Revumenib and Collaboration Dynamics Shape Syndax Pharmaceuticals’ 2025 Performance

Syndax Pharmaceuticals reported strong revenue growth driven by FDA-approved oncology therapies and their collaboration with Incyte, despite sustained net losses and considerable R&D investments.

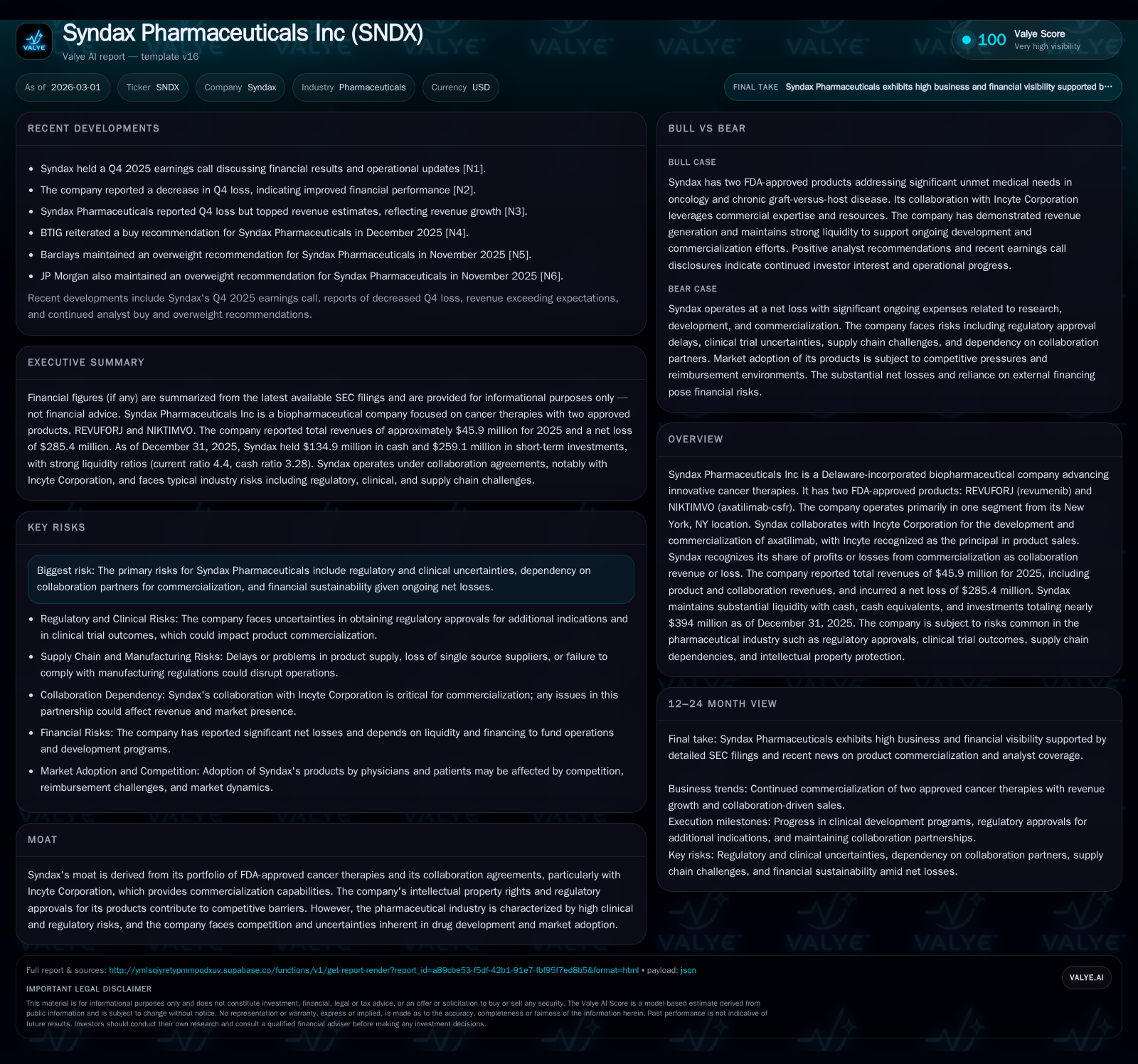

In 2025, Syndax Pharmaceuticals marked a pivotal year transitioning from a development-stage biotech to a commercial-phase company with revenues surging 72.8% year-over-year. This growth was primarily fueled by two FDA-approved cancer therapies, REVUFORJ (revumenib) and NIKTIMVO (axatilimab-csfr), alongside the strategic collaboration with Incyte Corporation that supports commercialization efforts. Although operating losses improved by nearly 20%, Syndax's net loss remained substantial at $285.4 million, reflecting ongoing high R&D expenditures and scale-up costs. The company sustains robust liquidity with over $394 million in cash, cash equivalents, short-term deposits, and investments but must carefully navigate regulatory risks and dependency on partners to sustain its commercial momentum and fund future pipeline advancements.

Surging Revenues from FDA-Approved Oncology Therapies

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -285 | -323 | -273 | 187000 | +10.5% |

| 2024 | -319 | -275 | -340 | -52.3% | |

| 2023 | -209 | -161 | -230 | 0 | -40.2% |

| 2022 | -149 | -134 | -152 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -323 | -441.6 |

| 2024 | -110.6 | |

| 2023 | -161 | -37.8 |

| 2022 | -134 | -31.9 |

Source: SEC companyfacts cache [F1].

Syndax Pharmaceuticals' transition from a development-focused biotech to a commercial-stage company was exemplified in its 2025 financial results. Total revenue for the year increased by 72.8% compared with prior years [F1], propelled principally by sales of its two FDA-approved oncology products: REVUFORJ (revumenib) targeting acute leukemia subtypes, and NIKTIMVO (axatilimab-csfr), approved for chronic graft-versus-host disease treatment [S14][N2]. This shift has moved revenue recognition away from milestone payments toward product sales combined with collaboration profit shares.

Drivers Behind Syndax’s Top-Line Growth and Operating Loss Trends

Despite notable revenue gains, operating losses improved by about 19.6% year-over-year but remained large at -$273 million in 2025 [F1]. Net loss totaled -$285.4 million for the same period [F1], reflecting substantial investment in R&D—encompassing clinical trial costs across multiple pipeline candidates—and marketing, selling, general administrative expenses associated with initial commercialization stages.

These results underscore the high operating leverage typical of oncology biopharmaceutical companies advancing novel therapies.

The Strategic Role of the Incyte Collaboration in Market Penetration

Central to Syndax’s recent performance is its collaboration agreement with Incyte Corporation concerning axatilimab’s development and commercialization [S14][N2]. Under this arrangement, Incyte acts as principal in product sales within the U.S., managing primary sales channels while sharing profits or losses equitably with Syndax.

Per ASC Topic 808 governing collaboration arrangements, Syndax records its share of net profits or losses as "collaboration revenue, net," distinct from direct product revenues [S20]. This structure grants access to Incyte’s established commercial infrastructure but aligns Syndax’s revenue recognition closely with joint performance outcomes.

Cash Flow Profile and Capital Structure Amid High R&D Investments

The company’s operating cash flow was negative approximately $323 million during 2025 [F1], signaling continued heavy investment in late-stage drug development and early commercialization activities. Capital expenditures were minimal ($187 thousand) indicating outflows largely consist of operating expenses rather than fixed asset acquisitions.

As of December 31, 2025, Syndax maintained a strong liquidity position with combined cash, cash equivalents, short-term deposits, and investments exceeding $394 million [S8][F1], supporting operational needs despite ongoing net losses. The current ratio stood around 4.4, reflecting solid short-term financial flexibility [F1].

Additionally, royalty interest financing agreements provide upfront capital via sale of future royalties on NIKTIMVO sales; this debt-like instrument carries an effective annual interest rate near 9%, adding recurring financing costs that impact net results [S16][S23].

Risks and Regulatory Challenges Ahead

Regulatory uncertainty remains a fundamental risk alongside typical clinical trial execution hazards inherent in biopharmaceutical innovation cycles [S4][S12][N1]. Dependency on partners such as Incyte for U.S. commercialization introduces operational risk layers; any disruption could affect market penetration effectiveness and revenue streams [S26]. Competitive pressures within oncology therapeutics necessitate continuous innovation to sustain differentiation.

Outlook: Key Milestones to Monitor

While explicit forward guidance is limited publicly [N1][N3], indications point toward focusing on scaling commercial uptake of REVUFORJ and NIKTIMVO alongside advancing clinical trials aimed at label expansions or new indications. Upcoming regulatory decisions and milestone achievements under licensing agreements will be critical drivers for validating growth trajectory.

Capital Allocation Considerations

Reflecting its developmental stage profile, Syndax has not declared dividends or repurchased shares recently [F1][N2]. Equity financing along with royalty interest liabilities tied specifically to NIKTIMVO revenue streams underpin the company's capital structure strategy during early commercial expansion phases [S16][S23]. Negative return on equity (~-441.6%) aligns with high net losses relative to shareholder equity—a common feature among biopharma firms investing extensively in pipeline development while scaling commercialization efforts [F1].

This analysis is based strictly on publicly filed financial statements and verified news sources without speculative projections or investment recommendations regarding Syndax Pharmaceuticals Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments