Dollar General's Growth Momentum Meets Operational Efficiency and Risk Oversight

Dollar General leverages its rural store network and operational discipline to deliver strong financial results amid evolving retail dynamics.

Dollar General Corporation operates a vast network of discount stores primarily in underserved rural and suburban areas, targeting value-conscious consumers with a broad mix of low-priced goods. The company’s recent fiscal year showed a robust rebound in operating income and net profit, driven by effective cost controls and steady same-store sales growth. Its future growth hinges on expanding store footprint and maintaining price competitiveness while managing risks including cybersecurity threats and sector competition. Capital allocation favors dividends and share buybacks, supporting shareholder returns alongside sustained investment in existing operations. Monitoring quarterly performance milestones will be critical for assessing continuation of these trends.

Company Overview

Dollar General Corporation stands as a dominant discount retailer focusing on value-driven consumer segments predominantly in rural and suburban United States areas. The company offers a comprehensive product mix including consumables, seasonal items, apparel, and home products at low price points designed to cater to budget-conscious shoppers seeking convenience. Its business model is underpinned by high inventory turnover and tight operational cost controls enabling competitive pricing.

Historical Financial Performance

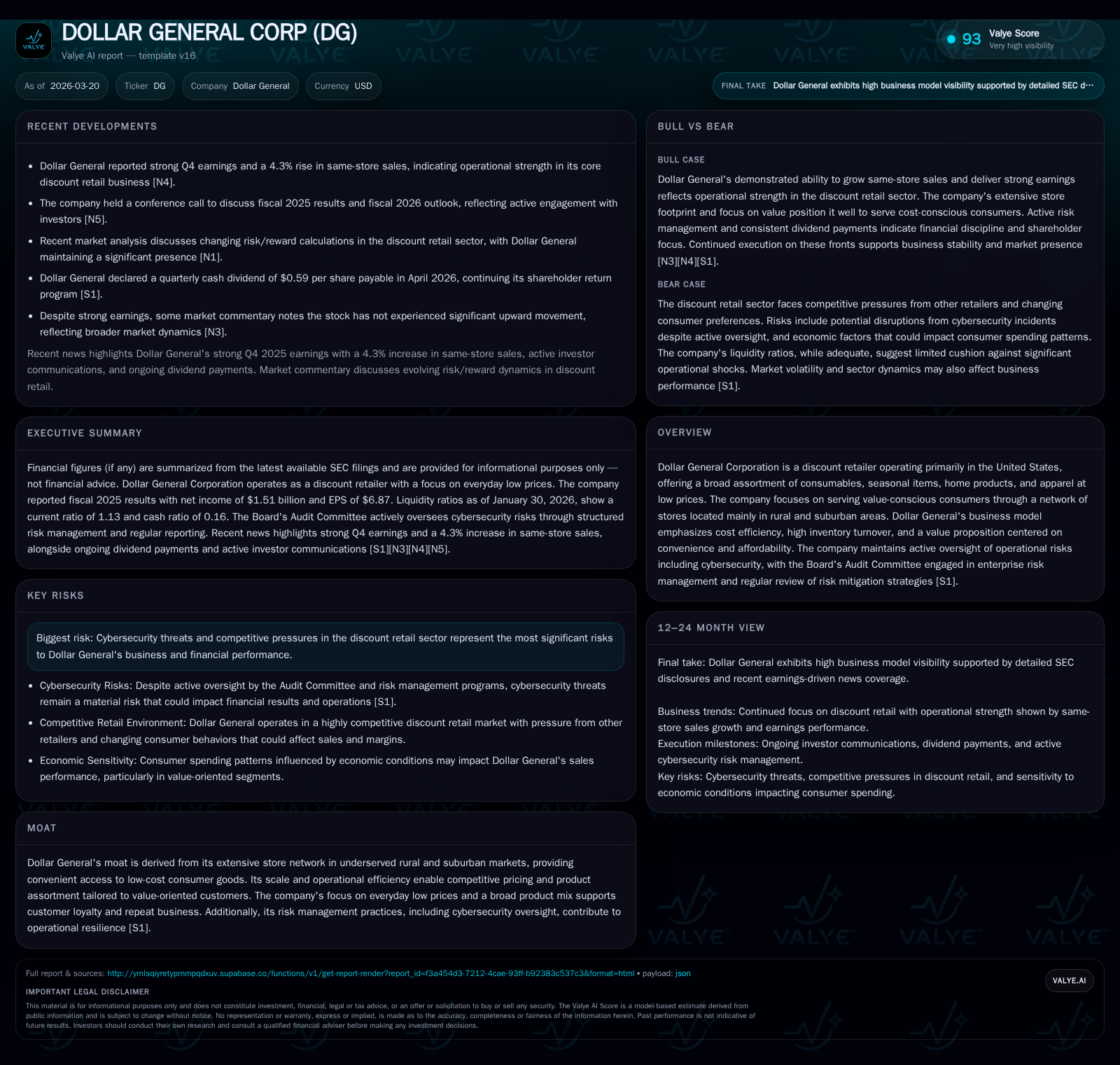

Fiscal year 2025 marked a notable recovery phase for Dollar General. Operating income reached $2.20 billion, up 28.6% from the prior fiscal year’s $1.71 billion [F1]. Net income widened even more significantly by 34.4%, totaling $1.51 billion compared to $1.13 billion the previous year [F1]. This uplift was supported by effective overhead management and positive same-store sales growth, reported at +4.3% for Q4 alone [N3].

Operating cash flow expanded robustly by over 21%, hitting $3.63 billion, evidencing strong underlying earnings quality and working capital efficiency [F1]. Capital expenditures dipped modestly by about 5%, reflecting optimized allocation between new store openings versus sustaining existing assets [F1]. The resulting free cash flow was approximately $2.4 billion, offering ample flexibility for capital returns.

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1.5 | 3.6 | 2.2 | 1241 | +34.4% |

| 2024 | 1.1 | 3.0 | 1.7 | 1310 | -32.3% |

| 2023 | 1.7 | 2.4 | 2.4 | 1700 | -31.2% |

| 2022 | 2.4 | 2.0 | 3.3 | 1561 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 520 | 2.4 | |

| 2024 | 519 | 2.7 | 1.7 |

| 2023 | 518 | 2.7 | 0.7 |

| 2022 | 494 | 2.7 | 0.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue data was not provided explicitly in the sources.

Growth Prospects

Going forward, Dollar General’s growth trajectory rests on two pillars: continued expansion of its physical footprint primarily in less densely populated regions underserved by competitors and bolstered productivity through enhanced assortments aligned with evolving consumer preferences [S1]. The retailer has demonstrated an ability to adapt its merchandise mix rapidly and maintain everyday low prices attractive during economic uncertainty.

Expansion potential exists but may face limitations due to saturation challenges in certain markets or shifts in consumer behaviors toward e-commerce channels where Dollar General's presence is more limited relative to peers. Competitive pressures from other discount chains also represent ongoing headwinds that require sustained operational agility.

Forecasts and Milestones

The company outlined a fiscal year 2026 outlook coinciding with its earnings release on March 12 that highlights confidence in maintaining positive same-store sales trends alongside measured new store growth initiatives [N2,S3]. Market consensus remains watchful for margin trajectories given input cost volatility.

Key upcoming milestones include monitoring Q1 FY2026 earnings that will provide insights on inflation pass-through efficacy and the impact of recent leadership appointments such as the Chief Operating Officer transition aimed at driving merchandising innovation [S24].

Returns and Capital Allocation

Dollar General maintains a disciplined approach to capital allocation balancing reinvestment with consistent shareholder returns. Annual dividends approximate $520 million with quarterly payments stable at $0.59 per share as declared in early March [F1,S17].

Though share repurchase activity slowed compared to earlier years—absent explicit figures for FY2025 buybacks—the historic pattern shows robust buyback programs around $2.7 billion annually fostering EPS accretion . Liquidity remains healthy with over $1.13 billion in cash equivalents and a current ratio near 1.13 signaling solid short-term solvency [F1].

Return on equity stood near an estimated 17.8%, underpinning effective profit generation relative to equity levels invested in the business [F1]. Free cash flow supports financial flexibility for both organic growth investments and shareholder distributions.

Operational Risk Management

Cybersecurity is prominently managed under the Board’s Audit Committee supervision which conducts extensive oversight across cybersecurity strategy risk assessments incident tracking and mitigation activities tailored to retail-specific threats such as ransomware attacks prevalent industry-wide [S1,S9]. Quarterly reports and metrics help maintain vigilance while the committee receives ongoing education addressing emerging cyber risk trends including AI governance considerations.

Other risks include intensifying competitive dynamics within discount retail that necessitate continued innovation in pricing strategies and nimble merchandising decisions.

Leadership Transition Highlights

The elevation of Emily C. Taylor to Chief Operating Officer in November 2025 reflects internal succession planning reinforcing operational continuity given her long tenure spanning merchandising operations through channel innovation roles since joining Dollar General in 1998 [S24]. This move aligns incentives via enhanced compensation tied partly to company performance metrics.

Market Reaction Context

Despite Dollar General’s Q4 earnings beat reported on March 12 the stock experienced muted upward movement influenced by broader macroeconomic concerns such as rising oil prices and credit market volatility which affect consumer discretionary spending sentiments [N2,N11,N12,N13]. The mixed market response underscores external factors sometimes overshadowing fundamental strength.

Analysis: Strategic Positioning Amid Retail Dynamics

Dollar General's extensive footprint across economically sensitive rural areas affords it entry barriers difficult for large-format competitors who concentrate urban centers — a strategic moat enabling resilience during variable consumer confidence cycles. Moreover leveraging high-turn inventory models common among dollar stores aligns well with lean supply chain tactics enhancing margins when carefully balanced against inflationary pressures.

However sustaining momentum demands constant vigilance on pricing elasticity given shelf space constraints versus broader retailers with omnichannel capabilities better suited for evolving digital consumption habits.

Conclusion

Dollar General emerges from fiscal year 2025 with reinforced profitability driven by focused execution within its value-based retail model supported by proactive risk oversight structures notably around cybersecurity matters that could materially impact financials if inadequately managed. Future horizons depend on steady expansion into underserved geographies while optimizing operational efficiencies amid uncertain macroeconomic backdrops influencing consumer spending patterns. Monitoring quarterly sales trends along with margin fluctuations remains vital to validate continued success beyond headline earnings reports as the company balances growth ambitions with prudent capital returns policies favoring dividends plus share repurchases.

Disclaimer: This analysis is based solely on publicly available information cited herein as of March 20, 2026 without any forecasting or investment advice intended.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments