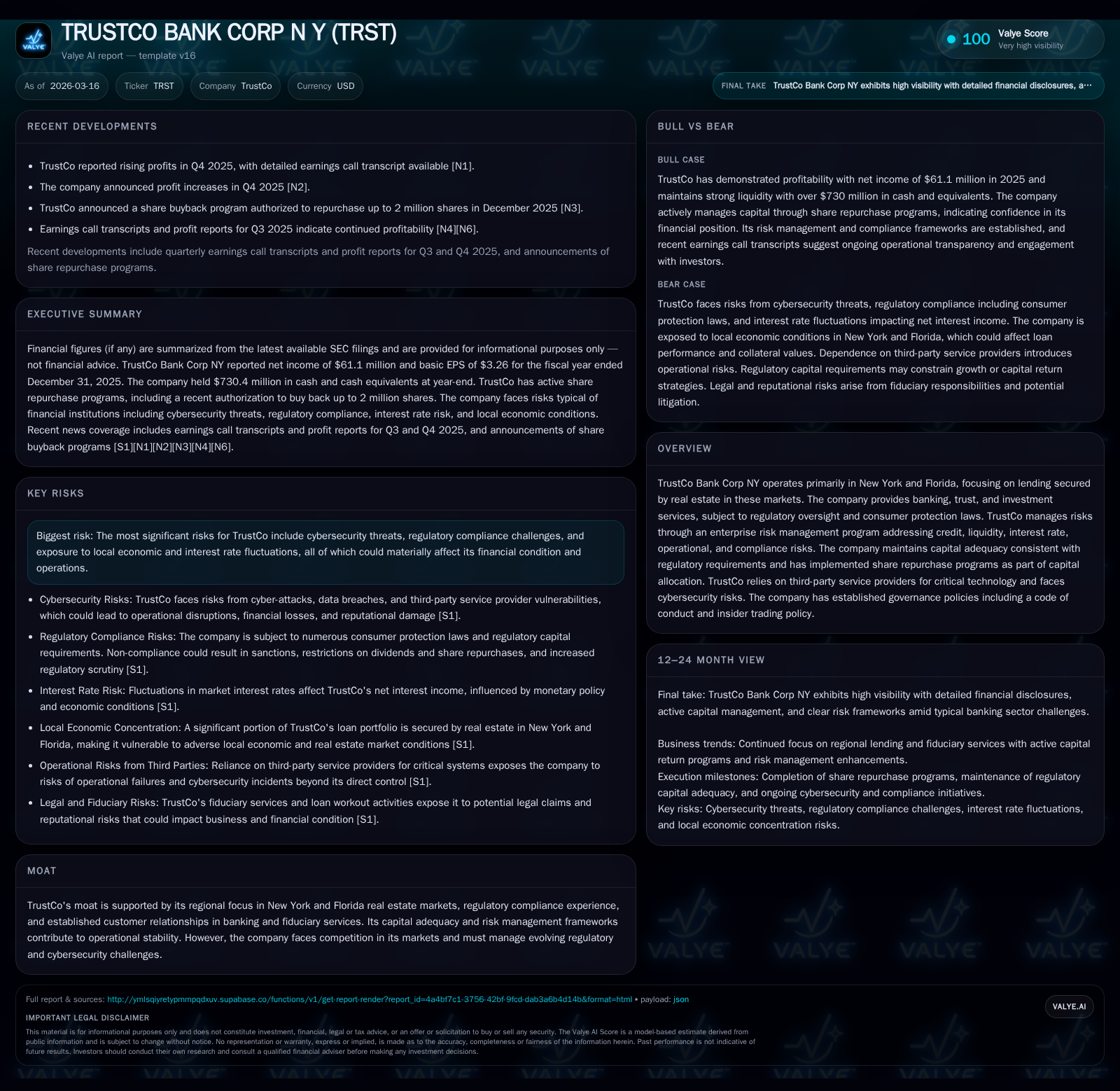

TrustCo Bank’s Performance Rebound and Strategic Capital Moves

TrustCo Bank achieved a notable recovery in net income in 2025, underpinned by strategic capital management and a steadfast focus on its regional lending markets.

TrustCo Bank Corp NY reported a significant rebound in 2025 net income with a 25.2% year-over-year increase, recovering from prior fluctuations largely driven by its real estate secured lending in New York and Florida. The bank’s capital allocation strategy emphasized stable dividends alongside a sharp increase in share buybacks, supported by robust liquidity with over $730 million in cash and equivalents. While ongoing Federal Reserve rate cuts create net interest income sensitivities, TrustCo sustains disciplined risk management addressing credit, regulatory, and cybersecurity challenges. Looking forward, growth is poised to hinge on local economic conditions and competitive pressures with no explicit forward guidance disclosed.

Historical Financial Performance and Year-on-Year Drivers

TrustCo Bank Corp NY demonstrated a meaningful rebound in net income for fiscal year 2025, delivering $61.1 million compared to $48.8 million in 2024—a substantial 25.2% increase from the previous year that followed a pullback in FY2024 [F1]. This inflection underscores the bank's ability to navigate through volatile operating conditions.

Operating cash flow showed a mild contraction of approximately 3.1% year-over-year to $57.6 million in FY2025, indicating some pressures on cash generation despite improved profitability [F1]. Notably, capital expenditures more than doubled from $4.9 million to $11.9 million—a strategic ramp likely invested in technology or branch enhancements consistent with expanding service capabilities [F1].

Equity grew steadily over the four-year period ending at nearly $687 million by late 2025, bolstering the balance sheet amid incremental retained earnings accumulation—a reflection of healthy capital retention given stable dividend payouts [F1]. Dividends remained consistent near $27.6 million annually across this timeframe while buybacks surged dramatically to about $38.1 million in FY2025 from just $374 thousand the previous year, highlighting an active capital return strategy alongside measured payout discipline [F1][S4][S5].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 61 | 58 | 12 | +25.2% |

| 2024 | 49 | 59 | 5 | -16.7% |

| 2023 | 59 | 64 | 6 | -22.0% |

| 2022 | 75 | 79 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 28 | 38 | 46 |

| 2024 | 27 | 0 | 55 |

| 2023 | 27 | 0 | 58 |

| 2022 | 27 | 7 | 75 |

Source: SEC companyfacts cache [F1].

Table: Fiscal Year Performance Summary (FY2022–FY2025). Figures rounded; all USD; sourced from [F1]

Interest Rate Environment and Net Interest Income Sensitivities

TrustCo operates predominantly with real estate-secured loans concentrated regionally in New York and Florida markets where approximately 64% of loans are New York-based and around 36% Florida-based [S14]. A significant proportion of these loans carry fixed rates or are initially fixed for long tenors (five to ten years), making net interest income sensitive to changes in interest rate environments due to potential repricing mismatches.

Following a peak federal funds target range of 5.25–5.50% through late-2023 and early-2024 periods, the Federal Open Market Committee initiated six rate cuts spanning a total of approximately 175 basis points during calendar years 2024–25 to reach a range of roughly 3.50–3.75% by December 31st 2025 [S1][S20]. This retreat introduces reinvestment risks whereby prepayment rates may accelerate as borrowers refinance into lower-cost loans reducing loan yields; alternatively slower prepayments during rising rates could pressure cash flow reinvestment capabilities.

Moreover, TrustCo faces potential erosion of net interest income if deposit expense rates adjust faster than asset yields given shorter duration liabilities versus longer-term fixed assets—a classic asset-liability management concern exacerbated by current macroeconomic uncertainty and potential inflation persistence impacting Federal Reserve actions going forward [S1][S20].

Risk Management: Navigating Regulatory Compliance and Cybersecurity Challenges

TrustCo maintains comprehensive enterprise risk management addressing credit quality monitoring alongside liquidity controls and regulatory compliance frameworks including adherence to consumer protection laws such as the Community Reinvestment Act (CRA) and fair lending statutes enforced by agencies like CFPB and DOJ [S6][S7]. These frameworks mitigate risks posed by potential sanctions or fines arising from noncompliance.

Cybersecurity remains a critical focus area given increasing threats including fraud schemes such as phishing or ransomware attacks compounded by reliance on third-party service providers operating elements of communications and IT infrastructure [S13][S19]. While no material losses have been reported due to breaches so far,[S19] ongoing vigilance is mandated due to evolving threat sophistication.

Operational risks related to anti-money laundering regulations under Bank Secrecy Act requirements also necessitate rigorous monitoring for suspicious activity reporting; lapses could trigger regulatory penalties affecting reputation and operations [S7][S9]. Lending concentration in real estate further exposes credit risk dependent on local property values influenced by regional economic health factors such as employment levels or inflation pressures which could impair borrower repayment capacity during downturns [S14].

Capital Allocation Priorities: Balancing Dividends and Share Repurchases

TrustCo exhibits prudent capital deployment balancing shareholder returns with conservative balance sheet management.

Annual dividends have remained consistent near $27 million without significant increases indicating payout stability attractive to income-focused investors while share repurchase activity accelerated markedly in FY2025 totaling approximately $38 million versus nominal buybacks previously.[F1] This reflects execution against board-authorized programs: an earlier program completed repurchases of one million shares by December 11th 2025 while a new program authorized up to two million shares through December 31st 2026 provides ongoing repurchase flexibility aligned with market valuations and liquidity positions [S4][S5].

Capital expenditures doubling likely reflects investments targeting technological upgrades or expansion initiatives required for competitiveness amid evolving financial services delivery models including digitization—a key factor given fintech disruption risks.[F1][S22]

Liquidity Position and Capital Structure Overview

TrustCo’s liquidity remains robust with cash and equivalents exceeding $730 million at fiscal year-end supporting normal loan disbursements alongside contingencies against market shocks or deposit outflows potentially triggered by fintech alternatives attracting low-cost funds away from traditional deposits [F1][S8][S10].

The equity base nearing $687 million provides capital adequacy consistent with supervisory expectations where regulators may require buffers beyond minimums especially post industry stress episodes among regional institutions comparable in size [F1][S25].

Strategic Outlook: Market Opportunities Amid Regional Concentration Constraints

The geographic focus on New York/Florida real estate lending serves as both strength—entrenched customer relationships—and constraint exposing growth directly to cyclical housing trends influenced by local economic factors including employment conditions and monetary policy.

Competitive pressures arise from larger banks leveraging diverse funding sources alongside fintech innovations diverting transactions traditionally routed via banks—exerting margin compression risks via pricing pressures on loans/deposits coupled with deposit volatility linked to digital wallet adoption or alternative investment choices accessible directly by consumers/business clients.[S22][S26]

No explicit future guidance has been disclosed; thus monitoring Federal Reserve policy shifts influencing net interest margins plus evolving regulatory developments affecting lending constraints or compliance costs will be crucial for assessing future earnings prospects.

Key Milestones To Watch

- Progress under the December-initiated stock repurchase authorization allowing up to two million shares through end-2026 will indicate management’s capitalization strategy responsiveness amid market conditions.[S4][S5]

- Quarterly dividend declarations remain a barometer of earnings confidence; any deviation warrants scrutiny especially if paired with shifts in capital return mix signals.[S3]

- Federal Open Market Committee decisions impacting interest rates will critically affect asset-liability dynamics influencing net interest income sustainability.[S1]

- Regulatory updates around fair lending enforcement or cybersecurity compliance costs should be monitored for potential operational impacts.[S6][S7]

Disclaimer: This analysis is based solely on publicly available information as of March 16th 2026 and does not constitute investment advice regarding TRUSTCO BANK CORP N Y (TRST) securities or strategies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments