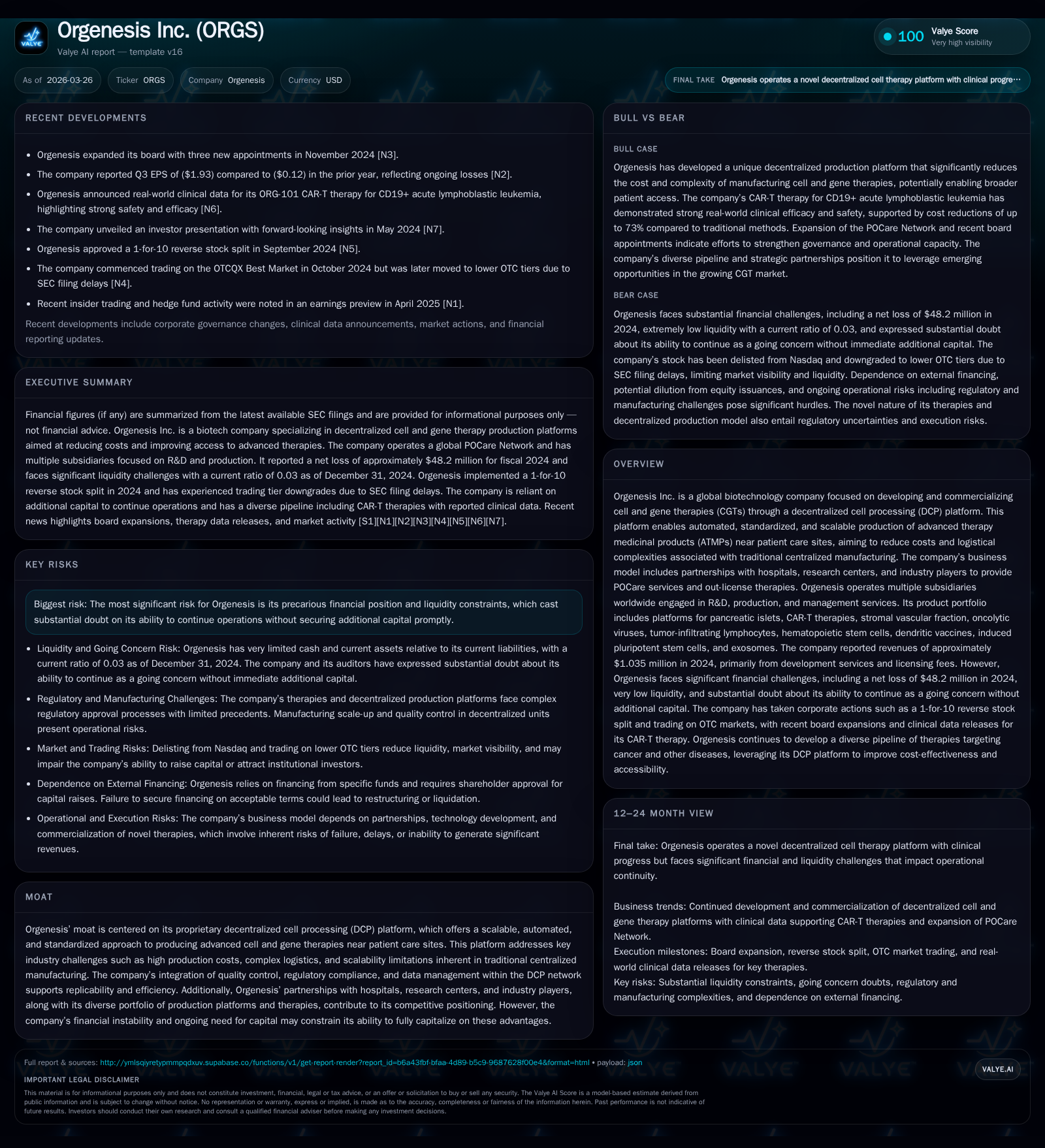

Orgenesis Inc. Confronts Liquidity Challenges While Advancing Decentralized Cell Therapy Production

Orgenesis pursues a decentralized platform for cell and gene therapies but faces severe financial constraints that cloud near-term sustainability.

Orgenesis Inc. operates a pioneering decentralized cell processing (DCP) platform aimed at scalable, automated production of advanced cell and gene therapies near patient care sites. Its innovative approach targets the high cost and logistic complexities of traditional centralized manufacturing. However, the company struggles with ongoing losses, a deteriorated balance sheet, and extremely limited liquidity, raising substantial doubt about its ability to continue as a going concern. Revenue growth has been stagnant while operational expenses and losses have expanded significantly. The firm’s future hinges on securing additional capital and successfully commercializing therapies through partnerships and decentralized manufacturing units—both of which remain uncertain.

Company Overview

Orgenesis Inc. is a global biotechnology developer targeting the rapidly evolving cell and gene therapy (CGT) market through a disruptive decentralized cell processing (DCP) platform [S1][S6]. This paradigm shifts manufacturing from conventional centralized facilities to automated modules situated near patient care sites designed to reduce cost inefficiencies, logistical complexities, and scalability limitations endemic in existing models.

Their solutions encompass platforms for autologous advanced therapy medicinal products (ATMPs), including CAR-T cells, pancreatic islets for diabetes treatment via trans-differentiation technology, stromal vascular fractions, tumor-infiltrating lymphocytes, dendritic vaccines, among others [S6][S27]. By leveraging closed system automation within Decentralized Production Units (DPUs) and Orgenesis Mobile Production Units for Local use (OMPULs), the company aims to provide harmonized quality control compliant with current Good Manufacturing Practices (cGMP) at or near point-of-care.

Orgenesis’ business model relies extensively on collaborations with hospitals, research centers, licensing partnerships worldwide responsible for clinical trial execution and commercialization in their respective territories [S6][S21]. This approach partially de-risks development by enabling POCare partners to conduct initial clinical validations while Orgenesis refines processes centrally before addressing major markets such as the US or EU.

Historical Financial Performance

Annual revenues grew sharply from approximately $7.7 million in 2020 to around $36 million in 2022 but plateaued near $34.7 million in 2023 [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2024 | -48 | -17 | -40 | +13.0% | ||

| 2023 | 35 | -55 | -15 | -54 | -3.6% | -271.8% |

| 2022 | 36 | -15 | -25 | -9 | +1.5% | +17.5% |

| 2021 | 36 | -18 | -27 | -17 | +364.0% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2024 | -17 | 128.4 |

| 2023 | -17 | 263.8 |

| 2022 | -37 | -54.0 |

| 2021 | -35 | -46.9 |

Source: SEC companyfacts cache [F1].

(Source: [F1])

Operating losses deepened considerably—from an $8.6 million loss in FY22 escalating to nearly $40 million by FY24—driven by scale-up expenses and ongoing R&D investments outside revenue growth gains [F1]. Net losses also grew correspondingly reaching over $48 million in FY24.

Operating cash flow remains negative consistently owing to burn from development activities exceeding operating income improvements; FY24 marked approximately negative $17 million CFO with capital expenditures minimal after prior large-scale investments [F1]. Notably, Orgenesis reduced capex dramatically by over 87% YoY in FY24 compared to FY23.

Equity collapsed into negative territory at about negative $37.5 million by end-2024 versus positive $27.6 million two years prior due mainly to cumulative losses wiping shareholder equity [F1].

Liquidity & Capital Structure Concerns

Liquidity presents an immediate existential threat for Orgenesis with cash dropping from approximately $0.8 million at end-2023 down toward negligible levels around $78,000 by end-2024 [F1]. Current liabilities stood at approximately $26.9 million against current assets approximating only $0.76 million introducing a perilous current ratio near 0.03—far below healthy thresholds signaling acute funding stress [F1][S4][S9].

The company had outstanding debts approximating $65 million as of late 2024 comprising convertible loans, lines of credit, related party loans among others; recent repayments were limited (~$6 million post-period) [S4]. Management disclosed active pursuit of expense reduction measures alongside urgent attempts at securing fresh financing [S4], yet substantial doubt remains about viability absent new capital infusions.

Business Model & Product Portfolio

Orgenesis operates primarily through two intertwined verticals:

- POCare Platform: A global network delivering decentralized CGT manufacturing near patients using standardized protocols enabling harmonized clinical trials and scalable output [S6][S21].

- Therapeutic Portfolio & Licensing: Broad pipeline focused on personalized autologous cell therapies including pancreatic islet regeneration for diabetes via trans-differentiation technology licensed from THM under strict milestone agreements [S25]. Other areas include CAR-T immunotherapies, stromal vascular products for regenerative medicine, and emerging extracellular vesicle-based technologies protected under pending patents [S24][S27].

This network-based licensing model distributes development risk while positioning Orgenesis as both technology licensor and service provider facilitating clinical trial supply chains through Octomera LLC subsidiaries specialized in bio-isolator based manufacturing automation [S21]. Revenue sources blend recurring service fees with royalties typically around 10% of net sales generated by partners [S6][S21].

Growth Prospects & Strategic Drivers

Substantial growth depends on:

- Expanding deployment of Decentralized Production Units (DPUs/OMPULs) creating localized supply chains for CGTs.

- Demonstrating clinical proof-of-concept from partner-led regional trials validating therapeutic efficacy particularly for autologous ATMPs such as diabetes therapy enhancing endogenous insulin production [S25][S27].

- Obtaining regulatory approvals facilitating commercialization especially in major markets requiring stringent cGMP compliance within decentralized hubs [S26].

- Securing meaningful licensing deals leveraging proprietary IP including EV technologies with potential dermatological indications extending patent life into mid-century [S24].

- Enhancing automation via AI-driven microfluidics integrated in production platforms supported by European Innovation Council grants for iPSC manufacturing capabilities [S11].

Challenges include supplier dependencies for complex manufacturing equipment; evolving multi-jurisdictional regulatory frameworks; competition from larger biopharma companies with deeper resources; and ongoing intellectual property litigation risks tied to license agreements [S17][S20][S25].

Risk Factors & Regulatory Environment

The most pressing risk remains financial sustainability given steep cash burn amid minimal liquidity leading auditors and management alike to express substantial doubt about going concern status as reported at December 31, 2024 [S1][S4][F1]. Failure to raise timely capital could lead to operational curtailments or bankruptcy.

Developmental risks are pronounced given reliance on innovative autologous therapies like trans-differentiation approaches facing uncertain regulatory pathways partly due to novelty and required long-term follow-up studies [S25][S26]. Additionally:

- Liability claims could arise due to unforeseeable side effects or manufacturing defects exposing the company to costly litigation or regulatory actions potentially hindering commercialization efforts [S7][S10][S15].

- Lack of internal marketing or sales infrastructure compounds uncertainty over product revenue generation post approval necessitating effective partner collaboration for commercialization execution [S15][S19].

- Intellectual property challenges remain an active threat with competitors or licensors pursuing infringement claims potentially imposing royalty burdens or injunctions restricting operations [S15][S20][S22].

- Cybersecurity vulnerabilities plus evolving data privacy regulations present business continuity hazards alongside reputational risks affecting investor confidence or customer trust [S15][S23].

- Environmental health safety regulations concerning use/disposal of hazardous materials used in cell processing could entail costly compliance upgrades impacting margins if tightened further [S12][S13].

Capital Allocation & Returns Discussion

Due largely to heavy investment requirements aimed at R&D scale-up alongside commercial infrastructure establishment efforts currently yielding no profits nor free cash flow positive periods over recent years examined [F1], Orgenesis's cash flow situation deteriorated with CFO moving from –$25 million range historically toward –$17 million despite slashed capital expenditures approximating just $260 thousand in FY24 hinting at curtailed asset investment likely aimed at conserving cash amidst liquidity crises; yet operational expenses remain elevated driving continued net losses nearing –$48 million annually underscoring deficit financing needs without tangible capital returns [F1].

Return on equity appears significantly negative driven primarily by erosion of equity base into deeply negative territory reflecting accumulated losses rather than operational efficiency metrics; this indicates no current value creation measurable through earnings [F1].

No dividends or share buybacks have been executed due primarily to ongoing need for cash preservation given precarious balance sheet circumstances [F1][S4]. Future capital returns will depend entirely on achieving sustainable profitability requiring successful pipeline product launches alongside prudent financial management.

Outlook & What To Watch For (Analysis)

Absent explicit forecast guidance disclosed publicly by Orgenesis within available filings or news releases, key upcoming milestones likely critical include:

- Achievement of regulatory clearances permitting commercial launch of flagship autologous therapies developed under the trans-differentiation platform.

- Expansion velocity of DPUs globally creating modular capacity enabling cost-efficient localized production away from centralized facilities.

- Progression updates from regional partner clinical trials validating safety/efficacy encouraging broader licensing uptake.

- Successful closing of financing rounds improving liquidity profile sufficient to fund operations beyond short term.

- Developments regarding resolution or impact of ongoing IP litigation cases influencing licensing freedom or royalty burdens.

- Scaling automation enhancements especially integration of AI-enabled microfluidic technology enhancing yield uniformity underpinning competitive differentiation.

Overall Orgenesis stands at a critical juncture balancing innovative technical progress against stark funding realities threatening near-term survival absent swift remedial action.

This analysis is informational based on publicly available financial disclosures and company filings as of March 26, 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments