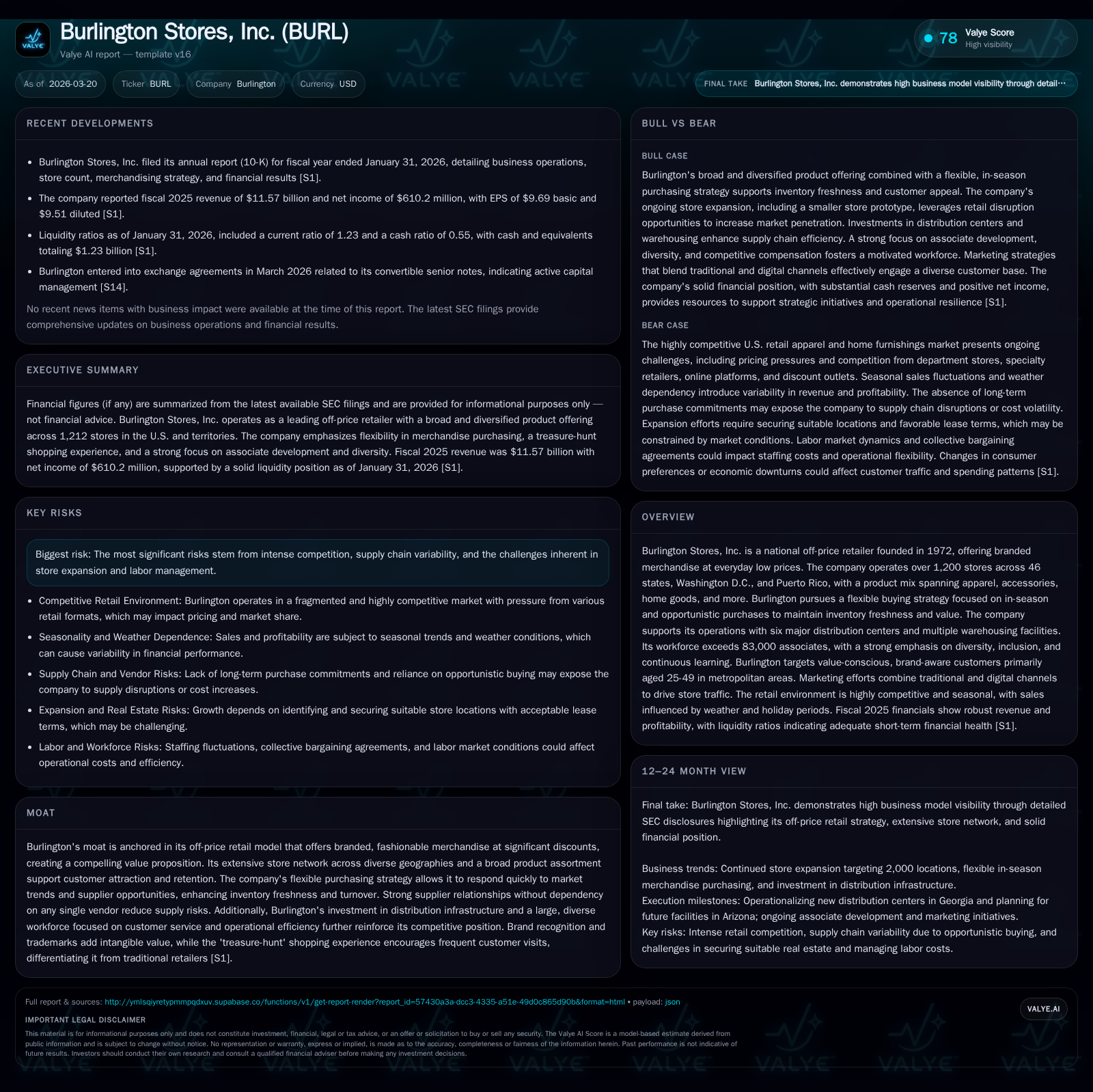

Burlington Stores' Resilient Expansion and Earnings Surge in Fiscal 2025

Burlington’s flexible off-price model and strategic execution fueled notable gains in revenue, net income, and infrastructure expansion during fiscal year 2025.

Burlington Stores, Inc. delivered robust financial performance in fiscal 2025, driven by an 8.8% increase in revenue to $11.57 billion and a 21.1% surge in net income to $610 million [F1]. The company’s merchant agility, anchored in majority in-season buying and a comprehensive scorecard approach, underpinned inventory freshness and customer appeal [S9]. Store expansion continued with 113 new openings, surpassing closings and pushing the store base past 1,200 locations nationwide [F1][S7]. Capital allocation reflects disciplined growth investments with $1.06 billion in CapEx and $278 million in share repurchases [F1], supporting long-term ambitions while maintaining a strong operating cash flow margin. Risks such as labor management and supply chain variability remain near-term focal points [S5].

Historical Growth Trajectory and Key Drivers Through Fiscal 2025

Burlington Stores demonstrated pronounced top-line and profitability growth over the past several fiscal years culminating in fiscal year 2025 with revenues climbing to $11.57 billion, an increase of approximately 8.8% from $10.63 billion in fiscal 2024 [F1]. Net income exhibited an even stronger acceleration rising by more than one fifth (+21.1%) to reach $610 million compared to the prior year’s $504 million [F1]. This outperformance reflects effective leverage of the company’s off-price model alongside operational efficiencies.

Operating cash flow exhibited robust growth as well at $1.23 billion in fiscal 2025 versus $863 million the prior year (+42.6%), comfortably supporting capital expenditure expansion which rose by approximately one-fifth to over $1 billion allocated primarily for capacity enhancements [F1].

Store expansion has been a consistent driver underpinning these financial outcomes. The store count grew from about 1,007 units three years ago to 1,212 stores as of January 31, 2026 — covering an expansive footprint across 46 states plus Washington D.C., and Puerto Rico — with new store openings outpacing closures by more than tenfold last fiscal year [F1][S7]. This geographic diversification helps mitigate regional risk while tapping varied consumer segments.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 11.6 | 610 | 1231 | 1060 | +8.8% | +21.1% |

| 2024 | 10.6 | 504 | 863 | 880 | +9.3% | +48.3% |

| 2023 | 9.7 | 340 | 869 | 493 | +11.8% | +47.6% |

| 2022 | 8.7 | 230 | 596 | 447 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 278 | 172 | 33.8 |

| 2024 | 256 | -17 | 36.7 |

| 2023 | 243 | 376 | 34.1 |

| 2022 | 317 | 149 | 28.9 |

Source: SEC companyfacts cache [F1].

Financial metrics reflect fiscal years ending late January/early February annually per company reporting [F1]

Merchandising Agility: The Flexibility Behind Fresh, Branded Inventory

Central to Burlington’s success is its nimble merchandising model aligned tightly with the off-price sector dynamics that prize inventory freshness and deep discounts on branded items [S9]. A majority of merchandise is purchased in-season allowing responsiveness to shifting fashion trends rather than being locked into pre-season buys that can result in aging stock.

The company deploys a merchant scorecard framework evaluating incoming goods on four key attributes — fashion relevance, product quality, brand strength, and price competitiveness — ensuring each purchase aligns well with the value proposition offered customers [S9]. Buyer-planner roles are distinctly defined; buyers actively source products week by week engaging suppliers face-to-face while planners analyze data to optimize assortment mix.

This approach sustains high inventory turnover while preserving the "treasure-hunt" experience driving repeat visits among customers hunting for unexpected branded bargains up to approximately sixty percent below full-price retailers’ tags across broad categories from apparel through home goods [S9][S1].

Store Network Expansion and Distribution Infrastructure Enhancements

Burlington accelerated store growth with net openings exceeding one hundred stores during fiscal year 2025 alone (113 opened vs only nine closed), resulting in a total of over 1,200 locations nationwide at fiscal year end — a milestone reflecting ongoing confidence in organic unit growth amidst retail industry disruption favoring off-price channels [S7][F1].

Supporting this vast network is an evolving distribution infrastructure comprising six primary distribution centers strategically located along East and West coasts complemented by multiple warehousing facilities totaling millions of square feet [S7][S12]. Notably, progress on a recently acquired Georgia distribution center leased-exercised during fiscal year 2024 is set for full operational status by fiscal year end or early FY26 providing vital throughput capacity for Southeast operations.

In addition, substantial land acquisition for a future center near Buckeye, Arizona signals longer-term logistical foresight aimed at strengthening omniregional replenishment capabilities coinciding with store density increases further westward scheduled for fiscal year ending FY28 deployment likely [S7]. These expansions coincide with increased capex of over $1 billion (+20% YoY) mainly directed toward such capacity projects enhancing supply chain flexibility — a critical asset underpinned Burlington’s scale advantages within off-price dynamics where logistics agility supports rapid inventory turns needed for sustained freshness of assortments.

Analyzing Recent Earnings Beat and Comparable Store Sales Momentum

Recent quarterly earning reports through Q4/FY25 revealed positive operational momentum reflective of strong comparable sales gains contributing materially to top-line surprises relative to market expectations noted across multiple sources cited on March earnings announcements [N1][N3][N4][N6].

Specifically, Burlington reported comparable store sales growth year-over-year suggesting resilient consumer appetite despite macroeconomic uncertainties—a corroborative signal of the effective implementation of the flexible buying strategy alongside enhanced shopper propositions amidst competitive pressures typical of off-price retailing environments.

The market rewarded this performance evidenced by share price appreciations following announcement releases reinforcing investor perception around sustainable execution prowess though explicit forward guidance remains relatively broad but confirms focus on "flexibility initiatives" slated for continuation into FY26 emphasizing responsiveness enhancements referenced by management commentary [N6][S1].

Strategic Capital Allocation: Balancing Growth Investments and Shareholder Returns

Capital deployment reveals Burlington’s balancing act between aggressive store network expansion funded via operating free cash flows generated alongside prudent equity reinvestment policies rather than levering external capital disproportionately at this juncture.

With an approximate Return on Equity north of approximately thirty-four percent (~34%) computed from net income over equity base as of FY25 end [$610M / $1.81B]—a notable efficiency indicator within retail—the company maintains disciplined financial stewardship supporting both organic growth projects (e.g., new stores, logistics hubs) as well as shareholder returns primarily through steady share repurchases approximating $278 million annualized during FY25 compared to prior years’ buyback levels [$256-$316M range] without currently paying dividends as capital is prioritized toward reinvestment phases reflecting growth orientation combined with maintaining liquidity buffers near $1.23 billion cash & equivalents as recorded at fiscal close[F1][S16][S24].

Operational Metrics: Turnover, Working Capital, and Inventory Freshness

Burlington closely monitors key operational parameters optimized via its merchant organization design where buyers drive purchasing volume/freshness while planners refine forecasting/inventory turns balancing working capital efficiency against meeting rapid consumer demand cycles.

As per latest reporting lines from SEC filings citing current ratio stands at a healthy ~1.23 reflecting solid short-term liquidity positioning balancing payables against receivables/inventory stock levels ensuring adequate flexibility amid seasonally variable retail conditions [F1].[S9]

High inventory turnover rates correlate directly with the "treasure-hunt" value proposition intangible moat by incentivizing frequent customer visits seeking new deals constantly replenished across categories enabling reduced markdown risks typically constraining traditional off-price competitors less focused on turnover velocity all while maintaining supplier relationships diversified enough not to depend heavily on any single vendor curbing supply concentration risks despite significant volume purchasing power leveraged via flexible contract terms without long-term purchase commitments granted through agile sourcing strategies.[S9]

Competitive Positioning within the Off-Price Retail Sector

Within the fragmented U.S. apparel and home furnishings markets characterized by fierce price competition spanning department stores’ off-price arms through specialty discounters Burlington distinguishes itself through scale coupled with breadth spanning women’s apparel (20%), accessories/shoes (28%), home decor (20%), menswear (17%) and children/baby segments constituting multi-category diversification suited for cross-selling synergies attracting value-conscious yet brand-aware shoppers predominately aged mid-twenties to late forties residing mainly metropolitan catchments emphasizing convenience along with variety-driven impulse formats[S6][S9].

Its ability to offer up to sixty percent discounts off other retailers' prices combined with frequent merchandise refreshes sustained through disciplined merchandising scorecards ensures strong differentiation versus pure discounters or department store clearance outlets often hampered by dated product cycles or narrower assortments.

Marketing dynamically blends broadcast media reach complemented increasingly by digital/streaming platforms fostering authentic community engagement through social channels including influencer tie-ins combining broad awareness creation alongside localized targeted messaging effectively addressing its core demographics optimally leveraging evolving media consumption patterns.[S6]

Industry risks persist notably labor market cost pressures complicated by regulatory wage claims impacting margins while supply chain fluctuations pose episodic challenges; nonetheless Burlington's lack of reliance on any singular vendor insulates against acute disruptions seen elsewhere[S5][S13], outlining durable competitive moats rooted in operational effectiveness plus cultural emphasis on associate retention/development across its large workforce exceeding eighty-three thousand associates highlighting human capital importance[S8][S18].

Future Outlook: Growth Constraints and Strategic Opportunities to Monitor

Looking ahead opportunities hinge largely upon continued execution in expanding store footprint targeting eventually reaching around two thousand units anchored partially on deploying smaller-format store prototypes amidst accelerating closures/disruptions elsewhere creating favorable real estate availability [S7]. Coupled with planned commissioning of expanded logistics centers notably Ellabell Georgia facility operationalizing soon plus pending Arizona site development ensure material backend support.[S7]

Key headwinds center around labor availability/cost inflation potentially squeezing margins alongside intense retail competition necessitating constant merchandising innovation plus balancing inventory freshness without overstocking creating working capital tensions.[S5]

Management emphasizes ongoing "flexibility" initiatives encompassing buyer-planner coordination enhancements plus technological investments designed for data-driven rapid adjustments aligning inventory precisely with volatile customer demand patterns skeptical economic assumptions notwithstanding.[N6]

Absent explicit multi-year formal guidance issued recently investors should watch upcoming quarterly comparable sales results plus capex deployment pace alongside any margin trend disclosures reflecting ability to sustain profitability under evolving macro constraints.

This analysis synthesizes publicly filed SEC documents alongside recent market commentary without incorporating speculative forecasts or investment advice but aims principally at providing informed domain insights respecting validated company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments