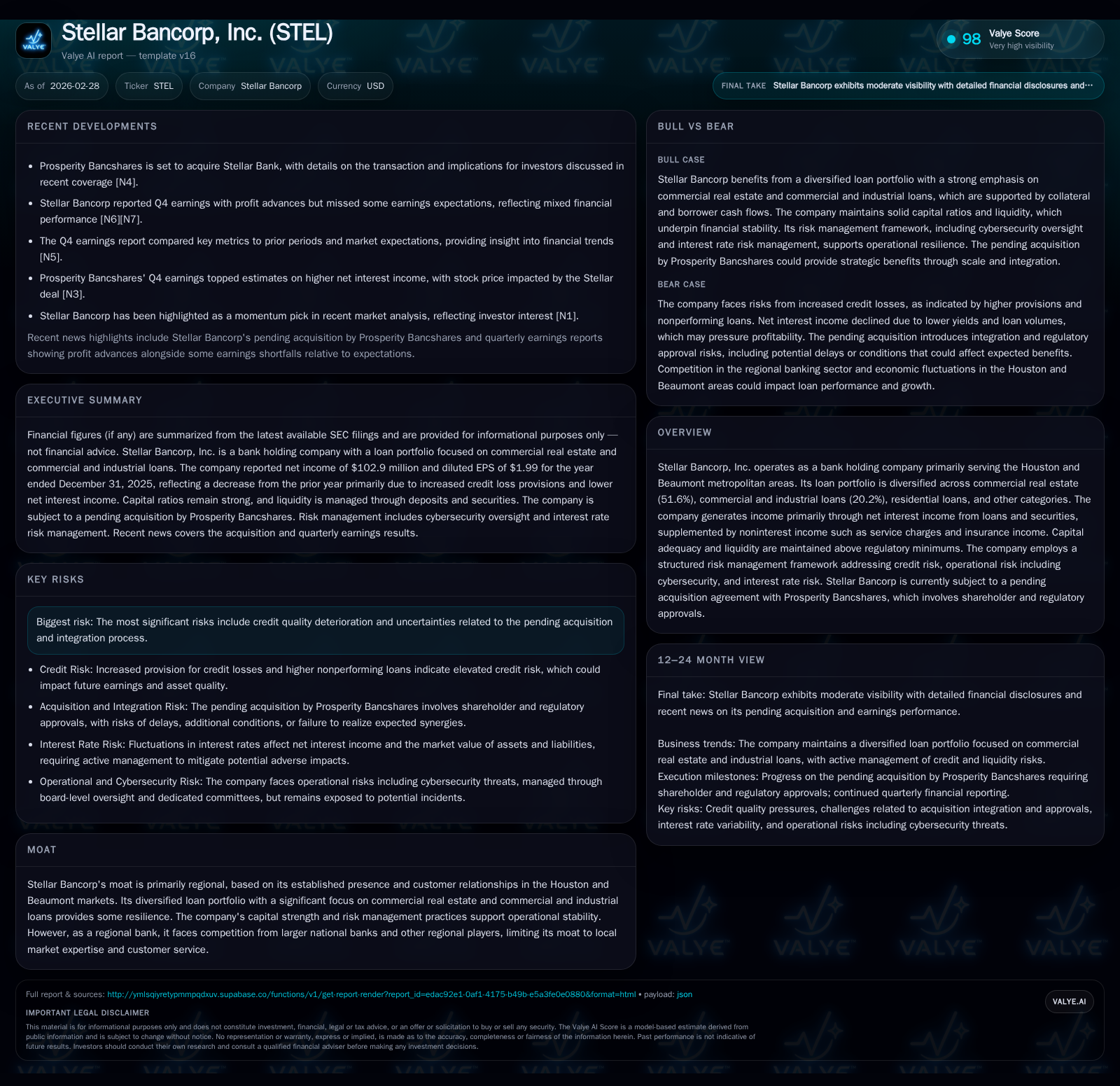

Stellar Bancorp’s Earnings and Capital Strategy Under Acquisition Pressure

The bank’s profit and loan growth face challenges as it manages disciplined capital strategy amidst a pending acquisition.

Stellar Bancorp experienced a notable decline in net income of 10.5% in 2025, pressured by increased credit loss provisions and lower net interest income despite modest funding cost improvements. Its loan portfolio remains heavily weighted toward commercial real estate, while credit quality risks have risen alongside nonperforming assets. The company sustains strong capital adequacy above regulatory minimums, supports dividends with an increased buyback program, and reinforces risk governance with enhanced cybersecurity focus. However, the pending acquisition by Prosperity Bancshares introduces execution uncertainties and weighs on near-term growth prospects within its regional Houston-Beaumont banking footprint.

Financial Performance Review: Trends Across 2023-2025

Stellar Bancorp reported a net income of $102.9 million for the year ended December 31, 2025, marking a 10.5% decline from $115.0 million in 2024 [F1][S1]. This reduction was primarily driven by a $13 million increase in provision for credit losses alongside a $6.4 million decrease in net interest income despite lower interest expenses on liabilities.

Net interest income before provisions stood at $401.6 million in 2025 compared to $408.0 million the prior year, impacted by a slight contraction (approximately 0.6%) in average interest-earning assets due mainly to reduced loan balances partially offset by improved funding costs [S1]. Interest income decreased by 4.6%, reflecting yield compression influenced by purchase accounting adjustments and lower yields on loans (6.68% in 2025 versus 6.89% in 2024).

Efficiency ratios modestly worsened to 62.28%, reflecting slightly higher expense relative to combined net interest and noninterest income despite a $3.5 million reduction in noninterest expense [S1]. Return on average equity declined from 7.34% to approximately 6.34%, signaling profitability pressures amid stable capital levels.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 103 | 97 | 4 | -10.5% |

| 2024 | 115 | 133 | 5 | -11.9% |

| 2023 | 130 | 168 | 7 | +153.7% |

| 2022 | 51 | 109 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 29 | 73 | 93 |

| 2024 | 28 | 3 | 128 |

| 2023 | 28 | 0 | 161 |

| 2022 | 15 | 24 | 105 |

Source: SEC companyfacts cache [F1].

This financial snapshot underscores decelerating earnings alongside significant reductions in operating cash flow likely related to tighter lending activity or margin compression.

Loan Portfolio Dynamics: Commercial Real Estate Concentration and Credit Quality

At December 31, 2025, Stellar's loan portfolio totaled approximately $7.30 billion with commercial real estate (including multi-family residential) representing about $3.77 billion or roughly 51.6% of total loans—a slight decrease from $3.87 billion at year-end 2024 [S19][S20]. Commercial & industrial loans comprised about $1.48 billion, indicating selective growth within this segment.

Loan reductions were noted particularly within commercial real estate construction & land development and residential construction categories—reflecting cautious underwriting amid sector headwinds [S19][S22].

Credit quality pressures surfaced as nonperforming assets rose to $60 million (0.56% of total assets) from $39 million (0.36%) the prior year, largely driven by impaired CRE-related loans [S17]. The allowance for credit losses was increased moderately to approximately $83.6 million or about 1.15% of gross loans, demonstrating management’s prudence addressing asset quality challenges.

The loan book exhibits diversification across property types including warehouse (16.6%), retail (15.7%), multi-family (11.5%), office (9.9%), among others—though concentrated regionally within Houston-Beaumont markets subject to localized economic factors [S20][S22].

Capital Structure and Returns: Sustained Adequacy Amid Profitability Challenges

Stellar Bancorp maintained strong capital levels through the end of fiscal year 2025 with total risk-based capital ratio at approximately 15.73%, common equity tier-one ratio near 14%, and tier-one leverage ratio exceeding 11%, all well above regulatory minimums designating the bank as "well capitalized" [S8].

Return on equity held near an estimated 6.2%, subdued relative to historical peaks but consistent with current profit pressures stemming from elevated credit costs [F1][S1]. Despite this environment, management sustained dividend payments totaling nearly $29 million (~$0.57 per share) reflecting commitment to shareholder returns stability [F1][S3].

Significantly, share repurchases surged to around $73 million in fiscal year 2025 versus roughly $2.8 million the prior year—indicative of an active capital deployment approach potentially aimed at offsetting dilution or signaling confidence ahead of the announced merger with Prosperity Bancshares [F1][S3].

The funding base remained largely deposit-driven with a shift toward higher-cost interest-bearing deposits offset by improved overall liability costs year over year; borrowed funds usage was minimal underscoring reliance on core deposits as primary funding source [S12][S18].

Operational Risk Management Enhancements: Focused Governance and Cybersecurity Leadership

Operational governance incorporates integrated risk oversight with dedicated board committees focused on credit risk management and cybersecurity—a critical priority given evolving threat landscapes requiring proactive mitigation strategies [S1].

Senior leadership includes experienced specialists such as the Chief Risk Officer with extensive banking risk management background across multiple institutions providing strategic oversight aligned with industry best practices.

Cybersecurity is led by a Certified Information Systems Security Professional (CISSP)-certified Chief Information Security Officer who chairs cross-functional committees meeting monthly to monitor technology programs—reflecting advanced capabilities uncommon among regional banks but necessary amid modern cyber threats [S1].

Comprehensive audit functions complement these efforts ensuring compliance adherence while operational risks are regularly reviewed through specialized committees incorporating executive leadership participation.

Pending Acquisition: Strategic Uncertainties Amid Regulatory Review and Market Reaction

Stellar Bancorp is undergoing a significant strategic transition following announcement of its pending acquisition by Prosperity Bancshares, subject to customary shareholder approvals and regulatory clearances—introducing potential timing delays and integration complexities [N6][N9].

Market responses have been mixed; while some analysts have upgraded Stellar’s valuation anticipating consolidation benefits post-merger, stock price volatility persists reflecting uncertainty around deal closure timelines and integration execution risks [N1][N9].

Regulatory scrutiny will likely emphasize maintenance of adequate capital post-closing alongside examination of competitive impacts within overlapping Texas markets served by both entities.

Execution risks include system integrations, cultural alignment challenges, retention of key personnel, and harmonization of loan portfolios amid rising credit stresses.

Growth Outlook: Entrenched Regional Presence Amid Competitive Pressures

Despite headwinds from asset quality concerns and merger-related uncertainties, Stellar’s entrenched customer relationships within Houston-Beaumont provide a meaningful local market moat anchored in community expertise.

The diversified yet regionally concentrated loan portfolio tempers exposure fluctuations although competitive dynamics against larger national banks limit rapid organic scaling absent inorganic growth or geographic expansion.

Organic growth will depend on deepening client engagement while managing prudent credit selection given cyclicality notably impacting commercial real estate—the largest segment of the loan book.

Key Milestones for Investors: Approval Process and Credit Loss Monitoring Post-Merger

Investors should closely monitor progress on acquisition approvals encompassing shareholder vote outcomes and federal regulatory reviews which will dictate merger timing and operational focus shifts.

Post-merger periods require attention to changes in credit performance metrics since legacy Stellar portfolios display signs of softening quality; movements in nonperforming loans could materially influence provisioning needs affecting earnings volatility.

Additionally, capital allocation policies may evolve following consolidation completion potentially impacting dividend distributions or share repurchase programs based on combined entity priorities.

Conclusion: Managing Profitability Pressures Within Strategic Transition Context

Stellar Bancorp’s recent financial profile illustrates typical mid-sized regional bank challenges operating within cyclical property-focused lending environments amidst macroeconomic tightening compressing yields and elevating delinquencies [F1][S1]. While profitability has softened over the past two years due principally to elevated credit costs offsetting net interest margin pressures,[F1] disciplined capital management sustaining strong adequacy ratios alongside steady shareholder returns reflects financial resilience.[F1][S3]

Enhanced operational risk frameworks demonstrate preparedness for evolving cybersecurity threats crucial for stakeholder confidence.[S1] However, uncertainty stemming from the imminent Prosperity Bancshares acquisition adds complexity to near-term outlooks though longer-term scale benefits may materialize post-integration.[N6]

Overall, Stellar presents solid foundational strengths buttressed by localized market moats balanced against notable risks centered on asset quality trends plus event-driven transition challenges inherent in pending M&A contexts. Investors are advised to track forthcoming merger approval developments alongside quarterly updates on credit loss provisions as key indicators shaping trajectory post-closing.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments