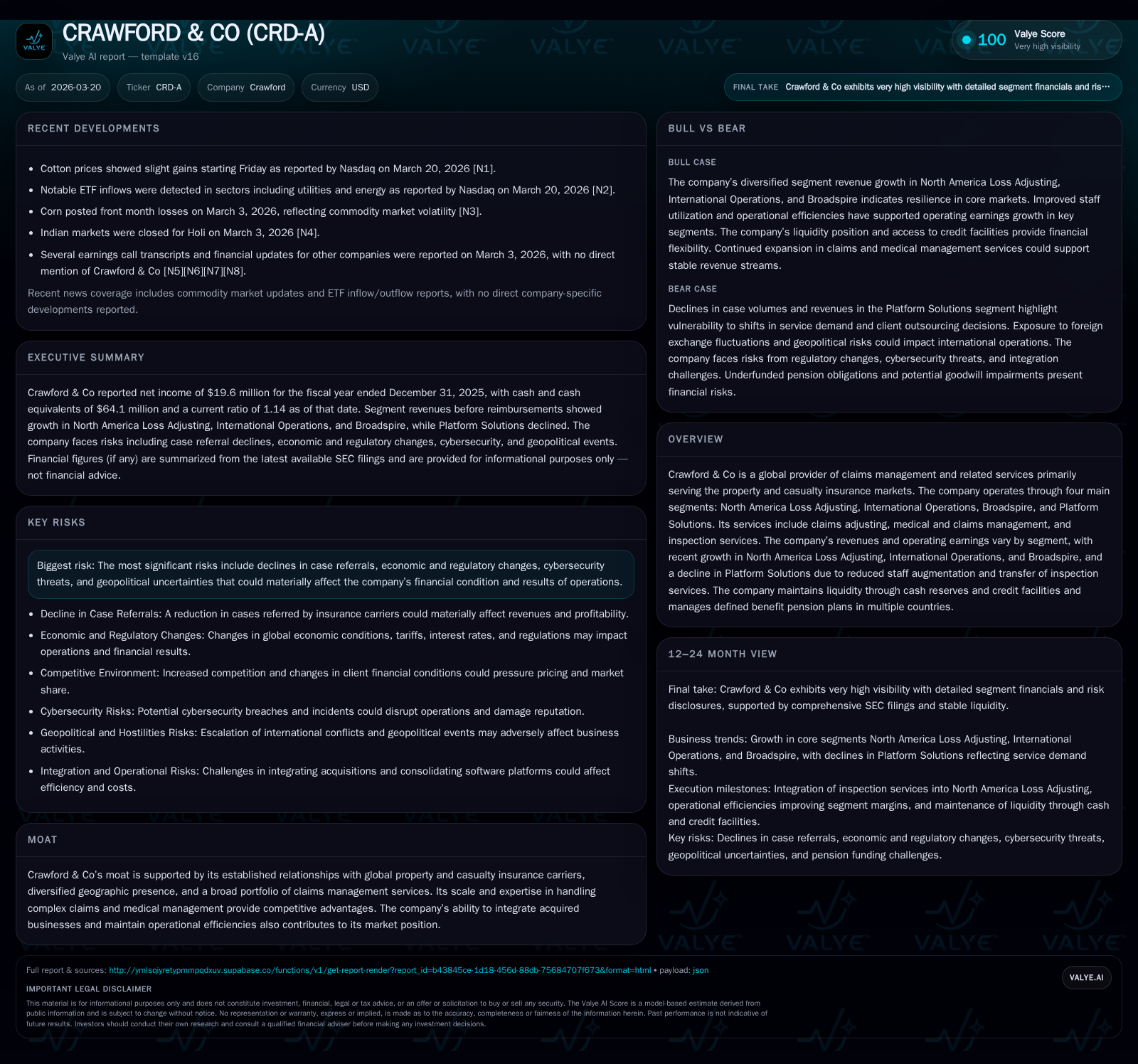

Crawford & Co's Shifting Segment Dynamics and Capital Strategy in 2025

Analyzing how Crawford & Co’s variable segment performance shapes its earnings outlook and capital deployment decisions.

Crawford & Co experienced a top-line contraction of approximately 3.5% in 2025, driven by divergent segment trajectories: growth in North America Loss Adjusting, International Operations, and Broadspire contrasted with declines in Platform Solutions. Despite net income declining by over 26%, operating cash flow nearly doubled year-over-year, reflecting strong cash collection and operational discipline. The company maintains a robust $500 million revolving credit facility supporting liquidity, while balancing shareholder returns with funding defined benefit pension obligations. Going forward, case referral volume variability and regulatory changes remain critical risks to monitor.

Historical Revenue and Profit Trends: Segment Contributions Over Time

Crawford & Co’s consolidated revenue for fiscal year 2025 was approximately $1.12 billion, reflecting a decline of roughly 3.5% compared with the prior year ($1.16 billion in 2024) [F1]. This decline aligns with the reported downturn principally attributable to the Platform Solutions segment’s reduced business activity.

Net income fell similarly by over 26%, from $26.6 million in 2024 to around $19.6 million in 2025 [F1], pressured by margin compression in select segments despite steady revenues elsewhere. Operating cash flow significantly outperformed net income trends—nearly doubling from $51.6 million to about $101.8 million—signaling improved working capital management and cash collections [F1]. Capital expenditures remained moderate at $7 million, a slight increase from the prior year [F1]. The combination of solid cash generation and cautious capex underscores disciplined operational execution.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 20 | 102 | 7 | -26.2% |

| 2024 | 27 | 52 | 6 | -13.1% |

| 2023 | 31 | 104 | 5 | +267.2% |

| 2022 | -18 | 28 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 14 | 11 | 95 |

| 2024 | 14 | 4 | 45 |

| 2023 | 13 | 3 | 99 |

| 2022 | 12 | 27 | 21 |

Source: SEC companyfacts cache [F1].

Revenue decline reflects reported segment disparities; net income erosion juxtaposes cash flow strength.

Segment-Level Growth Drivers and Challenges Evident in 2025 Results

The company operates four primary segments with distinct performance patterns through 2025 :

North America Loss Adjusting: Revenues grew modestly on an organic basis with an uptick in low-value inspection service cases partially offsetting declines in high-frequency claims linked to fewer significant weather events in the U.S. The transfer of inspection services from Platform Solutions contributed approximately $3.7 million year-to-date [S10]. Operating earnings expanded around mid-teens percent year-over-year on improved unit economics [S13].

International Operations: Revenues increased about 6-7%, benefiting from favorable foreign currency movements (+3.3%) and business expansion across regions except Latin America where case volume decreased approximately 25%. Operating earnings rose meaningfully (~48%) driven by higher pricing and efficiency gains primarily in the U.K., Asia, and Australia [S9,S16]. However, overall international case volumes declined roughly 9-10%, indicating mix improvements rather than volume-driven growth [S19].

Broadspire: Claims management and medical management services grew steadily with revenue increases near 3-4%, supported by new disability clients and price adjustments leading to enhanced gross margins [S14,S15]. Case volumes advanced slightly (~1-1.4%), underpinning segmented expansion.

Platform Solutions: Contrasting other segments, this area saw decreased staff augmentation services and transfer of inspection work reducing its revenue base despite margin improvement driven by cost control measures [S22]. Operating earnings experienced some quarterly pressure but stabilized over the nine-month period.

This uneven revenue profile reflects higher-margin segments offsetting client behavior shifts and service line transfers impacting lower-margin activities.

Business Model Nuances: Claims Adjusting and Medical Management Expertise

Crawford & Co leverages scale across diverse global jurisdictions with established relationships within property & casualty insurance markets—a durable competitive advantage rooted in complex claims handling capabilities [S8,S9].

Expertise spans loss adjusting—assessing claim validity—and medical claims administration involving detailed management of injury or illness compensation claims. This technical sophistication combined with multi-jurisdictional integration allows operational leverage supporting margins amid external pressures such as fluctuating case referrals or regulatory changes.

The company's ability to integrate acquisitions and streamline operations further strengthens barriers against fragmented smaller competitors lacking broad geographic reach or specialized medical management resources.

Capital Structure, Liquidity, and Credit Facility Overview

Crawford maintains a revolving credit facility totaling $500 million maturing December 2030 with geographic sublimits ($250M U.K., $125M Canada, $75M Australia), facilitating regional borrowing flexibility [S4].

Guarantees cover domestic subsidiaries plus key foreign disregarded entities securing borrowings via first-priority liens on personal property assets [S4]. Financial covenants include a maximum consolidated leverage ratio capped at approximately 4.50x EBITDA and minimum interest coverage ratio above roughly 2.50x EBITDA-to-interest expense ensuring prudent leverage metrics are maintained quarterly [S20].

As of late-2025 reporting periods, total debt including finance leases remained stable near $218 million while liquidity—combining unrestricted cash ($64 million) plus borrowing availability—was approximately $298 million [F1,S5,S17], providing ample buffer amid seasonal working capital fluctuations such as annual incentive payments.

Comprehensive Review of Capital Allocation: Dividends and Share Repurchases

Shareholder returns continued alongside operational reinvestment:

- Dividends paid increased modestly year-over-year to about $14.3 million in FY25 from $13.7 million prior year reflecting board confidence given sustainable cash flows [F1,S29].

- Share repurchases more than doubled reaching over $10.5 million executed during FY25 versus roughly $3.9 million previously reflecting opportunistic buybacks amid share price considerations.

These distributions balance against ongoing underfunded defined benefit pension obligations—the U.S. plan remains frozen but underfunded by approximately $19 million as of end-2024 while U.K plans hold a modest surplus [$9.2M], encouraging measured discretionary contributions [S5]. Pension funding rules vary internationally requiring cautious capital planning given evolving regulations.

Future Outlook: Risks from Case Volume Variability and Regulatory Environment

Management highlights key risk factors centering on insurance case referral declines which directly impact core revenues due to industry reliance on outsourced claims processing [S2,S18]:

- Fluctuations may arise from changing insurer outsourcing preferences or macroeconomic cycles affecting underwriting activity.

- Regulatory changes impacting pension plan funding could increase capital demands altering free cash flow availability.

- Cybersecurity threats pose growing operational risks within claims administration systems.

- Geopolitical tensions or localized economic downturns affect international exposure.

Contract renewals depend on demonstrated cost efficiencies; failure could constrain growth prospects.

Key Metrics to Watch: Operating Cash Flow, Pension Funding Status, and Earnings Resilience

Stakeholders should focus on:

- Operating Cash Flow: With CFO nearly doubling despite net income contraction ($101.8M vs $51.6M), cash conversion efficiency remains a critical indicator of business health beyond earnings volatility [F1].

- Pension Plan Funding: Levels of under/overfunding globally influence future contribution requirements affecting discretionary spending capacity especially dividends or buybacks [S5].

- Segment Unit Volumes: Case counts closely correlate with revenue generation particularly within Loss Adjusting and Broadspire segments; ongoing monitoring guides growth expectations [S19,S25].

- Capital Expenditures: Moderate increase signals balanced investment towards technology upgrades or process automation enhancing long-term competitiveness without compromising free cash flow generation.

This multidimensional framework offers a comprehensive lens into operational execution amid market challenges for informed stakeholder evaluation.

This report synthesizes available financial data as of Q4 2025 filing dates alongside company disclosures without providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments