United States Lime & Minerals’ 2025 Turnaround Reflects Strong Demand and Strategic Capex

A surge in operating income and cash flow underpins USLM’s growth, driven by construction and industrial demand amid capex expansion.

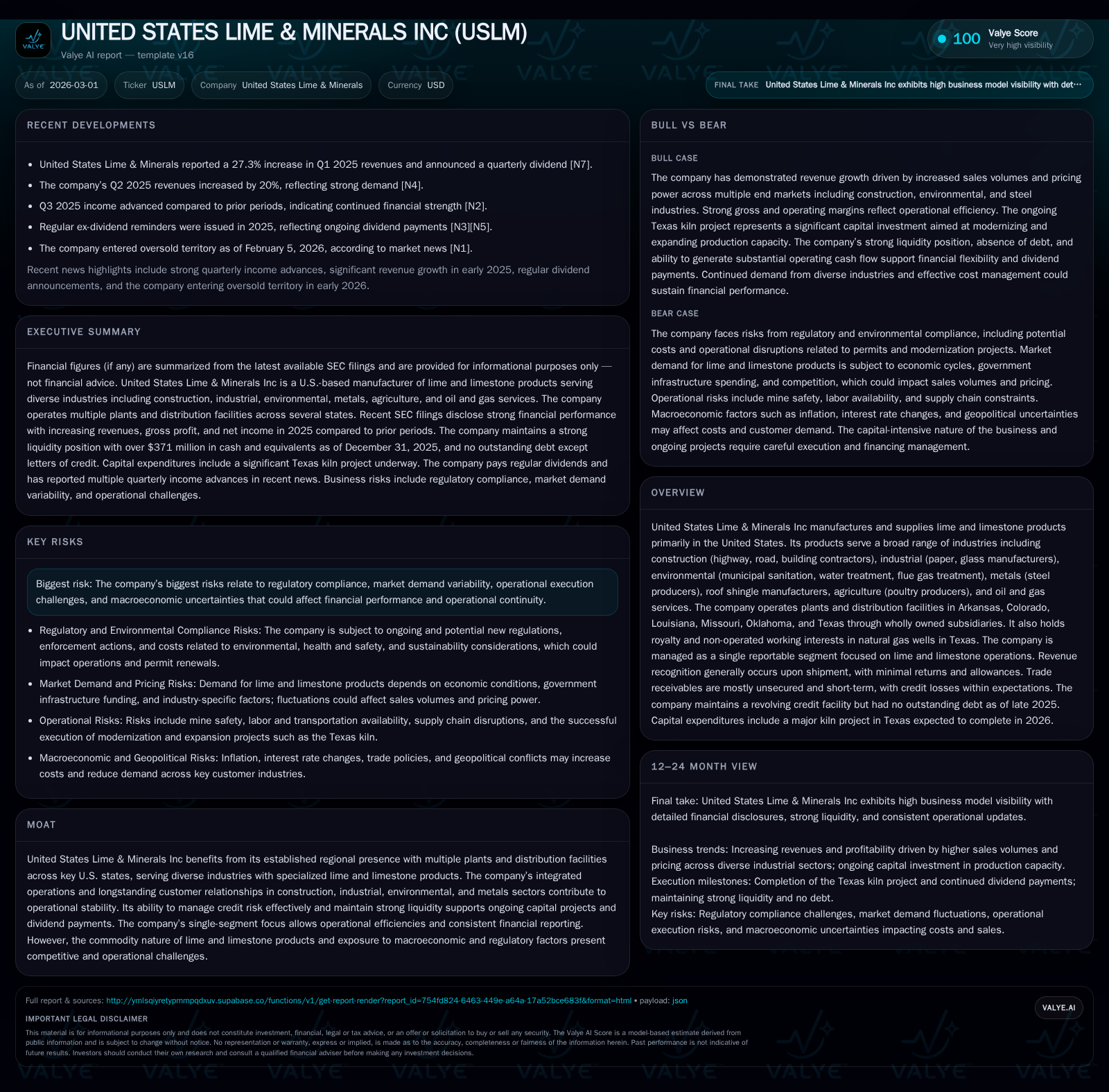

UNITED STATES LIME & MINERALS INC (USLM) exhibited robust financial progress in 2025, fueled by increased sales volumes, favorable price realization, and a focus on operational efficiency across its lime and limestone product lines. Revenue growth was supported primarily by demand from construction, environmental, and steel sectors, offset partially by softness in oil and gas services. The company invested heavily in capital projects like the Texas kiln expansion, signaling a commitment to capacity and modernization. Strong operating cash flow generation has enabled steady dividend payments and modest share repurchases while maintaining a conservative debt profile bolstered by a sizable revolving credit facility. Key risks include regulatory pressures and cyclical end-market variability.

Business Overview

UNITED STATES LIME & MINERALS INC manufactures and distributes lime and limestone products primarily across several U.S. states including Arkansas, Colorado, Louisiana, Missouri, Oklahoma, and Texas through wholly owned subsidiaries ([S1], [S10], [S25]). The company serves diversified end-markets such as construction (roadways, building contractors), industrial users (paper and glass manufacturing), environmental applications (water treatment and flue gas scrubbing), metals processing (steel industry), roof shingle manufacturing, agriculture (notably poultry), and oil and gas services ([S10], [S15]).

The company operates as a single reportable segment focused on lime and limestone operations ([S11], [S14]). Revenue is recognized upon shipment with minimal returns; external freight billed to customers is recorded as fulfillment costs within cost of revenue ([S10], [S25]). Trade receivables are predominantly unsecured but short-term with effective credit loss allowances maintained based on historical trends ([S14]).

Historical Performance & Growth Drivers

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 134 | 165 | 158 | 63 | +23.4% |

| 2024 | 109 | 126 | 125 | 27 | +46.0% |

| 2023 | 75 | 92 | 85 | 34 | +64.1% |

| 2022 | 45 | 64 | 55 | 27 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 7 | 3 | 102 |

| 2024 | 6 | 4 | 99 |

| 2023 | 5 | 1 | 58 |

| 2022 | 5 | 1 | 38 |

Source: SEC companyfacts cache [F1].

Revenue growth through mid-2025 was fueled chiefly by higher end-market demand from construction sectors—especially new infrastructure projects—and strength in environmental applications linked to regulatory requirements ([S18], [S29]). Steel industry customers also contributed increased purchases while demand softened in oil & gas service areas.

Future Growth Opportunities and Constraints

Growth prospects hinge on sustained demand in infrastructure-related segments such as highway construction and expanding industrial uses like water treatment facilities sensitive to environmental regulations ([N1], [S13], [S24]). Additionally, the boom in data center construction offers incremental uplift for limestone aggregates used in foundational works ([S29]).

However, the commodity-like nature of lime products subjects pricing to input cost fluctuations—particularly energy—and competitive market dynamics ([S24], [S22]). Regulatory compliance costs remain significant due to permits tied to plant expansions or new equipment installations like kilns ([S13]). Supply chain risks include transportation availability given reliance on railcars and trucking fleets ([S22]).

A key capital project underway is the construction of a vertical kiln at the Texas Lime Company plant initiated in 2024 with expected total spending near $65 million targeted for completion within 2026; this investment aims to enhance production capacity and efficiency ([S27]).

Financial Position and Capital Allocation

- Cash & equivalents were $371 million as of December 31, 2025 with no outstanding borrowings against the $75 million revolving credit facility except letters of credit related mainly to the Texas kiln project (~$4-7 million) ([F1], [S20]).

- Shareholders’ equity increased steadily to approximately $631 million at fiscal year-end 2025 reflecting retained earnings growth ([F1]).

- Operating cash flow rose nearly 31% year-over-year to $165 million while capex more than doubled to $62.7 million primarily due to kiln expansion spend—demonstrating prudent reinvestment into productive assets ([F1], [S27]). Free cash flow was approximately $102 million.

- Dividend payments increased moderately to $6.9 million during the year; share repurchases were modest at $2.7 million reflecting disciplined capital deployment consistent with leverage covenant constraints that limit repurchases when pro forma Cash Flow Leverage Ratio approaches thresholds ([F1], [S12], [S28]).

The company maintains leverage discipline targeting a maximum Cash Flow Leverage Ratio of approximately 3.50x EBITDA; dividends continue contingent on covenant compliance ensuring financial flexibility ([S5], [S12]).

Industry Context & Risks

Lime & limestone suppliers operate with tight margins heavily influenced by energy costs impacting calcination processes; logistical challenges persist amid national trucking labor shortages; regulatory pressures create permitting complexities; cyclical industrial activity results in demand volatility.

USLM’s geographic diversification across multiple states helps mitigate localized economic or regulatory variances but also exposes it to regional risks.

Principal risks include:

- Regulatory compliance delays or failures potentially restricting expansions or causing operational disruptions.

- Demand variability especially from volatile oil & gas services sectors.

- Competitive pricing pressures amid rising input costs.

- Macroeconomic uncertainties such as inflationary shocks or reductions in government infrastructure spending.

- Supply chain disruptions affecting fuel or transportation capacity crucial for timely deliveries.

Outlook & Monitoring Points

Key metrics for investors include shipment volumes across core end markets—construction versus energy—and updates on Texas kiln project progress given its strategic significance. Liquidity trends relative to capex spending will indicate free cash flow sustainability for dividends without requiring debt draws. Regulatory developments at federal or state levels may impact permitting timelines or emissions standards affecting operations. Pricing adjustments amid inflationary input costs will materially influence gross margin performance.

Conclusion

United States Lime & Minerals Inc demonstrated significant financial momentum through fiscal year 2025 driven by broad-based volume growth combined with price improvements across its U.S.-focused customer base ([F1]). Measured capital investment primarily targeting capacity expansion via modernized equipment such as the Texas kiln reflects management’s commitment to long-term operational scale advantages ([S27]). Conservative leverage management alongside strong operating cash flows supports continued dividend payments while cautiously pursuing share repurchases within covenant limits ([F1], [S28]). Despite promising fundamentals, market cyclicality coupled with regulatory complexities requires ongoing management agility ([S24], [S22]). Vigilant monitoring of end-market trends and disciplined capital execution remain critical themes going forward.

This analysis is based solely on publicly available information without any forward-looking investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments