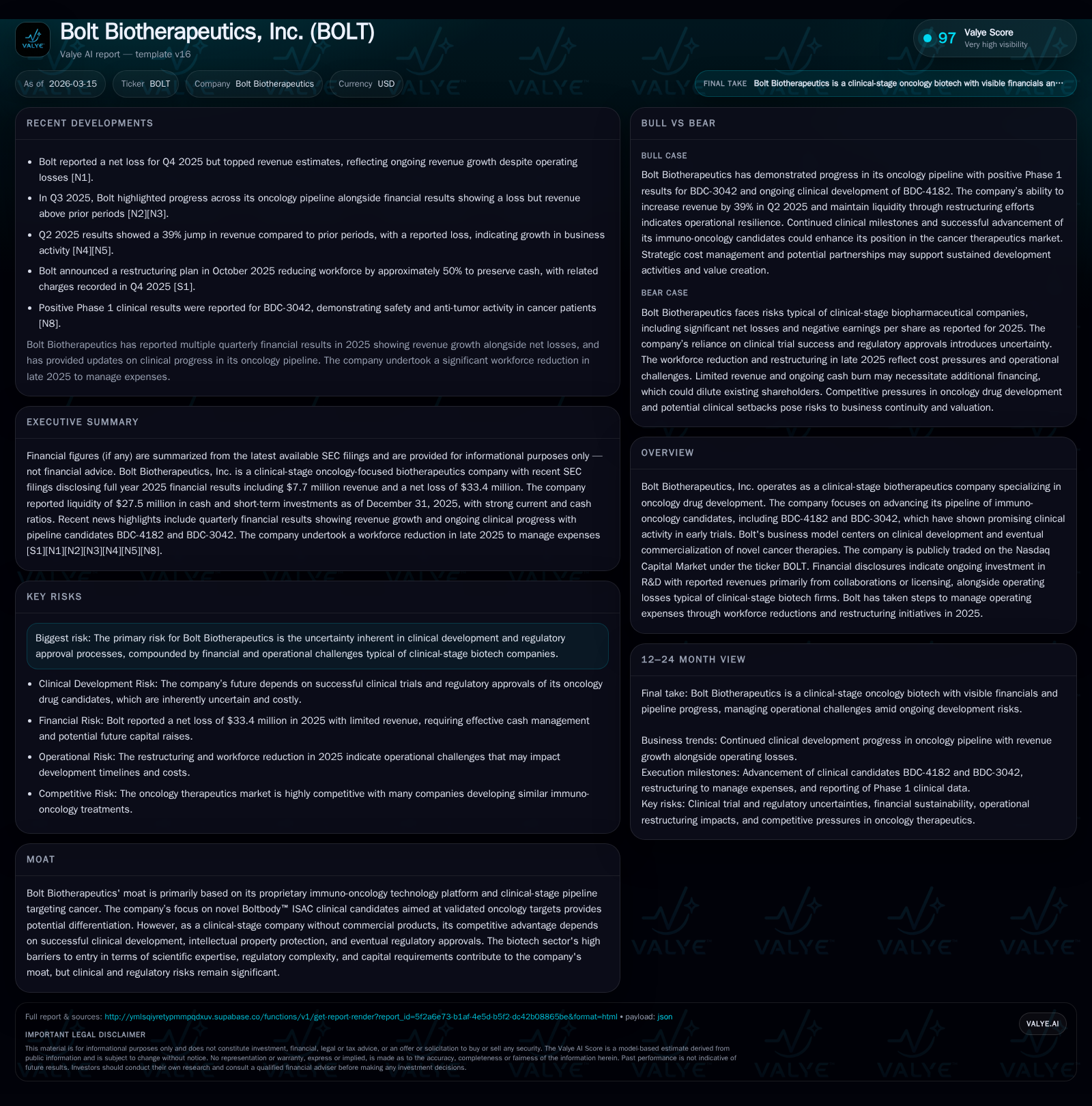

Bolt Biotherapeutics Climbs Toward Clinical Milestones Amid Operating Loss Improvement

The company advances immuno-oncology candidates while cutting operating losses through strategic restructuring in 2025.

Bolt Biotherapeutics, a clinical-stage firm specializing in innovative cancer therapies via its Boltbody™ ISAC platform, reported steady revenues with a near-flat top line alongside a substantial halving of operating losses for the year ending 2025. Key pipeline assets BDC-4182 and BDC-3042 continue advancing in early clinical trials, reinforcing future growth potential despite inherent clinical and regulatory risks. The firm’s capital allocation shows prudence with controlled cash burn and restructuring initiatives aimed at operational sustainability while clinical milestones remain crucial catalysts to watch.

Steady Revenue Growth and Reduced Operating Losses in 2025

Bolt Biotherapeutics maintained a stable revenue profile in fiscal year 2025 with reported top-line receipts of $7.695 million, practically unchanged from $7.69 million in the prior year [F1]. This revenue consistency likely reflects steady collaboration or licensing income sources typically seen in clinical-stage biotech companies that have yet to launch commercial products. More notable is the dramatic reduction of operating losses — from approximately $73 million in 2024 down to $36.1 million in 2025 — representing an improvement exceeding 50% year-over-year [F1][N1][S1]. This contraction of operating burn aligns with the company’s reported workforce reductions and restructuring efforts during the same timeframe, signaling Bolt's active management of its expense base and selling general administrative costs.

Taken together, these dynamics suggest Bolt’s financial sustainability is benefiting from prudent cost containment during continued investment into its research and development pipeline. In clinical-stage biotechnology, controlling the operating burn rate is essential to extend funding runway while advancing candidate molecules through expensive trial phases.

Pipeline Advances Fuel Future Prospects for Bolt’s Immuno-Oncology Candidates

Bolt’s core scientific differentiation rests on its Boltbody™ ISAC technology platform targeting oncology indications through immune system engagement. Two lead programs, BDC-4182 and BDC-3042, represent the forefront of this pipeline with encouraging initial clinical activity disclosed recently [N1]. These agents harness innovative mechanisms designed to selectively activate immune effector functions against tumor cells while minimizing systemic side effects—a key challenge in immuno-oncology therapeutic development.

Success at advancing these candidates through early-phase studies enhances their probability of downstream registration trials and eventual commercialization. Moreover, validation of the Boltbody™ ISAC approach could provide a platform advantage versus competitors focusing on traditional checkpoint inhibitors or CAR-T technologies. The sector continues to reward novel mechanisms that address unmet oncologic needs through robust immune modulation.

Key Clinical Milestones and Regulatory Expectations to Track

Explicit forward guidance remains absent from recent filings; however, standard clinical timelines suggest milestone events to monitor include dose-escalation completions, proof-of-concept efficacy readouts, and progression toward pivotal Phase II/III studies [N1][S1]. Investor diligence should focus on interim data disclosures for both BDC-4182 and BDC-3042 alongside any regulatory feedback—such as FDA fast track designations or breakthrough therapy status—which could materially affect valuation perceptions.

As is typical for clinical-stage firms, any delays or disappointing trial results would heighten risk profiles significantly, whereas positive data could serve as inflection points justifying renewed investor interest.

Capital Allocation Strategy: Managing Cash Flow Through Restructuring

At year-end 2025, Bolt reported cash and equivalents totaling $11.7 million with current assets amounting to approximately $30.3 million versus current liabilities near $8.4 million—translating into a comfortable current ratio of about 3.59 [F1]. This liquidity position reflects efficacy in managing short-term obligations despite ongoing negative cash flows.

Operating cash flow outflows narrowed from roughly -$61 million in 2024 to -$39.85 million in 2025—a significant improvement consistent with reduced spending pace [F1][N1][S2]. Concurrently, capital expenditures remained minimal at only about $72 thousand for the year compared to $41 thousand in 2024 [F1], confirming that the company's capex focus remains primarily on supporting ongoing R&D activities rather than fixed asset expansion.

These indicators highlight management’s disciplined approach toward conserving cash amid costly clinical advancement requirements—balancing necessary investment with expense control achieved partly through restructuring steps taken earlier in the year.

Analyzing Return Metrics and Financial Resilience

Reflective of its early-stage status and continued investment cycle, Bolt posted a net loss of approximately $33.4 million for FY2025 against equity of around $26.5 million—resulting in an estimated negative return on equity (ROE) near -125.9% [F1]. This sharp negative ROE underscores depletion of shareholder capital attributable largely to high research intensity prior to commercialization opportunities being realized.

While such negative returns are expected within the biotech development paradigm—often requiring years before product launch—the metric reinforces the necessity for successful progression along clinical phases to arrest equity erosion and ultimately drive long-term investor value.

Understanding Operational Challenges and Sector-Specific Risks

The company’s SEC filings lay out detailed risk factors centered on intrinsic uncertainties pertinent to clinical research endpoints and regulatory approvals [S1][S2]. Achieving meaningful efficacy signals within patient populations has well-recognized variability; failure at key trial stages would impose material setbacks.

Furthermore, compliance hurdles encompassing GMP manufacturing standards, safety monitoring obligations, and market authorization complexities compound execution risk. Competition within immuno-oncology innovation remains intense with multiple entities pursuing overlapping targets via diverse mechanisms—a landscape requiring sustained intellectual property defense alongside swift development execution.

Financially, maintaining sufficient funding amidst volatile capital markets presents additional challenges given prior equity drawdown trends highlighted above.

Outlook: Potential Catalysts and What Investors Should Monitor

Going forward, investors should closely monitor timelines around anticipated data releases for BDC-4182 and BDC-3042 trials as well as any updates regarding regulatory designations or partnerships that could enhance resource availability [N1][S3]. Awareness of upcoming financing activities or collaboration announcements will also be critical given ongoing cash consumption patterns.

Ultimately, tracking patient enrollment milestones, interim safety/efficacy readouts, plus adaptive strategic responses to sector competition will shape Bolt’s trajectory toward potentially transformative stages within its immuno-oncology focus.

Bolt Biotherapeutics Historical Financial Performance (FY2022-2025)

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 8 | -33 | -40 | -36 | +0.1% | +47.1% |

| 2024 | 8 | -63 | -61 | -73 | -2.4% | +8.8% |

| 2023 | 8 | -69 | -70 | -76 | +37.5% | +21.5% |

| 2022 | 6 | -88 | -77 | -90 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -40 | -125.9 |

| 2024 | -61 | -110.4 |

| 2023 | -70 | -61.4 |

| 2022 | -78 | -51.4 |

Source: SEC companyfacts cache [F1].

All figures USD; revenues represent collaboration/licensing income typical of pre-commercial biotech firms; capex values indicate limited fixed asset spend focused on supporting drug development.

Bolt Biotherapeutics exemplifies a clinical-stage biotechnology company balancing the dual imperatives of scientific advancement within its proprietary Boltbody™ ISAC immuno-oncology framework and disciplined financial management amidst significant operating losses endemic to early-stage drug development cycles. While revenue streams hold stable primarily from partnership-derived sources, substantial progress has been made by halving operating deficits through structural cost optimization measures undertaken during fiscal year 2025.

Yet the path ahead remains intrinsically uncertain given unresolved questions surrounding late-phase clinical validation of lead assets BDC-4182 and BDC-3042 alongside prevailing regulatory scrutiny common across oncology pipelines seeking market approval globally.

This analysis deliberately abstains from forecasting beyond documented disclosures but highlights critical operational parameters central to assessing Bolt's evolving valuation landscape including upcoming trial results cadence and liquidity trajectory against expenditures tied closely to R&D.

Disclaimer: This report is prepared solely for informational purposes without providing investment advice or recommendations regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments