MBX Biosciences Navigates Early-Stage Challenges with Expanding Peptide Therapy Pipeline

MBX Biosciences continues to invest heavily in its peptide-based therapeutic pipeline while managing significant operating losses and maintaining strong liquidity.

MBX Biosciences, focused on peptide therapeutics for metabolic diseases, recorded a net loss of $86.97 million in 2025 amid intensifying R&D and operational expenses. The company’s cash reserves of approximately $75.3 million support ongoing operations into 2029 under current plans. Its clinical pipeline includes three main candidates, with plans to add two obesity-related therapies in 2026. MBX relies on exclusive intellectual property licensed from Indiana University Research and Technology Corporation, forming a core competitive asset. While facing typical biotech risks including regulatory uncertainties and capital requirements, recent insider buying signals management confidence despite market caution.

Company Overview and Financial Performance

Founded in 2018, MBX Biosciences is developing peptide-based therapies targeting metabolic diseases such as obesity. The company remains pre-commercialization without approved products.

In fiscal year (FY) 2025, MBX reported a net loss of $86.97 million, worsening from a net loss of $61.92 million in FY 2024—a decline of about 40.5%. Operating losses increased by approximately 43.8% to $98.06 million in FY 2025 compared to $68.19 million in FY 2024 [F1]. These losses primarily reflect intensified research and development (R&D) activities alongside general administrative costs.

Operating cash flow (CFO) also contracted by roughly 46%, registering -$79.95 million in FY 2025 versus -$54.68 million the prior year, indicating higher cash burn related to clinical progression and operational expenses. Capital expenditures more than doubled year-over-year to $1.93 million but remain modest relative to total spending, likely supporting infrastructure expansion or manufacturing partnerships [F1].

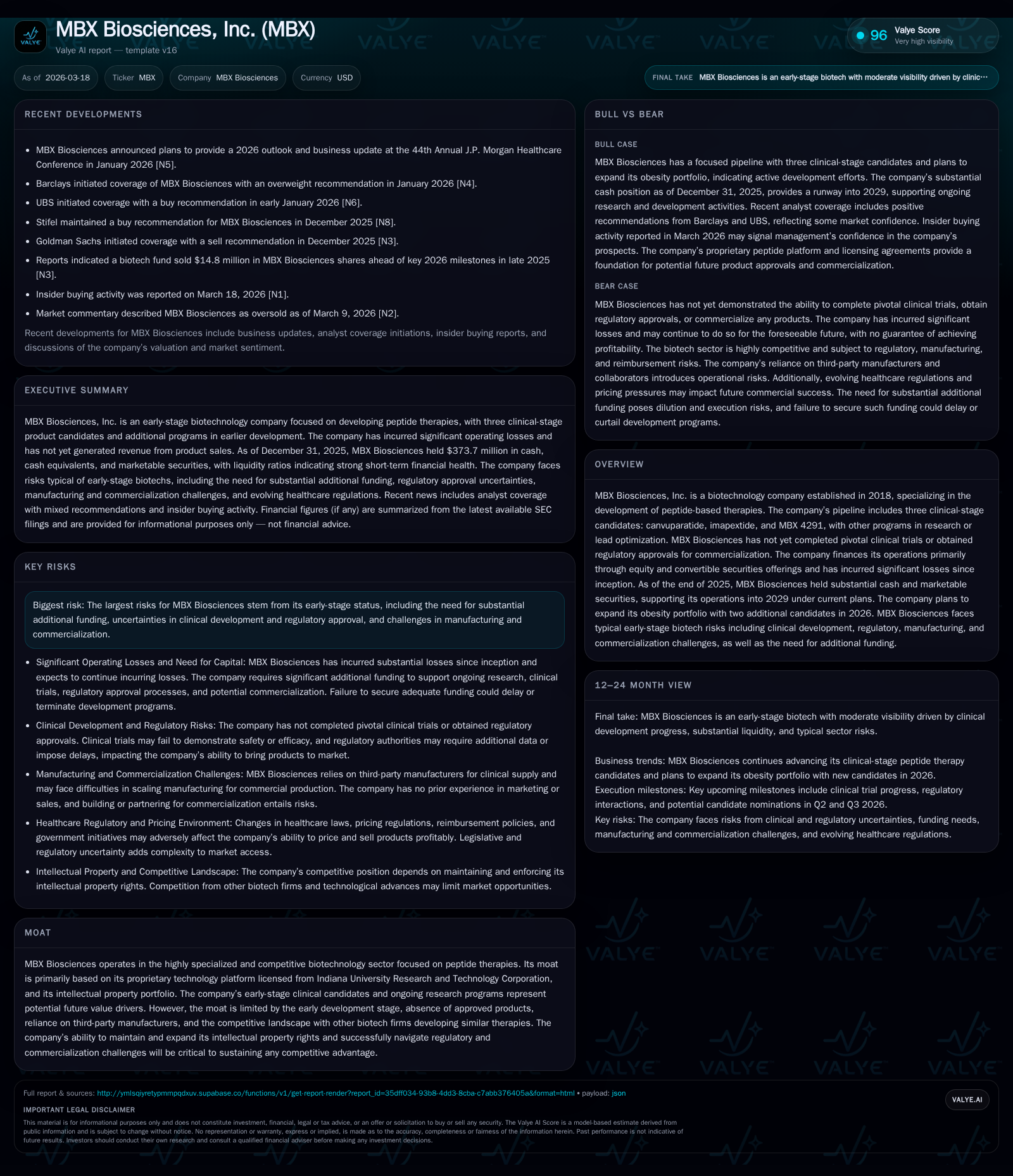

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -87 | -80 | -98 | 1929000 | -40.5% |

| 2024 | -62 | -55 | -68 | 874000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -82 | -23.6 |

| 2024 | -56 | -24.1 |

Source: SEC companyfacts cache [F1].

The absence of revenue is consistent with MBX's early-stage clinical status.

Shareholders’ equity increased substantially to $369.22 million at the end of 2025 from $257.44 million a year earlier as the company funded operations mainly through equity issuances and convertible securities [F1][S14]. This growth supports an approximate negative return on equity (ROE) of -23.6%, reflecting sustained losses against rising equity.

Intellectual Property Position

MBX holds an exclusive royalty-bearing license from Indiana University Research and Technology Corporation (IURTC), granting rights to foundational patents developed by Dr. DiMarchi's team covering innovative peptide technologies critical for its therapeutic programs [S6]. This IP serves as a key competitive differentiator but also exposes MBX to risks related to third-party challenges or potential disputes over patent validity or scope.

Pipeline Development

The company advances three clinical-stage candidates:

- Canvuparatide: An obesity-targeted peptide therapy.

- Imapextide: Another candidate addressing metabolic conditions.

- MBX 4291: A candidate further along development paths.

Additionally, MBX plans to expand its obesity portfolio with two new molecules slated for advancement in 2026 [N2][S1]. These developments align with growing market demand for effective metabolic disease treatments.

Regulatory Landscape and Risks

MBX operates within a complex regulatory environment typical for biopharmaceutical companies but faces added uncertainty following the U.S Supreme Court's July 2024 decision that reduced deference given to FDA interpretations—potentially leading to longer approval timelines or additional data requirements [S12].

Further regulatory risks include compliance with evolving healthcare fraud and abuse laws as well as challenges stemming from drug pricing reforms and reimbursement policies that could impact future commercial success [S11][S20].

Capital Allocation and Liquidity Position

With no product revenues yet generated, MBX depends on capital raises via equity offerings and convertible instruments to fund R&D and operations.

As of December 31, 2025:

- Cash and cash equivalents totaled $75.29 million,

- Current assets stood at $381.54 million,

- Current liabilities were $15.50 million, giving a strong current ratio of approximately 24.62 which provides substantial liquidity buffer for near-term operations [F1][S14].

Despite this liquidity strength, free cash flow remains negative with an estimated deficit of approximately $81.88 million in FY25 (operating CFO minus capex), underscoring the need for continued financing ahead of revenue generation milestones [F1].

No dividends or share repurchases have been declared consistent with prioritizing reinvestment into clinical programs during this early stage.

Market Sentiment and Insider Activity

Insider buying activity reported in March 2026 suggests confidence from management or board members despite ongoing financial losses—contrasting with market analyst views categorizing MBX shares as oversold amid price declines reflective of inherent early-stage biotech risks [N1][N2].

Summary

MBX Biosciences exemplifies the profile of an early-stage biotechnology firm balancing promising scientific innovation with significant operational losses and capital needs. Its proprietary licensed peptide platform targeting metabolic diseases positions it well strategically; however, critical inflection points remain tied to clinical trial outcomes and regulatory approvals.

Robust liquidity supports ongoing development activities into the foreseeable future though sustained negative cash flows necessitate further financing rounds before achieving profitability.

Investors should monitor upcoming clinical milestones, regulatory developments influenced by evolving FDA policies post-2024 Supreme Court ruling, patent litigation risks inherent in the biotech sector, as well as broader healthcare policy shifts affecting drug pricing and reimbursement frameworks.

This analysis is based on publicly available data as of March 18, 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments