Artius II Acquisition Inc.’s Capital Intensity and Deadline Threaten SPAC Viability

Operating as a blank check company, Artius II Acquisition Inc. depends on timely deal completion amid mounting costs and liquidity pressure.

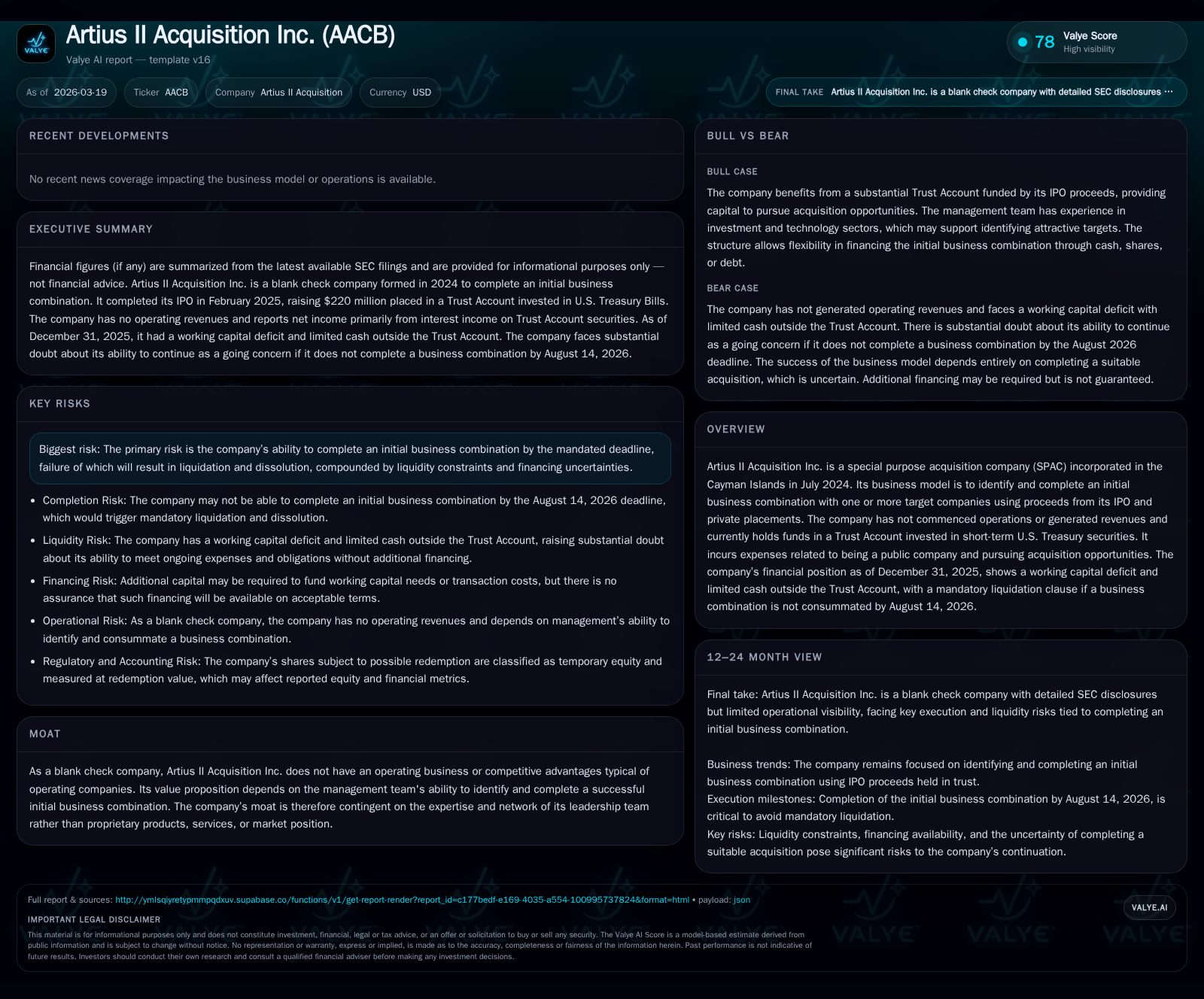

Artius II Acquisition Inc. (AACB) began in mid-2024 as a Cayman Islands-incorporated SPAC, raising over $221 million through an IPO and private placements to pursue acquisition targets. The company has no operating revenues and recognizes interest income from treasury securities held in trust. Despite generating net income by virtue of interest income exceeding expenses, AACB faces a working capital deficit and limited liquid resources outside the trust, accompanied by ongoing public company costs and a looming August 2026 deadline for completing its initial business combination or facing liquidation. The substantial advisory fees and deferred underwriting compensation further pressure cash flow, while reliance on sponsor loans remains uncertain, underscoring the critical importance of closing a transaction on time.

Company Overview

Artius II Acquisition Inc., incorporated in the Cayman Islands on July 25, 2024, operates as a special purpose acquisition company (SPAC). Its core purpose is to identify and complete an initial business combination through mergers or acquisitions using proceeds from its February 14, 2025 initial public offering (IPO) and related private placements [S1]. As a blank check entity, AACB does not conduct any substantive operations or generate independent revenues; rather, it generates nominal non-operating income primarily from investments held within its Trust Account [S1].

The company’s Trust Account held approximately $228.1 million at December 31, 2025 consisting mainly of short-term U.S. Treasury bills with maturities under six months. Interest income earned on these securities totaled roughly $8.08 million for calendar year 2025 [S1][S4]. However, the company’s actual operating cash balance outside the Trust Account was a mere $32,193 as of that date [F1].

Historical Financial Performance

Since inception through year-end 2025, AACB has recorded no operational revenues but has recognized interest income on Trust Account assets which substantially offsets operating expenses related to being public: legal fees, administrative costs, consulting, due diligence expenses paid as it pursues acquisition opportunities [S1][F1].

Notably for the full year ending December 31, 2025:

- General and administrative expenses were approximately $1.94 million.

- Advisory fees contracted for by the underwriter accounted for an additional $6 million expense.

- These costs were partially offset by interest income totaling about $8.08 million.

- The net result was a small positive net income of $136,237 [S1][F1].

For comparison:

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

*Period from July inception through December year-end.

These figures illustrate that while the company reports modest net income driven by interest earnings surpassing ongoing expenses, it remains unprofitable operationally without any acquired business generating revenue.

Capital Structure and Liquidity Position

AACB's capital raise included 22 million units sold at $10 each during its IPO (gross proceeds approx. $220 million), alongside a simultaneous sale of 175,000 Private Placement Units generating an additional $1.75 million [S1][S24]. Proceeds placed into the Trust Account are earmarked exclusively for use in financing the initial business combination.

Transaction costs amounted to roughly $7.54 million including cash underwriting fees ($250k), deferred underwriting commissions ($6.6M), and other offering expenses [S24]. The deferred underwriting discount becomes payable only upon consummation of the business combination transaction.

Outside the Trust Account, liquidity remains tight:

- Operating cash was about $32k end-2025.

- Current liabilities exceeded current assets resulting in a working capital deficit near $1.2 million [F1][S9][S16].

- Monthly administrative fees of around $25k are ongoing until transaction closure or liquidation [S25].

- Sponsor may provide bridge funding loans at their discretion but is not obligated [S9][S16]. No borrowings were outstanding under these arrangements at year-end [S23].

This tight liquidity situation underscores AACB’s dependence on completing a deal soon or securing additional capital injections to maintain operations.

Risks and Challenges

The major risk is failure to execute an initial business combination by August 14, 2026 mandated liquidation deadline which would cause dissolution and return limited funds to shareholders after expenses [S9][S15][S20]. Liquidity constraints external to the Trust Account heighten vulnerability especially if additional financing cannot be sourced on acceptable terms [S9][S15]. The ongoing obligation to cover advisory fees, deferred underwriter fees upon deal closing, monthly service contracts, and due diligence costs without offsetting revenues increases financial pressure.

Furthermore, market volatility linked to global geopolitical tensions could reverberate through capital markets affecting valuation multiples and deal feasibility for prospective acquisition targets [S23], complicating deal sourcing efforts.

Outlook: Drivers and Milestones to Monitor

AACB’s future trajectory hinges almost exclusively on its ability to finalize an initial business combination within roughly five months from report filing date (March 19 to August 14, 2026) [S9]. Success would trigger conversion of Class B founder shares into Class A stock partially diluting public shareholders but legitimizing ongoing operations post-merger [S18][S26]. Failure results in mandatory wind-down with distributions likely confined close to IPO trust account breakup values less costs.

Investors should watch for announcements regarding:

- Identification of potential target(s).

- Signing of definitive agreements regarding combination(s).

- Financing arrangements beyond trust account funds.

- Sponsor or director loans extended for working capital support.

Absent explicit forward guidance from management or disclosed milestones beyond statutory requirements [N# none available], these developments represent key binary inflection points.

Capital Allocation History and Policy

Being a pre-revenue SPAC model firm:

- No dividends have been declared or initiated; not applicable at this stage.

- No share repurchase activity reported since inception given unique capital lock-up structure around Trust Account funds.

- Deferred underwriting fees ($6.6 million) payable only upon transaction completion serve as contingent capital outflows [S24][S26].

- Advisory fees totaling $6 million were expensed upfront per agreement terms regardless of transaction outcome [S24][F1].

- Working Capital Loans up to $1.5 million may convert into private placement shares at lender discretion post-combination but remained unused as of last report [S16][S23].

All efforts focus narrowly on arranging adequate financial resources to support transaction-related activities rather than broader capital return strategies typical in mature enterprises.

This analysis synthesizes data extracted from Artius II Acquisition Inc.’s SEC filings as of March 19, 2026 ([F1], [S#]) combined with Valye News’s industry insight into SPAC liquidity dynamics and structural risk factors inherent to blank check companies constrained by forced deadlines. While AACB presents foundational capitalization sufficient for acquiring targets, rapidly approaching deadlines coupled with recurring cost burdens underline material existential uncertainty absent prompt deal closures or additional financing measures.

Disclaimer: This memo is strictly informational for internal analytical purposes only and does not constitute investment advice or recommendations regarding Artius II Acquisition Inc.’s securities or any associated transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments