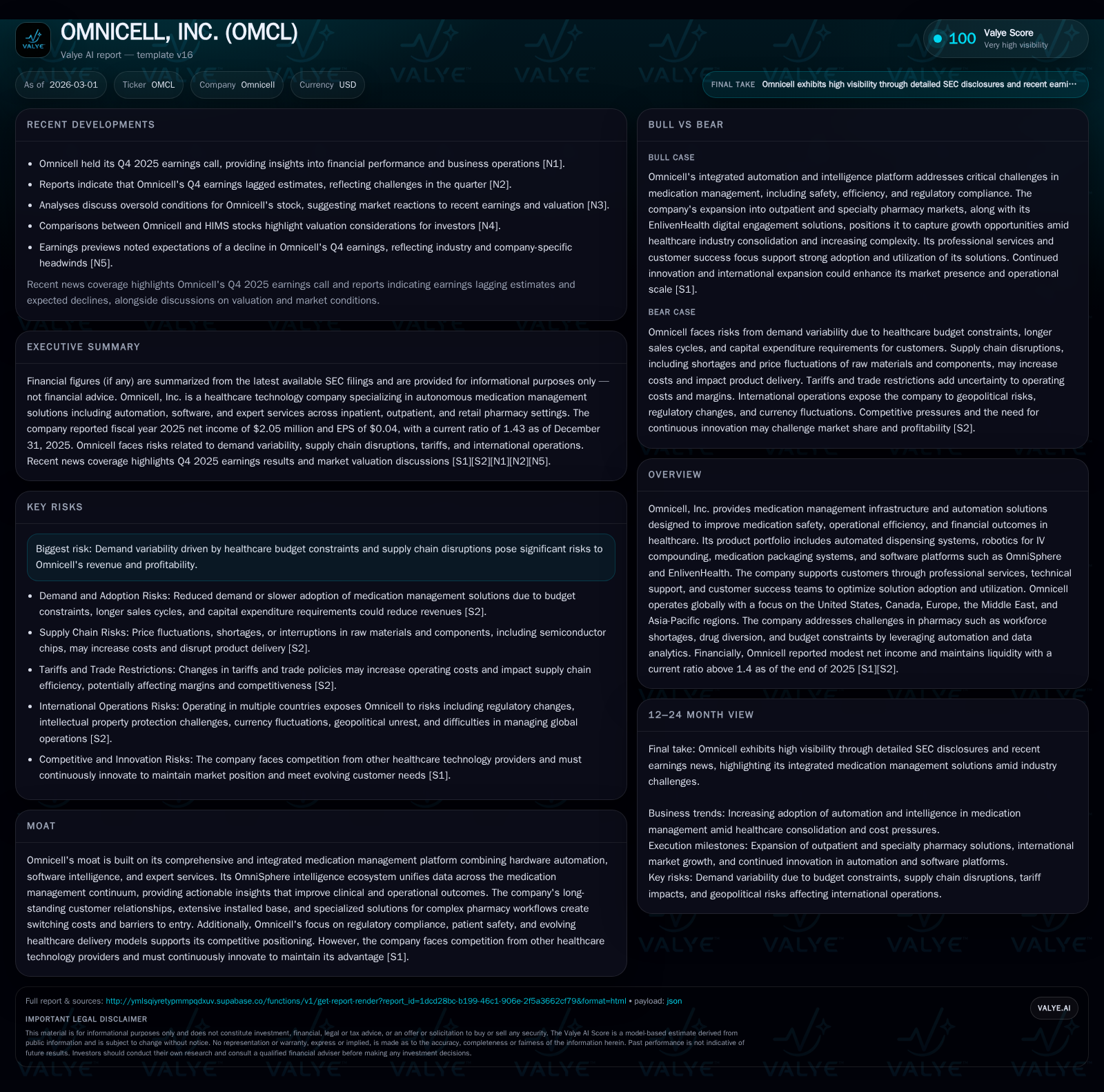

Omnicell, Inc. demonstrated fragile yet meaningful financial improvement in fiscal 2025, transitioning from prior losses to modest profitability supported by a 9.9% revenue gain. Its comprehensive medication management platform, blending automated dispensing, robotics, and the OmniSphere software ecosystem, underpins competitive positioning despite elongated sales cycles amid constrained healthcare budgets. Capital allocation in 2025 emphasized buyback program resumption and robust R&D investment to sustain innovation. However, demand variability tied to public health spending and evolving value-based care models remains a critical headwind to future growth.

Steady Growth and Turning Profits: A Look Back at Omnicell’s Recent Financials

Omnicell’s fiscal year 2025 marked a tentative financial turnaround following notable volatility in prior years characterized by losses and uneven profitability. Revenue climbed by nearly 10% year-over-year to $787.3 million, a substantial rebound demonstrating resilient demand for its medication management solutions amid macroeconomic pressures [F1]. Operating income reversed sharply from a loss of about $34.9 million in FY2023 to a modest positive result of approximately $5.16 million in FY2025 — an improvement exceeding 1400% by this metric [F1]. Despite this operating leverage, net income remained subdued at just over two million dollars, down from over $12 million the prior year, reflecting ongoing cost pressures and investment needs [F1].

Operating cash flow contracted by roughly one third relative to the prior year even as capital expenditures increased over 10%, signaling cautious but sustained investment into growth and technology platforms [F1]. This delicate balance underscores an underlying fragility in profitability recovery that Omnicell must carefully manage given uncertain healthcare spending climates.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 2 | 127 | 5 | 40 | -83.6% |

| 2024 | 13 | 188 | 0 | 36 | +161.5% |

| 2023 | -20 | 181 | -35 | 41 | -460.7% |

| 2022 | 6 | 78 | -2 | 48 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 78 | 87 | 0.2 |

| 2024 | 0 | 151 | 1.0 |

| 2023 | 0 | 140 | -1.7 |

| 2022 | 52 | 30 | 0.5 |

Source: SEC companyfacts cache [F1].

Table summarizes key financial metrics illustrating Omnicell’s path from losses toward modest profitability.

How Automation Solutions Drive Omnicell’s Market Position and Customer Retention

At the core of Omnicell’s resiliency is its medication management continuum—a carefully integrated platform combining sophisticated hardware such as automated dispensing systems and IV compounding robotics with cutting-edge software ecosystems exemplified by OmniSphere [S1, S10]. This intelligence platform consolidates operational data across dispensing points to deliver actionable insights enhancing medication safety, reducing manual errors, and improving supply chain visibility.

The complexity of pharmacy workflows in hospitals and extended care settings creates high switching costs for customers once they integrate Omnicell’s automation solutions deeply into their clinical operations [S11]. Beyond hardware installation, Omnicell invests heavily in customer education through professional services that address the nontrivial barriers of adoption faced by healthcare facilities reluctant or slow to transition from traditional manual processes [S2]. The resulting operational efficiencies target workforce shortages by reallocating clinical labor toward higher-value patient care functions while strengthening control against drug diversion—a pervasive industry issue.

Recurring revenues bolster Omnicell’s competitive moat as its solutions become embedded within broad institutional processes across multiple settings—from inpatient pharmacies to outpatient clinics—supporting usage-based billing models that align vendor incentives closely with customer success [N1].

Addressing Healthcare Budget Constraints: Challenges to Future Growth

Despite the technological sophistication of Omnicell’s offerings, growth faces real-world constraints rooted largely in capital budgets of healthcare provider organizations which remain tight amid inflationary pressures and broader macroeconomic uncertainty [S2]. Automated medication management systems typically represent significant upfront capital expenditures coupled with time-intensive implementation processes contributing to elongated sales cycles—a critical industry vernacular reflecting protracted evaluation phases requiring persistent customer education efforts before purchase decisions [S2].

The continuing shift toward value-based care models escalates these challenges by redistributing financial risk onto providers while gradually driving care delivery outside traditional hospital settings toward ambulatory or home environments where automated infrastructure investments may be less feasible or demand different modalities altogether [S29]. Tariffs on imported components further squeeze providers’ budgets affecting timing as well as scale of planned automation deployments.

Emerging Markets and Expansion: International Opportunities in Medication Management

Omnicell maintains a growing international presence spanning Canada, Europe, the Middle East, and Asia-Pacific markets where diversification offers offset potential against domestic spending headwinds [S14]. Strategic emphasis lies notably in the Middle East due to increasing healthcare infrastructure investments; however, expansion involves navigating complex regulatory landscapes demanding stringent compliance adaptations alongside managing localized supply chain risks exacerbated by geopolitical instabilities prevalent globally [S22].

These external factors introduce layers of uncertainty complicating integration efforts as automation systems must be tailored compatibly with existing health IT environments—a costly proposition mandating dedicated local expertise for successful execution.

Capital Allocation Priorities: Buybacks, Cash Flow, and R&D Investments

After a hiatus of two years without repurchases, Omnicell resumed its buyback program aggressively deploying approximately $77.6 million toward stock repurchases during FY2025—highlighting management’s confidence in balance sheet strength supported by a current ratio above 1.4 which maintains liquidity comfort levels amidst operational reinvestments [F1][S5][S23]. Free cash flow generation calculated near $86.9 million reflects prudent spend management offsetting increased capital expenditures into research & development critical for sustaining product innovation pipelines keyed toward advancing the 'Autonomous Pharmacy' vision elaborated by its ecosystem strategy [S23].

Despite this cash generation capability the company’s return on equity remains thin at about 0.2%, signaling that underlying net profitability margins are still under pressure due partly to continued legacy cost structures and evolving sales investments needed to support longer sales/buy cycle durations driven by customer budget cycles [F1].

Evaluating Risk Factors: Regulatory Compliance and Market Volatility

Omnicell operates within a complex regulatory environment subjecting it to significant legal scrutiny including exposure under federal fraud statutes such as the False Claims Act (FCA), Anti-Kickback Statute provisions, and related state laws that penalize improper billing or inducement practices irrespective of intent—a material risk dimension affecting revenue certainty and necessitating rigorous compliance frameworks across sales channels [S4][S7][S8][S12]. Whistleblower litigation (‘qui tam’ actions) poses recurring legal risk that management must vigilantly mitigate through adherence programs.

Additional risks arise from import tariffs increasing cost bases plus ongoing labor shortages impacting installation timelines for technology deployments at client sites which can delay revenue recognition or inflate project costs adversely affecting margins [S2][S13].[N3]

What to Watch: Key Milestones and Industry Dynamics in 2026

While explicit company forward guidance remains limited publicly up through early Q1-2026 reporting periods [N1], market observers should monitor quarterly margin trends closely given historical earnings variability coupled with professional services scaling up as a key lever driving broader solution adoption rates within existing accounts—an important growth vector under digitization tailwinds transforming healthcare operations fundamentally across care settings.

Competitive dynamics also warrant attention as peer technology providers push innovations potentially challenging Omnicell’s market share; thus product pipeline pacing versus regulatory approvals constitutes another critical axis determining longer-term positioning consistency [N2][N5]. Furthermore, macroeconomic developments around public health funding will materially influence decision-makers’ capital expenditure allocations shaping overall market demand trajectory.

This analysis synthesizes publicly filed SEC documents alongside recent earnings call disclosures and sector contextual understanding without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments