LAMY Balances Educational Gaming with Breakthrough Cancer Tech Expansion

LAMY’s transition from educational gaming into oncology via acquisition raises questions about its financial footing and strategic coherence.

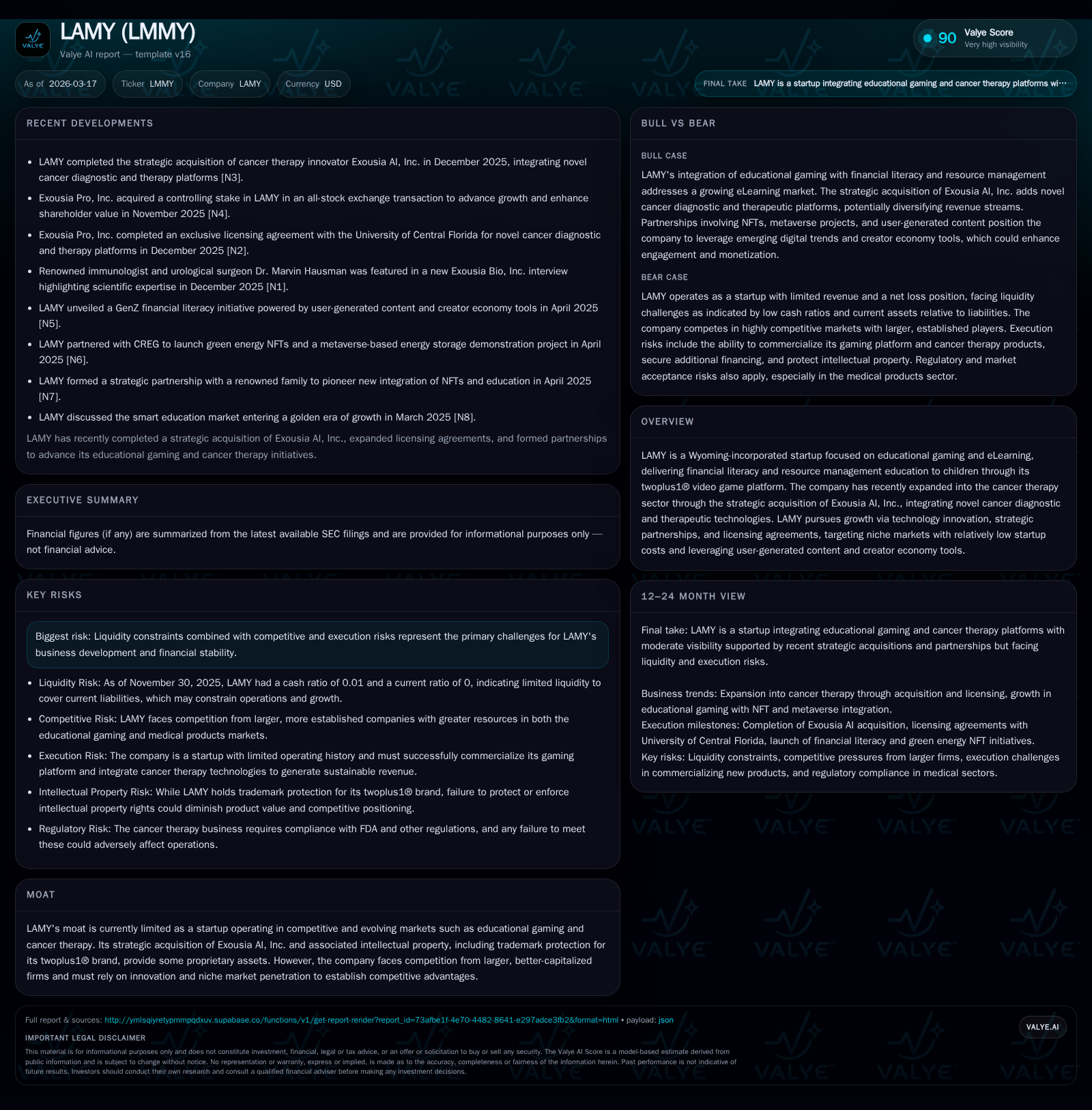

LAMY, a Wyoming-registered startup focused on an educational gaming platform teaching financial literacy to children, has recently diversified by acquiring Exousia AI, Inc., a cancer diagnostics and therapeutics company. This dual-sector strategy introduces operational complexity amid persistent liquidity challenges and competitive pressures. Historically, LAMY has generated minimal revenues with operating losses and relies heavily on related-party loans and convertible debt. The company faces significant execution and funding risks as it seeks to integrate oncology assets while scaling its gaming platform.

Genesis and Early Momentum: Building on Educational Gaming

LAMY was incorporated in Wyoming in early 2022 to develop an eLearning solution focused on imparting financial knowledge to children. Its flagship product, the twoplus1® video game platform, aims to provide an immersive learning experience around finance and real estate concepts. The company’s revenue model centers on competitive subscription fees supplemented by monetizable features such as virtual property trading commissions [S1].

Trademark protection for twoplus1® has been secured primarily in the United Kingdom with additional filings underway, establishing a foundational intellectual property asset important for niche market positioning [S1]. Despite numerous competitors in edtech gaming, LAMY leverages a low startup cost model to attempt market penetration. However, growth has been limited; revenues remain minimal relative to operating expenses. Management highlights innovation-driven cost advantages and proximity to clients compared with larger incumbents as key strategic levers [S1].

Strategic Shift: Acquiring Exousia AI and Entering Oncology

In December 2024, following a change-in-control transaction appointing Zhang Shengwu as sole director and CEO, LAMY acquired Exousia AI, Inc., specializing in cancer diagnostic and therapeutic technologies [S1]. This acquisition marks a significant expansion beyond LAMY’s original gamified financial literacy focus.

This diversification introduces operational complexities as LAMY must allocate resources across two vastly different sectors. Oncology requires navigating highly regulated environments with clinical validation needs and substantial R&D investment—areas without prior company experience. While Exousia AI brings innovative intellectual property targeting critical unmet medical needs, execution risks are heightened amid nascent commercialization capabilities [S1].

Market Position and Competitive Hurdles in Distinct Niches

LAMY now operates within two fiercely competitive industries: educational technology/gaming and biotechnology. The edtech sector is dominated by large firms with extensive content libraries and brand recognition. Oncology diagnostics face steep regulatory barriers, long development cycles, and stringent clinical standards.

The company's moat remains limited despite trademark protections for twoplus1®, as it struggles to scale user adoption against entrenched competitors [S1]. No public clinical data or manufacturing scale accompanies the newly acquired biotech assets, underscoring LAMY's early-stage position outside established competitive domains.

Financial Pulse Check: Historical Performance and Liquidity Challenges

LAMY's financials reflect typical pre-commercial stage patterns characterized by minimal revenue overshadowed by operating expenses focused on administration and development. Reported revenues were approximately $3,750 during the nine months ended February 28, 2025 (down from $7,750 prior year), indicating limited commercial traction [S20].

Operating expenses have resulted in net losses offset partially by other income during some periods; cash flow from operations has ranged from negative $11,070 to negative $1,028 over comparable periods demonstrating fragile cash dynamics [S20,S21]. Capital expenditures relate mainly to intangible asset investments tied to acquisitions but remain modest given lack of mature infrastructure [S15].

Liquidity pressures are evident: total liabilities exceeded total assets at recent reporting dates with zero cash balances reported multiple times across quarters [S7,S22,S23]. The balance sheet shows reliance on related-party advances (~$12.9 million current liabilities as of May 31, 2025) plus notes payable totaling approximately $39 million including related parties; accrued interest liabilities exceed $11 million reflecting rising financing costs [S7].

| Fiscal Year End | Revenue (USD) | Net Income (USD) | Operating Cash Flow (USD) |

|---|---|---|---|

| FY22-23 | 7,750 | (20,554) | (11,070) |

| FY23-24 | 3,750 | 54,895 | (1,028) |

| FY24-25* | N/A | (31,814) | (3,500) |

*Partial year figures based on interim filings ending August or February

Capital Structure Realities: Debt Profile and Financing Risks

The company lacks traditional credit facilities or committed bank lines; financing has relied on intermittent shareholder injections and debt issuances with uncertain timing or amounts [S3,S4,S5]. In January 2026 LAMY issued a $250K convertible promissory note bearing 15% interest that converts at steep discounts creating material dilution risk for shareholders [S27].

Going concern disclosures appear repeatedly due to ongoing liquidity constraints without secured funding plans beyond anticipated equity raises [S6,S12,S13]. This pattern is characteristic of early-stage ventures facing aggressive R&D spending alongside minimal income generation.

Future Prospects: Innovation Execution and Funding Imperatives

Management emphasizes innovation within both gaming education—aiming to enhance user-generated content—and licensing strategies targeting scalable digital market penetration [S1]. Oncology segment growth depends critically on successful integration of proprietary diagnostic or therapeutic assets acquired through Exousia AI.

However absence of concrete near-term financing plans beyond speculative equity offerings introduces significant uncertainty regarding operational sustainability given persistent high cash burn rates [S5]. Profitability hinges on successful execution across these diverse verticals requiring distinct capabilities rarely combined effectively at this stage.

Governance Changes and Risk Factors

The December 2024 change-in-control replaced prior management entirely with Zhang Shengwu consolidating leadership roles as sole director and CEO—typical for small startups undergoing strategic pivots [S1]. Material risks include liquidity shortfalls compounded by intense competition spanning both edtech giants and biotech innovators facing regulatory scrutiny [S18]. Legal exposures related to product quality or IP enforcement also present potential challenges given limited internal infrastructure disclosed.

Milestones to Monitor Going Forward

Absent formal guidance or detailed forecasts within SEC filings, key indicators include:

- Progress integrating Exousia AI’s oncology assets including pipeline advancement,

- Subscriber growth rates and retention metrics for twoplus1® driving recurring revenue,

- Announcements of capital raises or amended credit arrangements extending runway,

- Operating expense trends relative to revenue movement signaling cost control effectiveness,

- Strategic partnerships or licensing deals validating expansion efforts.

Tracking these milestones will help clarify whether LAMY can capitalize meaningfully on its unconventional dual-sector strategy or if resource constraints necessitate strategic recalibration.

This analysis is based solely on referenced SEC filings through March 17th, 2026 ([S1]-[S28]) without extrapolation beyond documented facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments