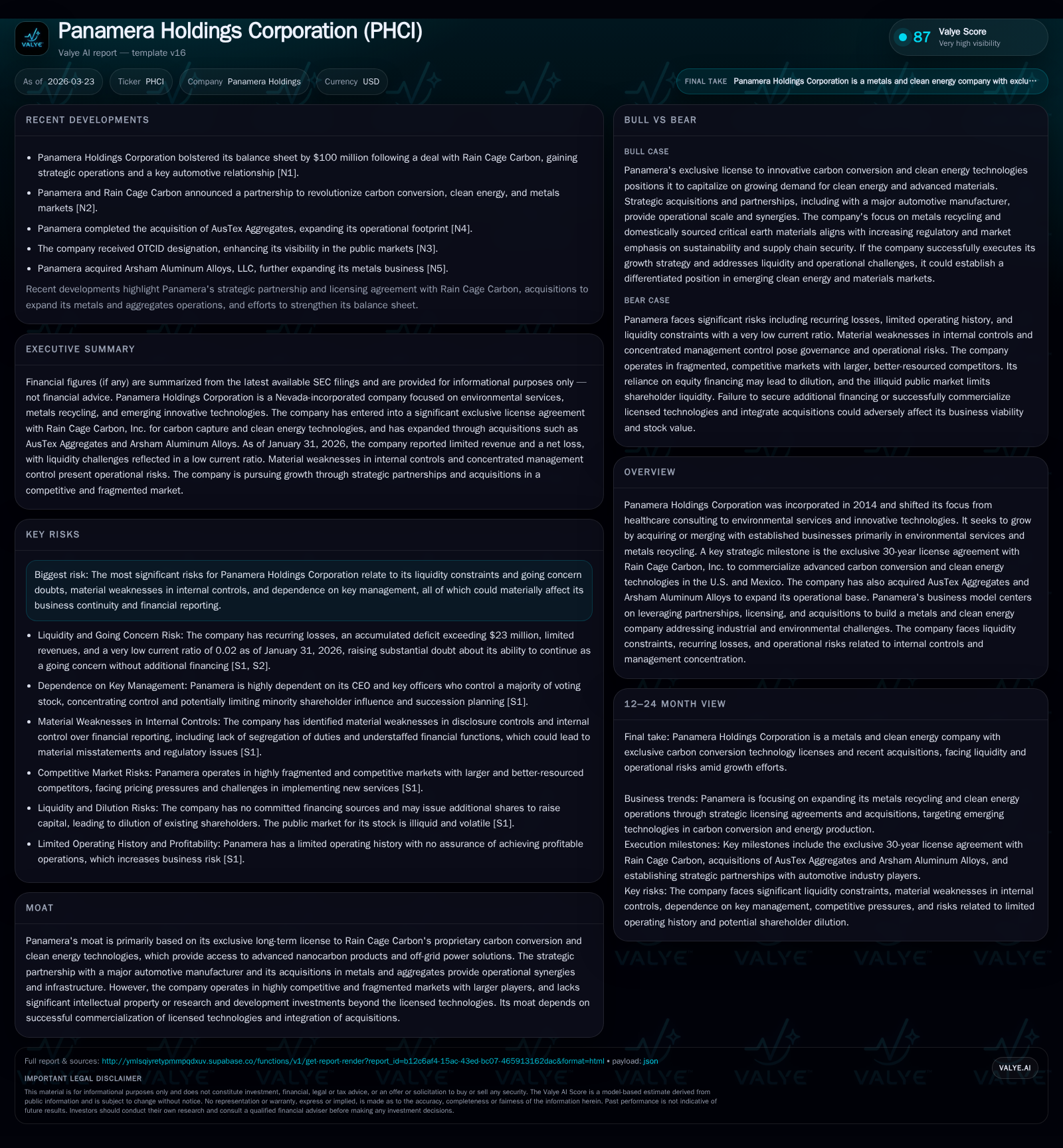

Panamera Holdings’ Transition from Healthcare Consulting to Advanced Metals Recycling and Clean Energy Integration

Panamera Holdings has pivoted from healthcare consulting toward environmental services with a heavy focus on carbon conversion technology and metals recycling amid severe liquidity challenges.

Originally founded in 2014 as a healthcare consulting firm, Panamera Holdings Corporation has undergone a strategic transformation targeting environmental services and advanced clean technologies, chiefly through an exclusive license for Rain Cage Carbon’s carbon conversion technology. Despite achieving dramatic revenue growth—over 20-fold from FY2024 to FY2025—the company continues to operate at a loss with persistent cash flow deficits and looming liquidity constraints raising substantial going concern doubts. Acquisitions like AusTex Aggregates and Arsham Aluminum Alloys underpin expansion efforts, but integrating these assets and commercializing cutting-edge licensed technologies remain significant challenges amid high operational and governance risks.

From Healthcare Consulting to Environmental Innovation: Evolution of Business Strategy

Panamera Holdings Corporation was founded in 2014 originally as Panamera Healthcare Corporation, dedicated to offering consulting services within healthcare organizations [S1]. However, by late 2021 the company undertook a decisive pivot, rebranding itself as Panamera Holdings Corporation with a broadened objective: pursuing business opportunities primarily within environmental services and innovative clean technologies [S1][F1]. This transition reflects a shift away from professional services toward industrial sectors focused on sustainability-driven themes such as metals recycling and carbon capture.

A central element of this new strategic direction is Panamera’s exclusive nationwide license agreement—spanning 30 years—with Rain Cage Carbon, Inc., signed in August 2025 [S1][N/A]. This license grants Panamera rights to commercialize advanced carbon conversion and clean energy technologies developed by Rain Cage Carbon across the U.S. and Mexico. These technologies reportedly enable the transformation of CO₂ emissions into valuable nanocarbon products along with off-grid power generation solutions. Alongside licensing arrangements, Panamera has pursued operational scale via acquisitions in metals supply chains including AusTex Aggregates and Arsham Aluminum Alloys [S1][S4]. Such moves aim to integrate high-potential green tech IP with tangible production assets.

This approach notably relies more on partnerships and licensing arrangements than in-house R&D investments, positioning Panamera as a conglomerate builder targeting fragmented markets for recycled critical earth materials and sustainable energy production [S1][F1]. The absence of own significant intellectual property beyond licensed tech highlights dependence on the success of Rain Cage Carbon’s innovations for future competitiveness.

Examining Historical Financial Trends: Revenue Growth Coupled with Persistent Operating Losses

Financially, Panamera exhibits a striking contrast between rapid revenue expansion and sustained losses. According to reported figures, total revenues climbed sharply from just $11.3K in FY2024 to $241.4K in FY2025—an eye-catching increase exceeding 2,000% year-over-year [F1]. Earlier fiscal years showed minimal but growing receipts: $41.7K (FY2022) and $100K (FY2023). Such growth reflects early commercialization efforts tied potentially to new licensing deals and acquisitions commencing around FY2024–FY2025.

However, this top-line growth masks ongoing operational inefficiencies. Operating income remained deeply negative throughout this period despite improvement from very large losses: operating losses reduced from roughly -$15.2M in FY2024 to about -$546K in FY2025 [F1]. Net income tracked similarly with net losses narrowing yet still substantial: nearly -$15.2M FY2024 down to -$536K FY2025. These figures yield an approximate negative return on equity (ROE) near -86% as of FY2025 given reported equity levels [F1].

Operating cash flows continue at large deficits ($-515K FY2025), underscoring an inability to self-fund operations or expansions reliably [F1]. The lack of positive free cash flow further indicates persistent funding challenges requiring external capital injections.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 241430 | -1 | -515320 | -1 | +2032.2% | +96.5% |

| 2024 | 11323 | -15 | -99380 | -15 | -88.7% | -114.0% |

| 2023 | 100001 | -7 | -98071 | -7 | +140.0% | -20827.8% |

| 2022 | 41666 | 0 | -29261 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -85.9 |

| 2024 | 8371.2 |

| 2023 | -14330.1 |

| 2022 | 71.5 |

Source: SEC companyfacts cache [F1].

Revenue surged dramatically but was accompanied by persistent high operating losses.

Commercialization of Rain Cage Carbon Technologies: The Growth Engine and Its Uncertainties

The core strategic asset underlying Panamera's transition is its long-term exclusive license for Rain Cage Carbon’s proprietary carbon capture and conversion technologies [S1][N/A]. These technologies involve converting industrial CO₂ emissions into commercially valuable nanocarbon materials while enabling localized renewable energy production solutions — innovations positioned at the intersection of emerging decarbonization efforts and resource circularity.

However, commercialization risks are considerable. Panamera lacks independent R&D efforts outside the licensed technology realm [S10], making successful market development highly dependent on Rain Cage’s technical maturation and acceptance within competitive metals recycling and clean energy markets plagued by larger players with entrenched capabilities [S4]. Adoption timelines inherent in cutting-edge cleantech further compound uncertainty over meaningful near-term revenue ramp.

Moreover, progressing from pilot deployments—which appear underway per company statements—to scalable commercial contracts is fraught with execution hurdles common in industrial innovation cycles such as supply chain development and regulatory compliance [S7]. The potential benefit derives largely from rare access to patented process advantages that may unlock domestic sourcing of critical earth materials; yet these cannot be assured without sustained investment bolstering application breadth.

Operational Expansion through Strategic Acquisitions: Synergies and Integration Challenges

Augmenting its licensing strategy are recent acquisitions aimed at vertically integrating materials supply infrastructure — notably AusTex Aggregates and Arsham Aluminum Alloys [S1][S4]. Such assets could provide foundational throughput capacity aligned with recycled metal recovery and aggregate supply lines intrinsic to carbon conversion outputs.

Nonetheless, acquisition-led growth introduces complexity risks common among smaller firms attempting diversification under financial strain [S17]. Integration challenges include aligning disparate corporate cultures; harmonizing regulatory compliance frameworks especially related to environmental laws; addressing any inherited contingent liabilities; managing cost structures subject to fluctuating demand; plus preserving key personnel incentivization post-acquisition [S7][S17].

Cost absorption pressures combined with limited operational scale put additional strain on margins while magnifying execution risk during these early consolidation phases.

Liquidity Constraints and Going Concern Questions: Financial Stability under Pressure

The company faces stark liquidity challenges reflective in its virtually nonexistent current ratio measured at approximately 0.02 as of January 31, 2026 — signaling extreme difficulty meeting short-term obligations solely through liquid assets [F1]. Total current liabilities dwarf current assets (approx. $4.25M liabilities vs $81K assets) evidencing substantial working capital stress.

An accumulated deficit exceeding $23 million includes sizeable non-recurring impairments ($7.5M) and stock-based compensation charges ($14.5M) that distort some loss components; however recurring losses persist independently [S1][F1]. Operating cash flows remain negative across multiple years ($-515K in FY2025 alone), necessitating continuous reliance on equity financing rounds or related party advances just to fund baseline operations [S9][F1].

Auditors have explicitly raised going concern doubts linked directly to these liquidity pressures; management openly acknowledges the risk that failure to raise additional capital could force severe scaling back or termination of business plans [S9][S12]. In a challenging capital market environment marked by illiquidity for small-cap OTC entities like Panamera’s shares this constraint represents a critical existential threat.

Capital Structure, Equity Dynamics, and Absence of Dividends: Implications for Shareholders

Capital structure features include authorization for up to 600 million shares split between common (550 million authorized) and preferred stock (50 million authorized). As of late 2025 approximately 79.9 million common shares outstanding exist with no preferred shares issued so far [S3][F1].

Significantly though the board maintains authority to issue preferred stock without shareholder approval — a governance mechanism that could dilute common stockholders materially if deployed strategically by management [S3][S11]. Likewise additional common shares can be issued at management discretion leading potentially to sizable dilution effects particularly given ongoing funding reliance on equity raises.

CEO T. Benjamin Jennings alone beneficially owns nearly 29% of outstanding common shares granting him effective control over voting matters including director elections or corporate transactions [S5]. This concentration limits minority shareholders’ influence over corporate governance outcomes while amplifying risk that decisions may reflect majority holder interests above others.

The company has never paid dividends historically nor does it plan any foreseeable dividend distribution given its focus on reinvesting earnings or raised capital toward growth objectives [S3]. This positioning diminishes appeal for income-oriented investors seeking yield stability.

Risks in Governance and Control: Management Consolidation and Reporting Weaknesses

Several operational risk flags emerge from governance disclosures highlighting material weaknesses in internal controls over financial reporting identified during fiscal year end July 31, 2025 [S4][S6]. Such deficiencies imply heightened exposures including inaccurate financial data compilation or reporting delays — factors that can undermine investor confidence.

Further complicating governance dynamics is the absence of independent audit or compensation committees as disclosed — raising concerns about oversight quality over executive remuneration or financial audit rigor as required under standard Sarbanes-Oxley expectations for listed entities [S16].

Concentrated executive power combined with deficient procedural controls creates an environment where minority shareholders face structural disadvantages when seeking accountability or transparency enhancements.

Outlook Considerations: Key Metrics to Watch and Potential Triggers for Value Realization

While explicit guidance has not been provided by management concerning detailed upcoming milestones [N/A], several focal points warrant monitoring:

- Progress achieving commercial scale deployments using Rain Cage Carbon’s licensed technology including contract wins or supply agreements;

- Successful integration outcomes following acquired assets realization toward incremental operating revenue contributions;

- Trajectory changes in operating cash flow including potential moves toward breakeven cash generation;

- Capital raises efficiency marked by terms minimizing shareholder dilution while providing sufficient runway coverage;

- Remediation actions addressing internal control weaknesses potentially restoring stronger governance credibility;

- Resolution or material developments relating ongoing litigation matters such as shareholder disputes that could impact reputation.

Prospective investors or analysts will benefit from closely observing quarterly filings for qualitative updates around commercialization activities plus liquidity metrics due to their outsized impact on viability assumptions going forward.

Disclaimer: This analysis is prepared solely for informational purposes based on publicly available data without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments