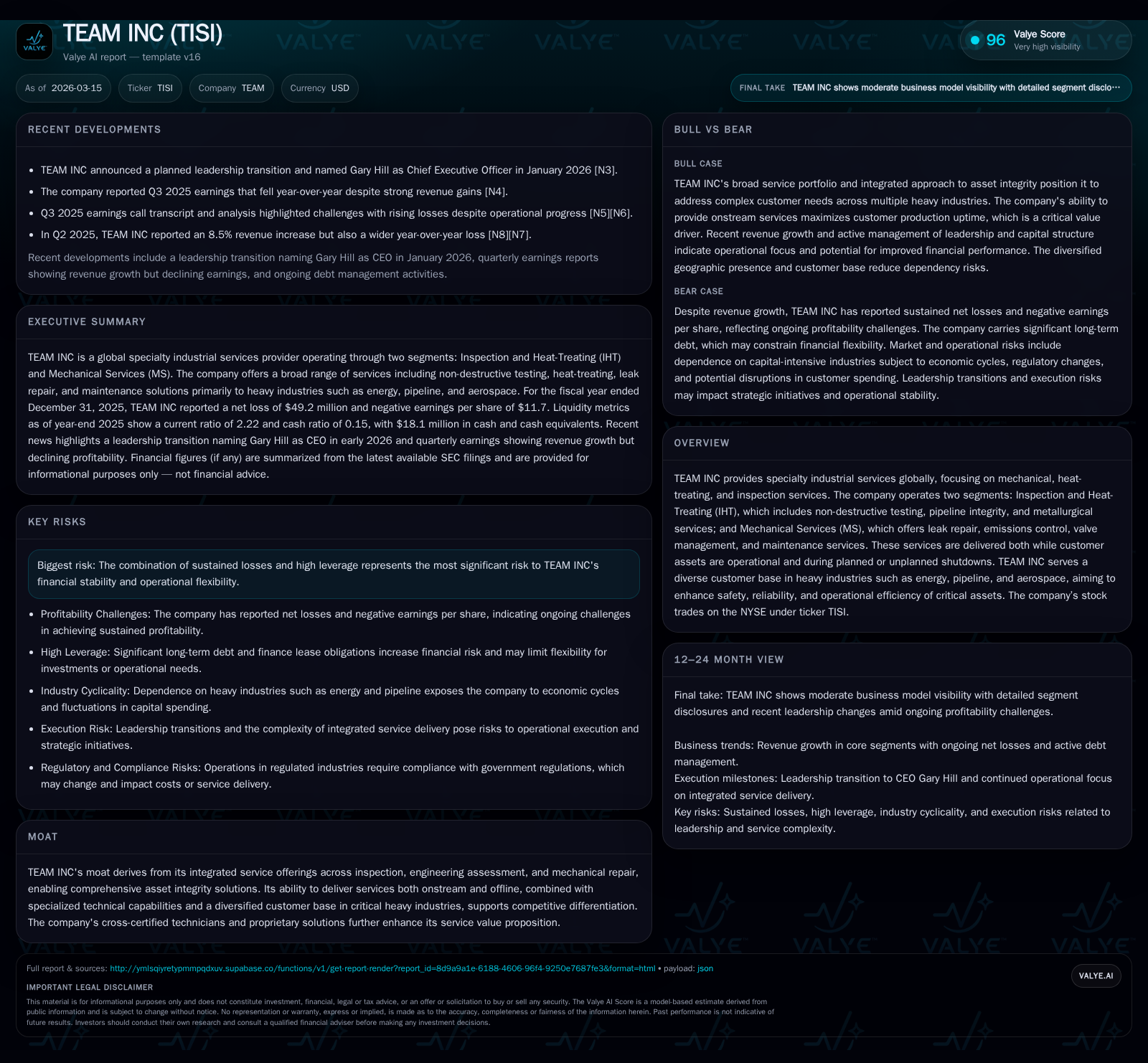

TEAM INC’s Strategic Shift: Integrating Services to Confront Financial Challenges

TEAM INC leverages its integrated inspection and mechanical services to drive revenue growth despite ongoing operating losses and elevated leverage.

TEAM INC has built a distinctive industrial services platform combining inspection, heat-treating, and mechanical repair capabilities that serve critical heavy industries globally. While the company stabilized operating income growth (+38.8% YoY in 2025) and sustained revenue near prior-year levels (-1.1% YoY), it struggles with persistent sizable net losses and negative operating cash flows, pressured by high-interest expenses from leveraged credit facilities. Amendments to debt agreements and a $75 million Series B preferred equity injection highlight management's efforts to enhance liquidity and extend covenant flexibility. Going forward, backlog strength in pipeline integrity and aerospace inspection, along with cross-certified technicians' ability to deliver onstream repairs, remain key growth levers. Monitoring EBITDA performance versus leverage covenants will be critical amid constrained free cash flow and no recent capital return program.

Historical Performance Review: Revenue Trajectory and Profitability Dynamics

TEAM INC’s financial journey over recent years depicts a company grappling with the dual challenge of maintaining revenue while restoring profitability amidst a substantial debt burden. The company reported revenues close to $316 million at fiscal year-end 2017 but has experienced fluctuations since then due to market conditions across its heavy industry client base [F1]. The most recent annual revenue in 2025 was roughly flat relative to the prior year (down by only 1.1%), signaling some stabilization after previous volatile periods.

Crucially, operational results showed improvement in 2025 with operating income rising by nearly 39% YoY to $14.1 million despite ongoing net losses widening to -$49.2 million. This divergence between operating income growth and net loss expansion reflects significant non-operational expenses notably interest costs related to a complex leveraged capital structure [F1]. Operating cash flows also turned negative ($-11.3 million), underscoring the tension between earnings and cash generation.

This imperfect recovery trajectory points to operational execution gains partly offset by financial strain from legacy leverage.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -49 | -11 | 14 | 9 | -28.6% |

| 2024 | -38 | 23 | 10 | 9 | +49.5% |

| 2023 | -76 | -11 | -13 | 10 | -208.1% |

| 2022 | 70 | -58 | -40 | 25 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -21 | 201.0 |

| 2024 | 13 | -2201.7 |

| 2023 | -21 | -166.1 |

| 2022 | -83 | 59.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures fixed at latest available point; YOY calculations based on data in narrative

Drivers of Past Growth: Core Service Segments and Market Reach

TEAM INC's integrated business model consists primarily of two segments: Inspection & Heat-Treating (IHT) and Mechanical Services (MS). IHT covers specialized non-destructive testing (NDT), heat treating components both on operational assets (“onstream”) or during shutdowns, as well as pipeline integrity assessments supported by advanced digital imaging technologies for metallurgical inspections [S1], [S24].

Mechanical Services complements this by delivering leak repair solutions—including composite patches tailored for leak control—and emissions reduction technologies largely aimed at maintaining production uptime through onstream valve insertions and hot tapping techniques that do not require asset shutdowns [S24]. These mechanically intensive offerings extend into planned turnarounds or unplanned outages where cross-certified technicians perform onsite machining or bolted joint repairs within compressed scheduling windows.

TEAM's ability to serve diverse client sectors such as energy infrastructure (including offshore oil & gas pipelines), manufacturing processes, midstream pipeline storage facilities, heavy construction projects, plus aerospace component inspections grants it resilience through diversified demand drivers [S8], [N1].

Moreover, the company emphasizes three service delivery profiles: turnaround/project services for scheduled maintenance; callout services addressing emergent repairs; and nested "run-and-maintain" models supporting continuous asset monitoring—all leveraging multi-skilled technician deployment for cost-efficient response [S24]. This service integration helps create barriers against commoditized pricing while building cross-selling opportunities.

Financial Health Spotlight: Operating Losses and Leverage Risks

Despite operational progress visible in improving operating income figures, TEAM INC faces material financial headwinds caused by its high indebtedness position that constrains flexibility.

As of September 30, 2025, total long-term debt approximated $295 million spread across several tranches including:

- A secured revolving credit facility (ABL Credit Agreement) with commitments raised from $130M to $150M expiring October 2028.

- A First Lien Term Loan totaling roughly $166 million maturing March 2030 with floating interest rates tied to SOFR plus margins adjusted downward upon meeting EBITDA targets.

- A Second Lien Term Loan tranche near $60 million also running through mid-2030 bearing higher effective interest rates (~13.5%-16%) often payable partly-in-kind depending on leverage ratios.

The capital structure undergoes active management via amendments such as ABL Amendment No.7 (September 2025), which extended maturities by one year, increased borrowing capacity under revolver terms, reduced interest margins contingent on performance metrics like Average Historical Excess Availability, and relaxed leverage covenant thresholds temporarily up to a First Lien Net Leverage Ratio of up to 6x until end-2026 .

These covenant relief measures acknowledge ongoing earnings volatility while granting incremental breathing room; however, they underscore the ongoing risk embedded in sustaining profitable operational performance sufficient to meet rising fixed charges.

Interest paid YTD through Q3’25 totals several millions annually (~$15M range combining all tranches), further pressuring cash flows given negative CFO reported for FY25 [-$11M] [S4], [F1].

Future Growth Outlook: Backlog, Market Demand, and Segment Potential

Management commentary along with analyst observations highlight a solid demand pipeline backed primarily by increased focus on pipeline safety regulation compliance and aerospace reliability programs requiring frequent NDT inspections onboard critical components—a recurring market feature driving steady workflow for the IHT segment [N1], [S3].

The intrinsic advantage of offering onstream mechanical services means clients can optimize uptime without sacrificing asset integrity—an increasingly valuable differentiator amid tightening regulatory scrutiny on emissions control especially in midstream environments dealing with volatile organic compounds.

While detailed backlog figures remain undisclosed publicly as of filing dates reviewed, implicit visibility comes from disclosed multi-year contracts renewal appetite—particularly among energy firms navigating infrastructure aging—that supports growth prospects in specialty industrial services focused on asset integrity management.

Technicians cross-trained across IHT/MS disciplines constitute a flexible labor pool able to serve dynamic customer demands ranging from urgent callouts post-failure events to preventive nested maintenance engagements intended to reduce unplanned outages—bolstering recurring revenue stability beyond project-based spikes [S24].

Key Financial Metrics: Margins, Cash Flow Trends, and ROE Analysis

Margins show an encouraging trajectory; operating income rose by nearly +39% YoY even as net losses widened due mainly to financing costs escalation stemming from leverage increases post refinancing transactions [F1]. This margin expansion at the EBITDA level underscores better cost controls or higher-margin contract mix but remains insufficient currently to drive positive net profitability.

Operating cash flow trends present more concern—flipping from positive $22.8 million in FY24 back into negative territory of about -$11.3 million in FY25 due partly to working capital swings plus non-cash items such as amortization of debt issuance costs pushing out cash generation horizon.

An indicative return on equity calculation using net loss over negative shareholder equity (-$24.5 million) is less meaningful here given insolvency appearance; however the continued erosion reflects growing balance sheet stress that pressures credit ratings and cost of capital considerations [F1].

Free cash flow is significantly negative (~-$20 million estimated by subtracting capex from CFO) which limits ability to self-fund growth initiatives or shareholder returns absent external financing injections.

Capital Structure and Liquidity: Debt Facilities, Amendments, and Covenant Flexibility

A granular look at TEAM INC’s debt arrangements reveals a heavily layered secured lending framework designed recently for both liability management and liquidity enhancement:

- The Amended Credit Agreements incorporate tiered leverage covenants increasing maximum permitted ratios temporarily (up to First Lien Net Leverage Ratio of 6x until Dec-31, 2026 followed by expected reversion).

- Interest rate margins benefit from step-down clauses allowing up to ~0.375% coupon reductions aligned with quarterly EBITDA achievements—thus incentivizing operational improvement tightly linked with cost savings across borrowing costs.

- Principal payments are minimal currently ($438k quarterly minimums) signifying measured amortization schedules focused on preserving liquidity over rapid deleveraging.

- Letters of credit outstanding nearly $9.5 million provide contingent liquidity support without impacting immediate borrowing base capacity.

- Repayment actions preceding amendments included partial prepayments exceeding tens of millions targeting higher-cost equipment finance loans or second lien term loans which optimize blended interest outlays [[S4]-[S6]].

Together these illustrate an active but cautious approach managing restrictive covenants while balancing borrowing costs against necessary operational funding.

Evaluating Capital Allocation: Capex Trends, Dividends, and Share Buyback History

Capital expenditures have moderated slightly year-over-year falling about 2% from just under $9.5 million in FY24 to roughly $9.3 million in FY25 reflecting steady investment aligned largely toward maintenance rather than expansion CAPEX typical within capital-intensive specialty industrial services where machinery uptime underpins service capability reliability [F1].

Notably there are no dividends declared nor share repurchases executed recently—the last known buyback program ended years prior—reflecting prudent preservation of capital amid ongoing negative free cash flow status targeting deleveraging priorities over shareholder returns currently.

Cash reserves stood at about $18 million end-FY25 while current ratio exceeding 2x indicates sufficient short-term liquidity buffer relative to liabilities allowing fundamental operations continuity yet constrained for opportunistic share repo activity absent robust CFO improvements or equity infusions [F1].

What Investors Should Watch: Upcoming Milestones and Risk Factors

Looking ahead stakeholders should focus closely on these pivotal developments:

- Debt covenant tests tied directly to EBITDA thresholds occurring quarterly through end-2026 that will determine access limits under both First Lien Term Loan and Revolving Credit facilities potentially triggering accelerated repayments or penalty interest if breached.[S23]

- Execution risk tied to converting pipeline integrity contracts backlog into revenue amid competitive pressure as well as successful delivery within aerospace component inspection regimes ensuring repeat business wins.[N2]

- Potential draws under Series B delayed draw options providing up to additional $30 million subject to meeting leverage criteria could materially affect liquidity dynamics.[S29]

- Macro factors including changes in environmental regulation enforcement impacting demand for emissions control repairs; labor market conditions affecting technician availability; inflation-driven cost pressures influencing margin structures.[S23]

- Legal proceedings or regulatory investigations disclosed historically remain limited but must be monitored as compliance mandated areas remain sensitive.[S23]

- Management’s efficacy integrating diverse service lines efficiently balancing turnaround project services with nested maintenance routings will critically influence margin sustainability going forward.Sustained bottom-line losses alongside persistent negative free cash flows could constrain strategic optionality absent meaningful earnings inflection or structural deleveraging success.

This report synthesizes TEAM INC’s current operational stance built around its unique integrated specialty industrial services model reinforcing strong service differentiation via cross-certified technicians capable of delivering robust onstream inspection/repair programs crucial for critical heavy industries globally.[N1][S1][S24] However prevalent net losses combined with elevated debt levels necessitate vigilant monitoring of covenant compliance alongside strategic initiatives aimed at steadily improving EBITDA generation underpinning sustainable deleveraging.[F1][S4][S6] Investors should consider prospective contract wins/losses along with upcoming financing milestones while recognizing inherent risks tied chiefly to financial rigidity exacerbated if adverse market conditions weaken underlying asset utilization trends.[S23]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments