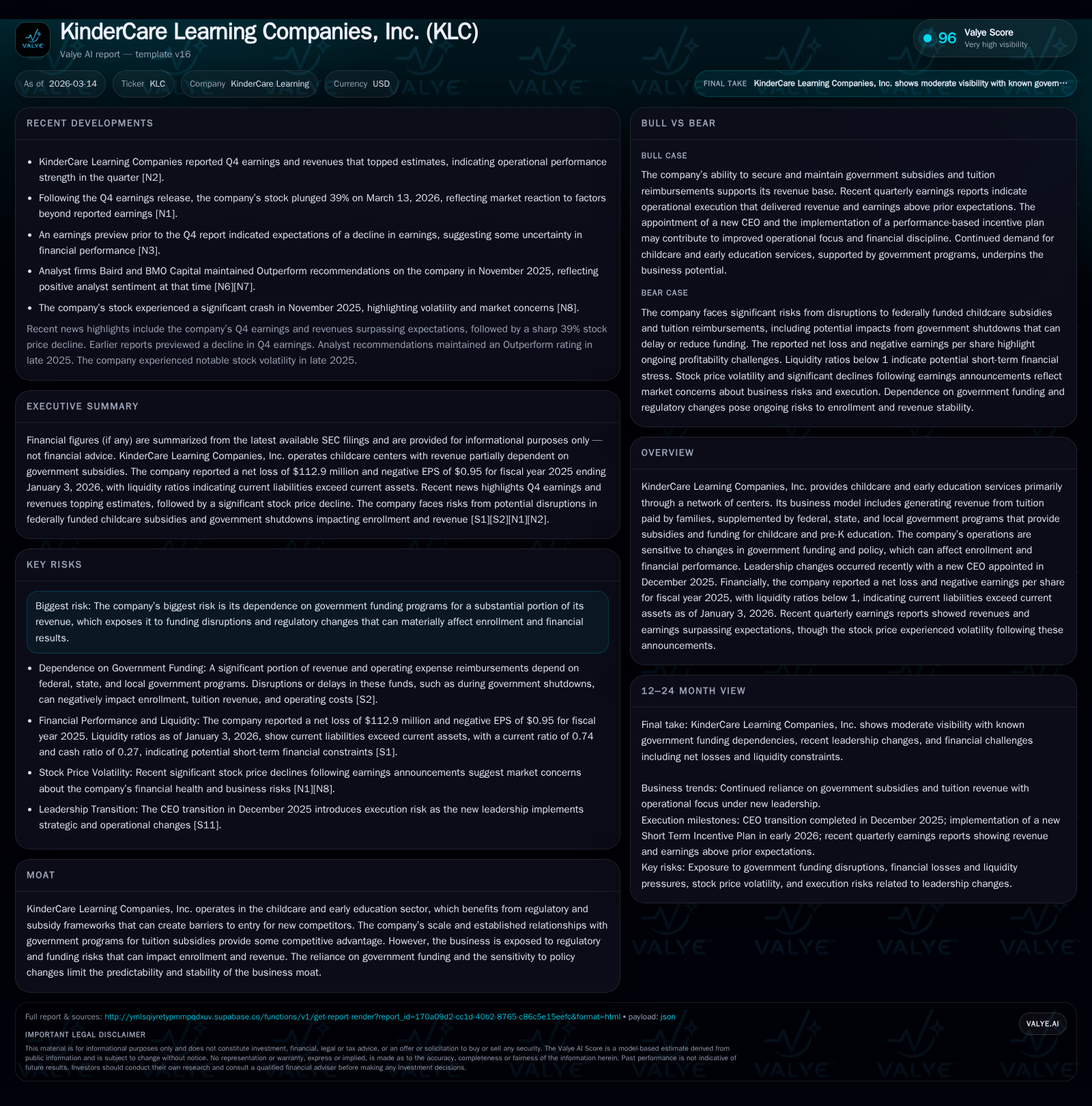

KinderCare Learning Companies: Rebounding Through Revenue Surges Amid Funding Sensitivities

KinderCare demonstrated significant operational recovery in fiscal 2025 with revenue growth and a doubling of operating cash flow despite ongoing risks tied to government subsidy reliance and tight liquidity.

Fiscal year 2025 marked a pronounced financial turnaround for KinderCare Learning Companies, Inc., highlighted by a 77.5% reduction in operating loss and a 105.8% surge in operating cash flow. While the company remains unprofitable with a net loss of $112.9 million, strong cash generation has improved strategic flexibility. KinderCare’s core growth drivers include improving enrollment and favorable tuition reimbursement trends, although the business continues to face vulnerability from potential disruptions in federal and state childcare subsidy programs. The appointment of CEO John T. Wyatt in December 2025 signals a leadership focus on navigating these funding headwinds alongside operational enhancements. Looking forward, liquidity constraints and evolving regulatory factors will be critical milestones to monitor.

Historical Performance: From Deep Losses to Earnings Improvement

KinderCare's financial results for fiscal year (FY) 2025 reveal considerable progress from the prior year’s performance metrics. Operating income losses shrunk markedly by 77.5%, improving from -$89.3 million in FY2024 to -$20.0 million in FY2025 [F1]. This sharp mitigation of operating loss suggests meaningful enhancements in underlying center operations, cost control measures, or enrollment optimization initiatives.

Nevertheless, net income remained negative at -$112.9 million, narrowing only by 15.5% from -$133.6 million the previous year [F1]. The relatively smaller improvement here compared to operating income implies ongoing pressures, possibly including financing costs or non-operating expenses.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -113 | 239 | -20 | 128 | +15.5% |

| 2024 | -134 | 116 | -89 | 132 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 110 | -14.9 |

| 2024 | -16 | -15.5 |

Source: SEC companyfacts cache [F1].

This table summarizes the key financials underpinning KinderCare’s turn towards operational resilience [F1]. The near-flat capital expenditure figures indicate ongoing investments in existing facilities or technology support despite tighter financial conditions.

Breakdown of Growth Drivers in FY2025

The revenue acceleration during Q4 2025 notably exceeded market expectations as per the company’s earnings release [N2]. Key contributors included an uptick in enrollment headcounts—a critical driver given KinderCare’s tuition-based revenue model—and expansion or stabilization in tuition reimbursement flows delivered through federal and state programs [S1][S2].

However, this top-line behavior remains tightly coupled with policy dynamics surrounding government childcare subsidies, which fund a tangible proportion of tuition fees [S2]. Administrative or appropriations delays associated with federal government funding cycles have historically impacted pass-through funding to local centers, thereby influencing the timing and certainty of cash collections [S8][S4].

KinderCare's ability to capture growth from these channels reflects its established scale and embedded relationships within subsidy frameworks but simultaneously underscores exposure to volatility in public funding regimes.

Operational Cash Flow as a Beacon Amid Negative Earnings

A particularly encouraging highlight is the doubling of operating cash flow from $115.9 million in FY2024 to $238.5 million in FY2025, representing a hefty improvement of 105.8% [F1]. This jump has translated into approximately $110 million positive free cash flow (operating cash flow less capex), signaling enhanced liquidity management amid earnings challenges.

Such strong CFO generation affords KinderCare more runway for strategic initiatives or debt service, serving as a crucial buffer given its negative net income stance [S12][S23]. The relative constancy of capex spend reflects ongoing commitment to infrastructure but without exacerbating cash strain.

Government Subsidies: A Fundamental Risk to Enrollment and Revenues

A defining risk factor lies in KinderCare's dependency on federal, state, and local government programs that subsidize child care tuition [S2][S8]. These funds often arrive via pass-through mechanisms contingent on appropriations processes vulnerable to shutdowns or administrative delays.

Prolonged lapses or funding suspensions could sharply curtail available subsidies causing declines in enrollment as families lose financial access or face delayed reimbursements [S4][S5]. KinderCare acknowledges these vulnerabilities explicitly within its risk disclosures highlighting potential adverse impacts on tuition revenue streams and cost structures.

While the company endeavors to mitigate timing risks through contingency planning and legislative engagement efforts, the unpredictability inherent in funding environments remains an existential constraint.

Recent Leadership Transition and Its Strategic Implications

On December 2, 2025, KinderCare appointed John T. Wyatt as CEO while retaining his role as Chairman of the Board, succeeding Paul Thompson who resigned concurrently [S25][S27]. Wyatt brings extensive experience steering consumer-oriented brands through operational transformations.

This leadership pivot coincides with KinderCare’s rebound phase as it seeks to solidify revenue gains while maneuvering amidst subsidy uncertainty [N2]. Strategic priorities under Wyatt may emphasize operational productivity improvements combined with proactive subsidy risk management given external dependencies.

The transition also aligns with governance intentions stated by the Nominating and Corporate Governance Committee focusing on executive continuity during recovery efforts.

Capital Allocation Profile: Liquidity, Capital Structure, and Returns Analysis

Liquidity ratios reveal heightened stress: current assets stood at $358 million versus current liabilities of approximately $485 million at January 3, 2026, resulting in a current ratio near 0.74—the working capital deficit indicating short-term obligations exceed liquid resources [F1]. This imbalance could constrain operational flexibility.

KinderCare's equity base contracted by roughly 12.7% during FY2025 down to $755 million amid sustained losses [F1]. This erosion contributes to an approximate return on equity (ROE) of -14.9%, reflective of recurring net losses absorbing shareholder capital value.

No dividends or share repurchase programs were declared or executed during this period as per recent filings reflecting prudent capital preservation stance given financial constraints [S10][S12][S15].

The company's modest leverage positioning necessitates careful stewardship of working capital cycles and financing capacity amidst external payment timing risks [S13][S14].

Forecasting KinderCare’s Recovery: Milestones to Watch

Forward-looking signals hinge on several pivotal milestones deserving investor scrutiny though explicit guidance remains unavailable publicly [N3][N4]. These include:

- Enrollment metrics continuing upward trend post-Q4 gains indicating sustained demand resiliency.

- Timely appropriations and disbursement patterns from federal and state childcare subsidy programs mitigating prior funding disruptions.

- Execution progress under new CEO John T. Wyatt translating into positive margin trajectories or expense efficiencies.

- Any regulatory shifts impacting eligibility criteria or reimbursement rates for subsidized childcare services affecting overall revenue mix.

As such data evolve over subsequent quarters, they will serve as barometers for KinderCare’s ability to sustain its operational recovery amid sectoral complexities.

Industry-Specific Challenges in Early Education Financing

KinderCare operates within a childcare ecosystem where 'pass-through funding' delays are commonplace due to multi-layered administration from federal down through state agencies impacting monthly tuition reimbursement flows [S2][S8]. Such timing gaps pressure cash conversion cycles altering working capital requirements significantly.

Further complicating this landscape are 'cost-to-serve mix' considerations where variable facility overheads intertwine with fluctuating relative subsidy support levels across geographic segments—requiring nimble financial management from providers like KinderCare who must balance enrollment headcount variability against fixed center operation costs.

Hence industry participants regularly monitor 'tuition reimbursement cycles' closely since deviations materially influence liquidity positions and operating results outside pure demand fundamentals.

This analysis synthesizes publicly available SEC filings up through early March 2026 alongside contemporaneous earnings disclosures without speculative augmentation beyond documented data points referenced herein. All financial figures represent United States Dollar amounts unless otherwise specified. This memo omits investment recommendations adhering strictly to analytical presentation parameters described above.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments