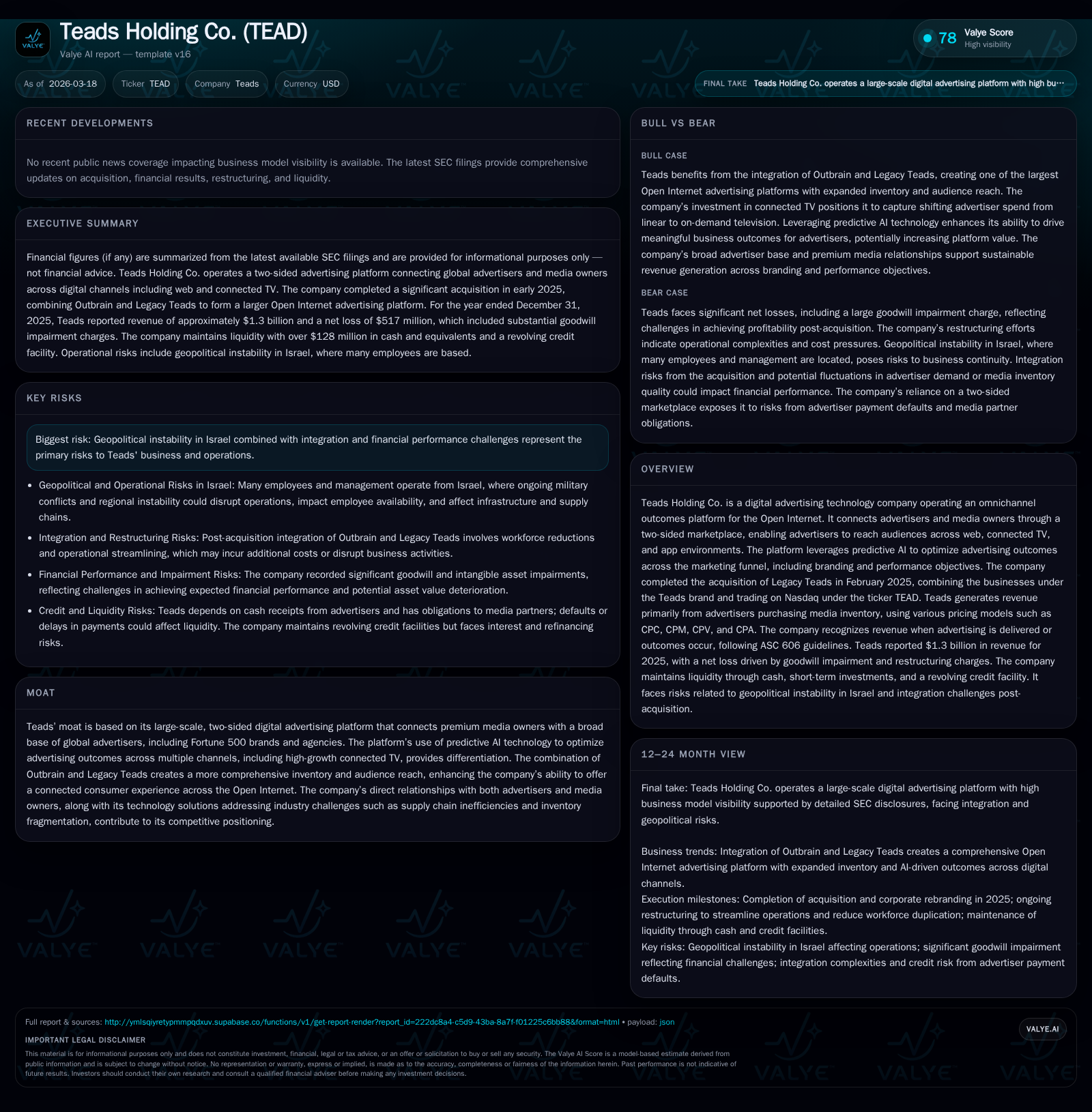

Teads Holding Co. Transforms Digital Ad Tech with Omnichannel Platform and AI Integration

The 2025 acquisition of Legacy Teads propelled Teads to $1.3 billion revenue, unveiling strategic growth avenues and operational pressures.

Teads Holding Co.’s transformative purchase of Legacy Teads in early 2025 nearly doubled its scale, driving a 46% revenue surge to $1.3 billion while escalating operating losses over 30-fold due to integration and scaling costs. The company now operates an omnichannel advertising platform leveraging predictive AI across web, connected TV, and app environments, positioning it to capture full-funnel marketing demand amid a fragmented media landscape. However, challenges remain in margin management, balance sheet leverage, and geopolitical risks localized in Israel. Going forward, Teads’ ability to stabilize profitability while expanding programmatic media inventory and innovating pricing models will be critical in delivering advertiser ROI and sustaining growth momentum.

Legacy Integration and Its Impact on 2025 Financial Performance

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1300 | -517 | 8 | -399 | +46.1% | -72624.3% |

| 2024 | 890 | -1 | 69 | -13 | -4.9% | -106.9% |

| 2023 | 936 | 10 | 14 | -9 | -5.7% | +141.7% |

| 2022 | 992 | -25 | 4 | -14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1 | 2 | -541.8 |

| 2024 | 7 | 61 | -0.3 |

| 2023 | 19 | 4 | 4.6 |

| 2022 | 33 | -10 | -11.3 |

Source: SEC companyfacts cache [F1].

Teads Holding Co.'s landmark acquisition of Legacy Teads on February 3, 2025 marked a pivotal shift in its financial footprint. Prior to the transaction, operations reflected those of predecessor Outbrain Inc., but post-acquisition the consolidated statements include Legacy Teads’ results from early February through the end of the year [S1][S2].

This $900 million deal was principally funded through $625 million cash complemented by the issuance of approximately 44 million common shares. The acquisition expanded Teads' digital advertising footprint notably, nearly doubling annual revenue from $889.9 million in 2024 to $1.3 billion in 2025—a robust year-over-year increase of about 46% [F1][S1].

Yet this surge came at significant cost. Operating income deteriorated from a loss of $12.6 million in FY2024 before the acquisition to a substantial negative $399 million post-merger—an order-of-magnitude jump attributable largely to integration expenses, expanded personnel costs tied to scaling, as well as amplified traffic acquisition costs incurred for inventory procurement across a broader range of media partners [F1][S1]. Net loss expanded correspondingly from a negligible $711 thousand deficit pre-acquisition to over half a billion dollars negative for FY2025 [F1].

The abrupt change reflects typical post-merger growing pains: investments to unify platforms, harmonize processes, accelerate product roadmaps including AI capabilities, and expand global sales efforts. Stakeholders should anticipate ongoing elevated costs in the near term as synergies are realized.

Dissecting Revenue Growth Drivers: From Omnichannel Reach to Predictive AI

Teads differentiates itself through its two-sided marketplace that directly interfaces with both advertisers—including Fortune 500 brands and agency groups—and premium media owners spanning traditional publishers to emerging connected TV (CTV) platforms and mobile app developers [S1][S2].

The company’s omnichannel platform orchestrates personalized programmatic bidding across CPM (cost-per-thousand impressions), CPC (cost-per-click), CPV (cost-per-view), and CPA (cost-per-action) pricing frameworks depending on campaign objectives ranging from branding uplift through performance conversions.

A key technological lever is predictive AI integrated deeply into campaign optimization algorithms. This capability facilitates granular audience targeting, real-time outcomes measurement throughout the marketing funnel—from impression delivery through engagement metrics—and dynamic budget allocation that enhances ROAS (return on advertising spend) for advertisers.

Further buoying growth is Teads’ extensive premium inventory access especially within CTV —a rapidly expanding segment given consumer drift toward streaming environments—and exclusive partnerships enabling unique reach across fragmented digital properties on the Open Internet [S2].

Profitability Pressures and Operating Loss Trends Post-Merger

Despite top-line momentum, profitability reflects heightened expenses intrinsic to scale transformations and legacy business integration. Operating losses magnified dramatically; the operating income margin sank deeply negative due primarily to merger-related charges which included restructuring costs totaling $28.9 million along with amortization increases—depreciation surged concurrently linked to capitalization of acquired intangibles [F1][S1].

Traffic Acquisition Costs (TAC), representing payouts to media partners for ad inventory consumed via Teads’ platform, also grew sharply—they constituted a significant portion of revenue and rose proportionally faster during parts of the year due to shifts in revenue mix and contract terms affecting margin realization.

Personnel expenses doubled relative to prior periods reflecting hiring to bolster AI development teams alongside augmented sales capacity essential for expanded platform deployment across geographies.

Net losses expanded disproportionately relative to incremental revenues which signals challenging cost structure leverage currently limiting free cash flow generation despite positive operational cash flow (~$7.6 million annually after capex) [F1].

Outlook for Growth: Market Opportunities Versus Industry Headwinds

Looking ahead, Teads targets several strategic growth vectors grounded firmly in its augmented omnichannel capabilities:

- Expansion into connected TV continues apace as advertiser demand grows for measured brand impact within premium streaming contexts.

- Further AI innovation promises deeper attribution insights linking creative execution directly with commercial outcomes at scale.

- Broader adoption of outcome-based pricing models may unlock new revenue streams by shifting advertiser commitment towards measurable business results.

However, growth pacing may encounter headwinds including ongoing geopolitical instability around key operational hubs—particularly Israel—which could disrupt talent availability or infrastructure reliability [S1]. Additionally integration complexities lingering post-merger may absorb management focus.

Seasonality inherent in advertising budgets—with Q4 typically peaking—and macroeconomic uncertainty could also impose unpredictable spending rhythms impacting sequential quarterly results [S1]. Advertiser ROAS expectations remain exacting amidst inflationary pressures requiring continual value delivery enhancements.

Capital Structure Evolution and Liquidity Position After Acquisition

Following completion of the Legacy Teads purchase, Teads restructured its capital base by raising approximately $637.5 million through senior secured notes bearing a hefty coupon rate of 10%, maturing in 2030 [S11][S13]. These notes refinanced short-term bridge loans initially used to fund acquisition outlays.

As of December 31, 2025, total liquidity stood at approximately $178.7 million comprising $128.2 million cash and cash equivalents plus $10.5 million short-term investments along with availability under a revolving credit facility capped at $40 million due to covenant restrictions related to senior secured net leverage ratios exceeding thresholds post-acquisition [F1]. The Company had no borrowings outstanding under this revolving facility at year-end but remains subject to customary covenants restricting additional indebtedness or capital returns [S6][S12].

Reviewing Capital Allocation: Cash Flow, Buybacks, and Dividend Policies

Capital deployment since acquisition has prioritized operational reinvestment over direct shareholder returns as evidenced by sharply curtailed share repurchases—the company spent only approximately $646 thousand on buybacks during fiscal year 2025 down from $6.6 million previous year—and absence of dividend distributions reflecting conservative liquidity management priorities amid loss-generation environment [F1][S14].

Free cash flow remains thin at about $2 million after capital expenditure outlays focused on platform development initiatives predominantly related to AI technology enhancement and infrastructure scaling [F1]. Return metrics have accordingly suffered; most notable is the plunge in return on equity down near -542% following heavy net losses indicating current shareholder equity erosion despite strong revenue expansion.

Strategic Risks: Geopolitical and Integration Challenges Ahead

The company explicitly acknowledges geopolitical instability concentrated in Israel—home to critical R&D operations—as a substantial risk factor potentially threatening workforce continuity or supply chain durability impacting media inventory aggregation quality [S1].

Simultaneously the complexity inherent in merging distinct technology stacks, corporate cultures,and vendor relationships places pressure on both financial performance normalization cadence and operational resilience.

Industry-wide fragmentation within digital advertising supply chains combined with increasing demand for transparency puts strain on maintaining premium inventory quality while competing against emerging generative AI-based content dynamics challenging publisher page views.

Such factors require vigilant risk mitigation measures while pursuing disciplined execution of product innovation roadmap underpinning competitive differentiation within full-funnel omnichannel ad solutions space.

Key Metrics To Monitor Moving Forward

Investors should closely watch quarterly revenue progression against traffic acquisition cost trends—better alignment would suggest improving margin control post-integration. Tracking operating loss trajectory quarter-on-quarter for signs of stabilization or reduction is essential as efficiency gains from merged entity synergies take effect. Cash runway measured via free cash flow generation versus debt servicing obligations represents another vital indicator given high leverage levels. Finally, client penetration within connected TV environments where rapid audience shifts are unfolding will gauge success capturing emerging high-growth segments benefiting from programmatic media buying innovation.

Collectively these benchmarks will signal whether Teads can translate sizable scale gains enabled by its omnichannel platform powered by predictive AI into sustainable profitable growth aligned with shifting advertiser demands within the Open Internet ecosystem.

This analysis is based solely on publicly available information as detailed above without offering any investment advice or forecasts beyond explicit disclosures. Readers should consider all risk factors outlined by the company filings when interpreting this report.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments