COMPASS Pathways Accelerates Psilocybin Therapeutics Amid Financial and Regulatory Challenges

Clinical-stage biopharma COMPASS Pathways focuses on treatment-resistant depression with ongoing trials but faces escalating losses and financing constraints.

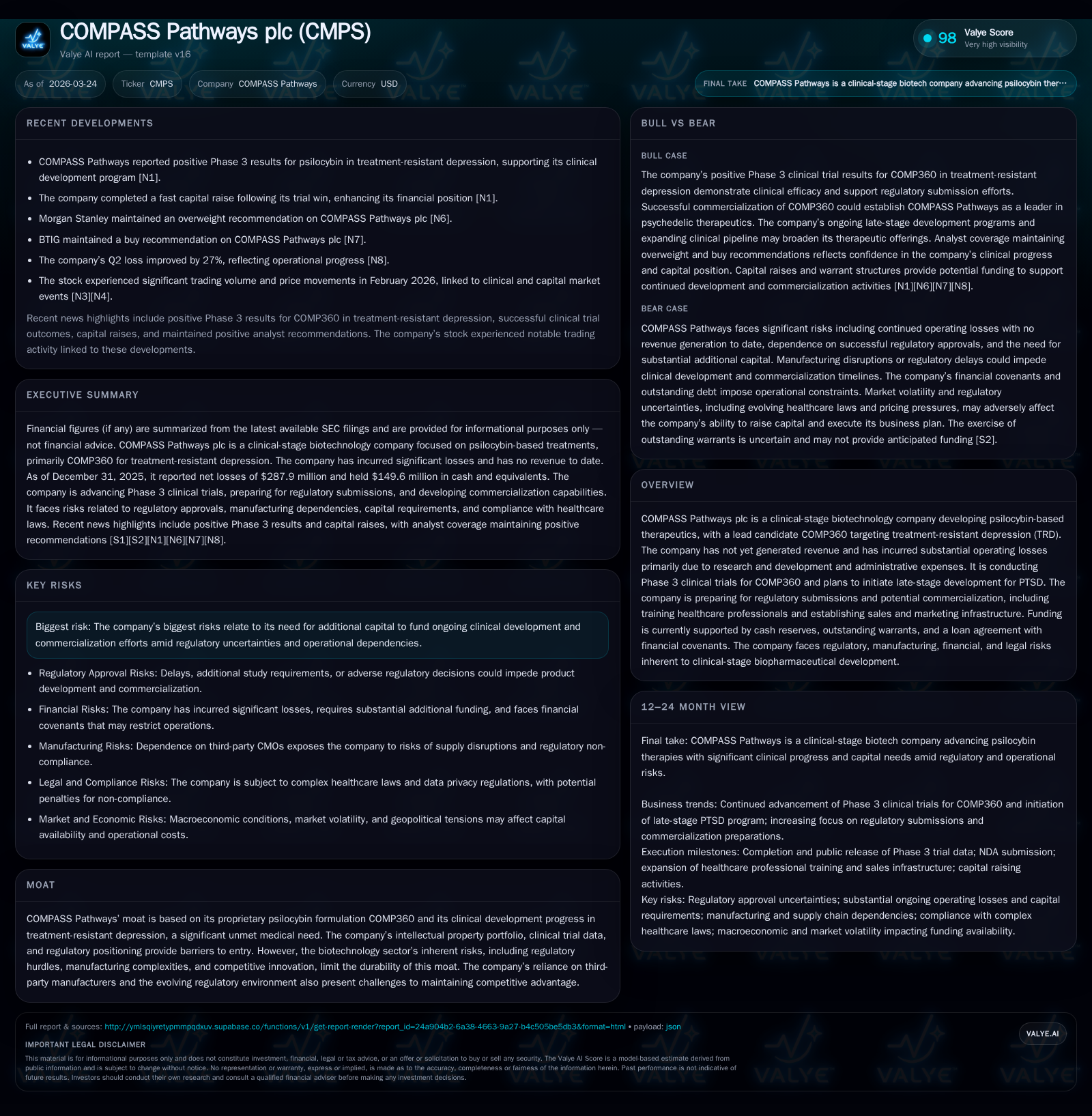

COMPASS Pathways plc is advancing its proprietary psilocybin-based treatment, COMP360, targeting significant unmet needs in treatment-resistant depression (TRD) and expanding into PTSD. Despite positive Phase 3 trial results and regulatory progress, the company remains pre-revenue with growing operating losses reaching $287.9 million in 2025. Financial resources are currently sufficient but constrained, relying on cash reserves, warrants exercises, and a $50 million loan facility subject to restrictive covenants. Regulatory, manufacturing, patent, and legal risks persist as the company prepares for potential commercialization and market launch over the next several years.

Overview of COMPASS Pathways plc

COMPASS Pathways plc operates within the clinical-stage biotechnology sector focused on developing psilocybin-based therapeutics for serious mental health disorders with an emphasis on treatment-resistant depression (TRD). Its lead investigational drug candidate, COMP360, is a pharmaceutical-grade crystalline psilocybin formulation optimized for purity and stability. The compound received Breakthrough Therapy designation from the FDA in 2018 owing to its distinct mechanism focused on rapid and durable responses where existing antidepressants are inadequate [S1].

The company’s clinical advancement journey is marked by key milestones: successful Phase 2b randomized controlled trials demonstrated efficacy at a 25mg dose versus a subtherapeutic control, with these findings published in a respected peer-reviewed journal. Building on this foundation, COMPASS completed enrollment of two pivotal Phase 3 trials (COMP005 and COMP006) during 2025 involving single-dose and fixed repeat dose designs respectively, assessing symptom severity reduction using MADRS scores at six weeks as the primary endpoint. Initial data from COMP005 showed highly statistically significant improvement over placebo [S1]. Parallel preparations proceed for filing New Drug Applications (NDA) pending further regulatory reviews [S3].

Historical Financial Performance

Despite clinical momentum, COMPASS Pathways has yet to reach commercial revenue generation as it remains in critical development phases. Operating loss trends have expanded substantially reflecting intensifying R&D investments alongside start-up commercial infrastructure costs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -288 | -157 | -179 | -85.6% | |

| 2024 | -155 | -119 | -178 | 0 | -30.9% |

| 2023 | -118 | -97 | -137 | 66000 | -29.5% |

| 2022 | -92 | -105 | -110 | 596000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 544.7 | |

| 2024 | -119 | -100.3 |

| 2023 | -97 | -52.5 |

| 2022 | -106 | -50.5 |

Source: SEC companyfacts cache [F1].

The negative equity reported at end-2025 (-$52.8 million) contrasts with prior years' positive shareholder equity positions illustrating accumulated deficit pressures from sustained losses [F1]. Cash on hand at $149.6 million leaves the current ratio at approximately 0.77 against current liabilities of nearly $248 million indicating near-term liquidity tightness [F1]. Capital expenditures are minimal as expected for a clinical-stage biotech focused primarily on R&D.

Operating cash flow remains substantially negative reflecting outflows predominantly tied to clinical trial progressions such as patient recruitment costs and production scale-up [F1]. The steep net income decline year-over-year partly reflects fair value adjustments related to warrant liabilities alongside traditional loss accruals from ongoing activity expansion [S1].

Future Growth Prospects

The main driver for future growth hinges on successful regulatory approval of COMP360 for TRD followed by market uptake in an underserved patient population. Should NDA filings receive timely FDA approvals supported by positive trial data consistency across both pivotal trials’ arms (COMP005 & COMP006), commercial launch preparations underway—such as building sales teams and training healthcare professionals—will transition COMPASS towards revenue generation [S1][S3].

Additionally planned expansion into post-traumatic stress disorder (PTSD) through late-stage development adds another potential revenue stream albeit accompanied by increased expenses without guaranteed outcomes [S1][S2]. The company also intends future development of pipeline candidates beyond psilocybin should trials meet benchmarks but this remains long term [S2].

However several limiting factors exist including:

- Dependence on maintaining intellectual property exclusivity amid evolving patent landscapes which could be impacted by third-party claims or legislative changes like the America Invents Act impacting patent tenure or licensing costs [S9][S15].

- Manufacturing scale-up complexities inherent in producing controlled substances requiring compliance with DEA scheduling procedures that may delay supply continuity or escalate costs [S1][S12].

- Navigating intricate healthcare regulatory environments globally including anti-kickback statutes and marketing restrictions that constrain commercialization strategies especially given psilocybin’s controlled substance status [S4][S6][S20].

- Needing substantial additional capital given cash burn rates especially since current loan covenants enforce minimal liquidity thresholds restricting flexibility [S8][S11][S19].

Forecasts / Milestones / Expectations

While explicit forward guidance is limited beyond declared milestones associated with continuing Phase 3 completions and NDA submissions planned within short term horizons [N1][N3], key items to monitor include:

- Timing of FDA regulatory decisions following NDA submission including possible scheduling rescheduling by the DEA necessary before marketing [S1][S21].

- Readouts from longer term follow-ups within the ongoing pivotal programs that may influence label breadth or REMS requirements impacting commercialization scope [S1].

- Progression and initial clinical data releases from the PTSD late-stage development program that can validate pipeline diversification efforts [N1][N3].

- Effectiveness of scaling manufacturing capacities aligned with expected launch demands while maintaining product quality standards that comply with cGMP regulations.

Returns / Capital Allocation

Returns metrics remain deeply negative corresponding with the clinical nature of operations without commercial revenues thus far. Based on reported figures:

- Approximate Return on Equity (ROE) based on FY2025 net loss ($287.9M) divided by ending equity (-$52.8M) suggests negative profitability scale typical of early biotech firms undergoing heavy investment phases [F1].

- Free Cash Flow remains negative at approximately -$157.2 million dominated by operating cash outflows with minimal capital expenditure reflecting concentrate use of funds towards R&D and operational expansion rather than infrastructure capex which typically characterizes mature companies [F1].

Capital structure includes indebtedness through a Loan Agreement with Hercules totaling up to $50 million initially drawn at $30 million with remaining tranches contingent upon performance milestones impacting liquidity [S8][S19]. This debt carries high interest rates (~9.75%) plus fees and payment restrictions including required minimum cash balances subject to lender covenants restricting dividends or share buybacks while outstanding [S8][S11][S19]. There has been no indication of dividend issuance or share repurchases given capital preservation priorities amid losses.

Industry Context and Competitive Considerations (Analysis)

The emerging psychedelic therapeutics sector is characterized by rapid scientific innovation interlaced with complex legal frameworks stemming from controlled substance scheduling that few traditional pharmaceuticals encounter. Developing safe delivery methods paired with rigorous clinical evidence garners increasing investor attention but also necessitates navigating uncharted regulatory frontiers where standard risk tolerance is tested.

COMPASS Pathways' strategy to establish intellectual property protection through proprietary polymorphic crystalline psilocybin formulations complemented by extensive clinical datasets represents one attempt to build defensible competitive moats while striving to establish first-mover advantage in TRD treatment. Nonetheless competitor entrants developing alternative psychedelics or adjunct therapies could reshape market dynamics rapidly.

Manufacturing dependencies pose further operational risks since scaling controlled substance production requires approvals at both federal and state levels disrupting timelines unpredictably unlike conventional pharmaceuticals produced globally under straightforward licenses.

Finally commercialization models must reconcile clinician training requirements under REMS programs emphasizing supervised administration protocols complicating simple pill dispensing paradigms typical in antidepressant markets.

Conclusion

COMPASS Pathways embodies the promise and pitfalls befitting a pioneer within an innovative yet commercially nascent biotech segment spotlighting psychedelics as next-generation mental health therapies. With tangible Phase 3 efficacy achievements attained for its flagship compound COMP360 aimed at TRD patients refractory to existing medications complemented by plans for PTSD indication development—the company teeters on a delicate threshold between research investment exhaustion and market entry onset.

Maintaining adequate liquidity constrained by debt covenant terms while managing intensifying operational complexity will be pivotal next steps prior to any sustainable commercial returns. Regulatory navigation through drug approvals intertwined with controlled substance reclassification constitute critical go/no-go junctures bearing significant financial consequence.

Investors monitoring this space should watch regulatory submission progress timelines closely alongside evolving intellectual property landscapes amid increasing competitive proliferation within psychedelic drug research.

This analysis presents an overview based on publicly available disclosures through March 24, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments