Abacus Global’s Expansion in Life Settlements and Asset Management in 2025

Abacus Global Management, Inc. more than doubled its revenue in 2025 through accelerated life settlement acquisitions and asset management growth despite liquidity strains.

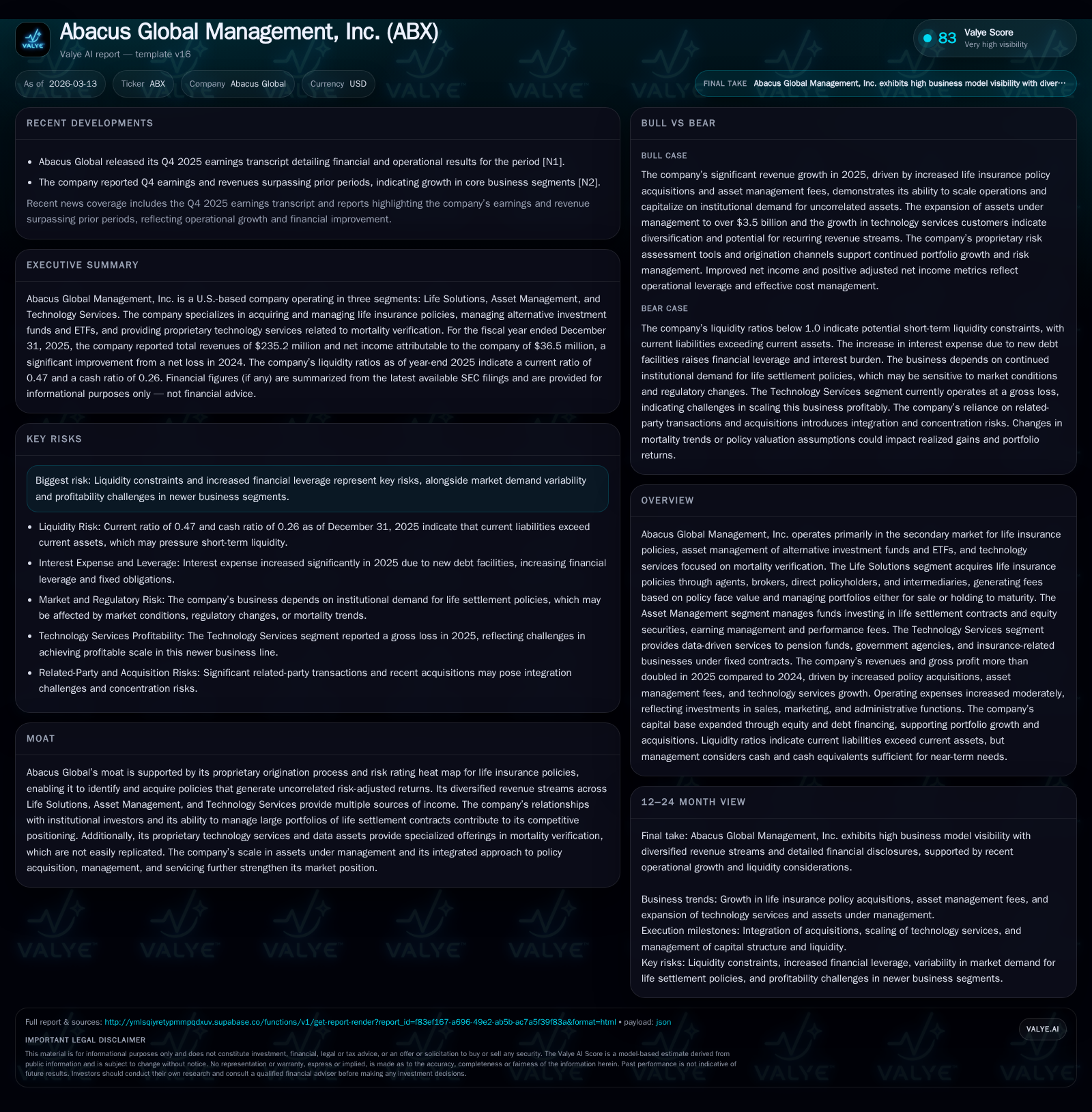

Abacus Global Management delivered a striking turnaround in 2025, with revenues surging over 110% year-over-year to $235.2 million and operating income flipping from a slight loss to nearly $88.8 million [F1]. This growth was primarily driven by the Life Solutions segment’s expansion in policy acquisitions and portfolio servicing fees as well as a significant jump in Asset Management revenues from fee-based funds [S7][F1]. The Company also invested heavily to grow its Technology Services segment’s nascent mortality verification offerings, albeit at a loss. Despite robust earnings, Abacus continues to grapple with liquidity constraints as reflected by a sub-1 current ratio and negative free cash flow [F1][S5][S6]. Capital deployment included heavy stock buybacks totaling over $43.8 million funded primarily from cash on hand [S4][F1]. Looking ahead, the company must balance sustaining origination volume amid policy availability risks while navigating debt covenants tied to its Senior Secured Credit Facility [S6][S27].

From Losses to Gains: Historic Revenue and Profit Leap in 2025

Abacus Global Management demonstrated a remarkable financial transformation in fiscal year 2025 after years of uneven performance. The Company's total revenue surged by 110.2% year-over-year reaching approximately $235.2 million compared with $111.9 million in 2024, marking more than a doubling of top-line volume [F1]. Operating income swung dramatically from a modest loss of roughly $0.9 million in the prior year into positive territory with nearly $88.8 million earned last year — an improvement exceeding ten thousand percent on a percentage basis that underscores the reset trajectory for the business.

Net income attributable to common shareholders turned sharply positive as well, rising from a net loss of approximately $23.96 million in 2024 to net income exceeding $36.5 million in 2025 [F1]. This significant bounce-back denotes not only revenue growth but also notable margin expansion and operational leverage unlocking profitability across core segments.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 235 | 37 | -26 | 89 | +110.2% | +252.4% |

| 2024 | 112 | -24 | -209 | -1 | +68.6% | -351.8% |

| 2023 | 66 | 10 | -65 | 24 | +1578.7% | |

| 2022 | -1 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 44 | -27 |

| 2024 | 11 | -210 |

| 2023 | 1 | -65 |

| 2022 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary (FY2023–FY2025), USD millions unless noted [F1]

Unpacking the Drivers: Life Solutions and Asset Management Segment Performance

Core contributions to Abacus Global’s turn came chiefly from two segments detailed prominently in its filings: Life Solutions and Asset Management.

The Life Solutions segment specializes in acquiring life insurance policies primarily via agents, brokers, direct policyholders, and intermediaries under a proprietary origination process backed by rigorous eligibility screening including mortality verification steps [S1][S7]. Revenues within this segment arise largely from origination fees averaging approximately 2% of policy face value plus portfolio management and servicing fees for both traded policies and those held until maturity.

In financials, the Life Solutions segment generated revenues of approximately $200.7 million for the year ended December 31, 2025 with cost of revenue around $12.9 million resulting in gross profit exceeding $187 million—highlighting strong margin performance from increased acquisition volumes and fee income growth [S7].

Simultaneously, Asset Management’s contribution notably expanded with revenues climbing from about $3.6 million in the comparable period of 2024 to roughly $33.8 million in fees earned through management of alternative investment funds focused on life settlement contracts along with expanded equity ETF strategies that leverage free cash flow based thematic approaches [S7]. Gross profit stood near $20 million highlighting improving operational scale driven by fee base growth compounded by performance fee realization over hurdle benchmarks typical for asset managers operating longevity-driven products.

This blended approach improves Abacus’ ability to harvest value via both direct policy ownership economics within Life Solutions alongside recurring fee streams from institutional clients tapping long-duration assets within managed funds.

Technology Services: From Losses to Emerging Revenue Stream

Though smaller relative to the other divisions, Abacus’ Technology Services segment embodies strategic forward-looking investment aimed at leveraging proprietary health/longevity data analytics and mortality verification technology deployed principally through fixed-fee contracts with pension funds, government agencies, and insurance sector clients.

Revenue here rose sharply but remains modest—up from roughly $34 thousand in late-2024 launch activity rising over twentyfold to around $0.72 million for full year ended December 31, 2025 [S7][F1]. Yet costs also rose steeply as hiring and R&D outlays intensified leading this segment to report a gross loss near $1.4 million reflecting early build phase burdens.

The uniqueness of this service vertical rests on specialized datasets rarely accessible elsewhere plus sophisticated algorithms that can verify insured lives' mortality status faster than conventional actuarial methods—offering barriers against replication given regulatory compliance demands around protected health information combined with secure data handling protocols.

Proprietary Origination Process and Risk Models Powering Growth

Central to Abacus Global’s competitive moat is its proprietary origination framework which uses three primary channels—agents/brokers, direct contacts with policyholders, and third-party intermediaries—to source life insurance policies suitable for secondary market purchase at scale [S1]. These flows provide steady deal pipelines necessary given inherent scarcity risks noted further below.

Augmenting channel reach is a patented risk rating heat map methodology integrated into underwriting systems that allows Abacus to calibrate risk-adjusted returns effectively across policies by projecting life expectancy estimates combining mortality tables with real-time health metrics inputted from insured individuals’ records verified through its tech services platform.

This yields uncorrelated returns diverging meaningfully from mainstream financial instruments—critical since accurate premium tracking combined with longevity forecasting is notoriously challenging yet fundamental for sustainable profitability here.

Capital Structure and Liquidity: Managing Debt and Covenant Compliance

Abacus relies heavily on structured debt facilities notably its Senior Secured Credit Facility (SSCF), arranged at closing late-2024 providing initial term loans aggregating $100 million plus a delayed draw term loan option originally sized up to $50 million fully drawn by September 2025 to finance accelerated life settlement policy purchases aligned with business expansion strategies [S5][S6].

The SSCF bears interest at SOFR plus an approximate spread of ~5%, stepping down contingent on EBITDA margins achieved which signals lender incentivization via performance-related covenant structures customary for leveraged entities managing illiquid securities portfolios.

While scaled debt boosts buying power enabling market share gain when quality policies are scarce, it has compressed liquidity ratios; notably the current ratio hovered near just under half at ~0.47 reflecting working capital constraints stemming from premium payments needed on held policies alongside funding procurement cycles for new acquisitions amidst uneven cash inflows tied partly to timing differences between premium disbursements versus death benefit realizations [F1][S5]. Nonetheless, credit covenant compliance was maintained as of December 31, 2025 per disclosures.

Capital Allocation Choices: Stock Repurchases Versus Cash Needs

Abacus Global signaled confidence via active capital return measures including multiple Board approvals during April through November 2025 augmenting total authorized stock repurchase capacity first set at $15 million ending up extended incrementally reaching aggregate authorization nearing $60 million expiring May 2027 [S4][S14].

During fiscal year 2025 alone the Company consummated about $43.8 million worth of share buybacks reflecting opportunistic execution as common shares traded below intrinsic value estimated internally perhaps tempered by trading plan protocols under Rule 10b5-1 registrations ensuring compliance stability during market volatility phases.

These repurchases were financed primarily using available cash plus forecasted free cash flows; however notable is persistent negative operating cash flow of about -$25.7 million coupled with capital expenditures just short of one million dollars resulted in reported negative free cash flow approximating -$26.6 million indicating ongoing reinvestment priorities balanced against shareholder remuneration ambitions [F1][S4]. Meanwhile dividends commenced modestly with a quarterly payout declared late-2025 at twenty cents per share signaling intended continuation conditional upon future earnings sustainability.

Operational Challenges and Risk Factors Ahead

Despite commendable gains performed operationally during the year ended December 31, 2025 several pragmatic risks loom large:

- Policy valuation uncertainty inherent due to fair value measurements at Level 3 inputs without active liquid markets potentially impacting financial statements materially upon misestimation.

- Accuracy limits on longevity forecasting where medical advances or population health improvements could elongate insured lives unexpected disrupting portfolio returns.

- Market supply risks governed by finite availability meeting strict purchase parameters requiring constant origination innovation or weakening acquisition volumes.

- Competition intensifying among originators inclusive of insurers themselves re-entering secondary markets thus compressing spreads achievable.

- Data privacy laws such as HIPAA/GLBA impose stringent requirements elevating cybersecurity risks especially given reliance upon proprietary mortality database services with potential reputational damage if breaches occur.

- Negative public sentiment historically impacting sector sentiment continuity posing valuation/litigation exposure concerns that require active stewardship and communication strategies [S12].

Market Outlook: What to Watch Post-2025 Surge

Looking forward past the robust financial surge of calendar year 2025 key indicators warrant close attention:

- Sustaining origination volume will hinge on Abacus’ ability to navigate the tightening pool of eligible life insurance policies while fortifying agent/broker relationships bolstered by data-driven insights guiding purchase decisions.

- Asset Management funds must continue scaling AUM while delivering hurdle-clearing performance fee capture amid volatile credit/equity markets shaping investor appetite toward longevity-driven products.

- The Technology Services segment needs breakeven inflection via contract renewal expansions leveraging proprietary advantages related to real-time mortality analytics vital for institutional client retention.

- Liquidity positions require vigilant monitoring especially given tight current ratios necessitating judicious working capital management balanced against ongoing debt repayment schedules governed under SSCF covenants due through decade-end horizon.

- Observing strategic capital allocation around buybacks versus dividend sustainability will signal management’s financial prudence stance influenced strongly by free cash flow trajectories moving forward.[N1][N2][S28]

--

This analysis is based solely on publicly available SEC filings dated as of March 13, 2026 ([F1], [S#]) and recent reported events ([N#]). It does not constitute investment advice or recommendations but aims to provide an insightful review into Abacus Global Management’s operational performance, financial condition, business model dynamics, risks encountered, and strategic posture following its decisive growth milestones during the reported fiscal period.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments