Intellicheck's Return to Profitability Driven by AI-Focused Product Expansion and Client Concentration

After years of losses, Intellicheck posted positive net income in 2025 amidst ongoing investments in AI and identity validation enhancements.

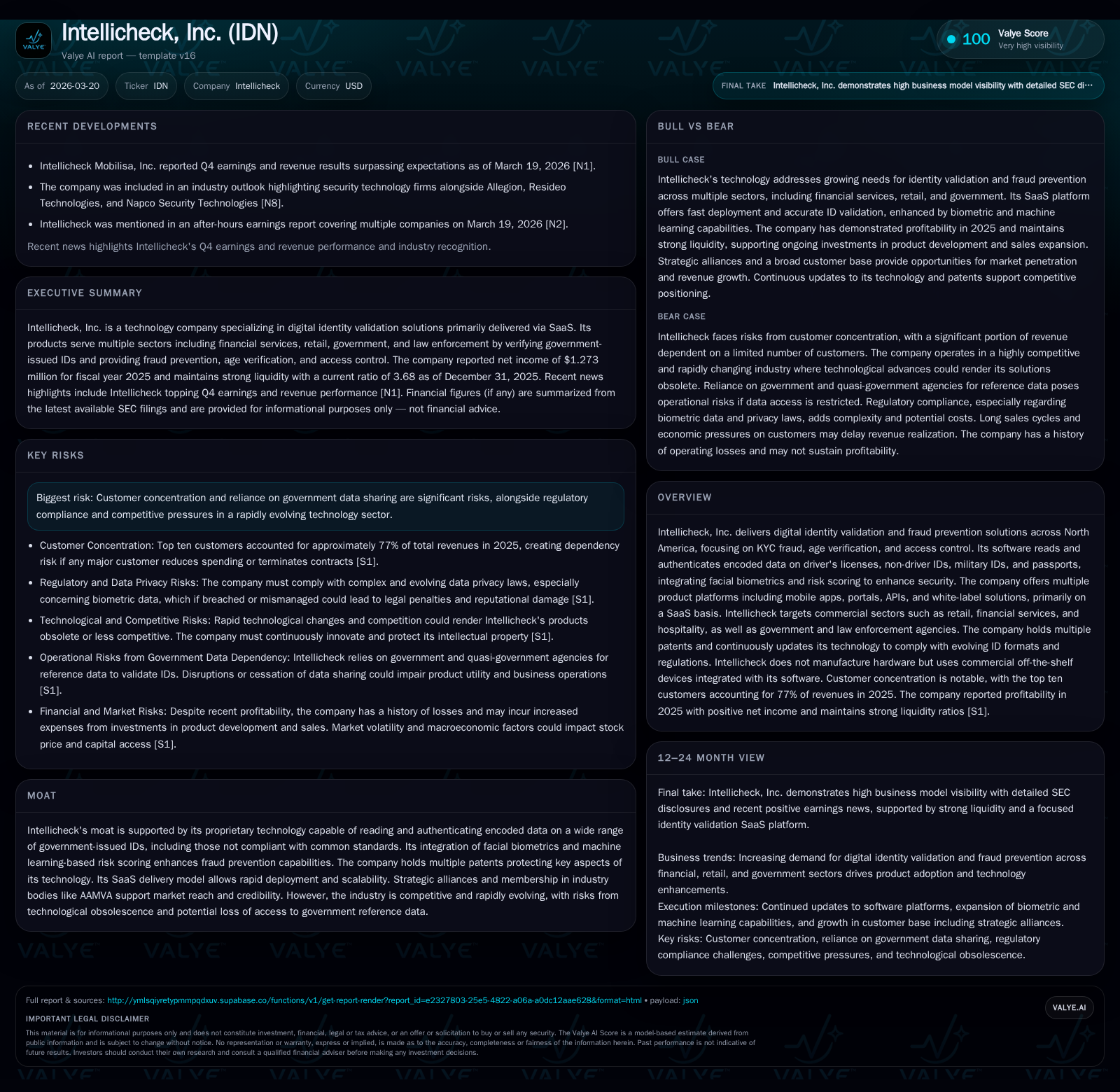

Intellicheck, Inc. achieved profitability in fiscal 2025, reporting a net income of $1.27 million following several years of losses, supported by growing revenues and stronger operating margins. The company's proprietary SaaS identity validation platform integrates barcode reading from IDs, facial biometrics, and machine learning risk scoring, primarily serving retail, financial services, and government sectors across North America. Despite the turnaround, its business remains exposed to customer concentration risks and reliance on government data sharing. Future growth hinges on expanding market share in commercial fraud prevention and innovation in AI-driven authentication technologies while managing operational scale and regulatory compliance.

Company Overview

Intellicheck, Inc., founded originally as Intelli-Check in 1994 and now headquartered in Melville, New York, operates as a technology company specializing in digital identity validation and fraud prevention solutions across North America [S1][S11]. The company's core offering leverages proprietary software capable of reading encoded formats on a broad spectrum of government-issued identification documents—including driver’s licenses, non-driver IDs, military IDs, and passports—many of which do not comply with common data standards [S11][S17]. Intellicheck enhances security assurance by integrating facial biometric matching via selfie comparison with ID photos and applying machine learning-based risk scoring using diverse data signals such as device fingerprinting and geographic information [S11][S17].

The company’s products are delivered predominantly as Software-as-a-Service (SaaS), available through mobile apps (IDN-Mobile), web portals (IDN-Portal), API integrations (IDN-Direct), and custom white-label solutions (IDN-Capture) [S11][S12][S18]. Hardware devices required for data capture are commercially off-the-shelf scanners or smartphones with barcode or magnetic stripe readers; Intellicheck does not manufacture any hardware itself [S23].

Target industries for Intellicheck’s solutions include retail commerce (mass merchandisers, convenience stores), financial services (banks, credit unions), hospitality (casinos, hotels), law enforcement agencies (FBI, ATF), transportation (airlines), and government institutions [S8][S15][S18]. Use cases span age-restricted product verification (alcohol, cannabis), instant credit approval kiosks at retail points-of-sale (POS), commercial fraud prevention including check cashing frauds, access control for secure facilities, and e-commerce transaction validation [S11][S18][S20].

Historical Performance

Financial performance has shown notable volatility over recent years. While revenues were recorded at approximately $1.53 million in FY2015 followed by declines to $734k in FY2016 before recovering to about $1.33 million by FY2018 [F1], detailed revenue figures after 2018 are not explicitly reported in the available disclosures.

Profitability was elusive until recently:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1 | 5 | 1 | 52000 | +238.7% |

| 2024 | -1 | -3 | -1 | 57000 | +53.6% |

| 2023 | -2 | -1 | -2 | 93000 | +48.6% |

| 2022 | -4 | -3 | -4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 4 | 6.2 |

| 2024 | -3 | -5.2 |

| 2023 | -1 | -11.5 |

| 2022 | -20.8 |

Source: SEC companyfacts cache [F1].

Intellicheck achieved positive operating income of approximately $1.09 million in FY2025 after running losses ranging from about $370k to over $3.7 million between FY2022-FY2024 [F1]. Its net income swung to a profit of $1.27 million after posting losses for four consecutive years [F1]. Operating cash flow similarly transformed dramatically from negative millions during previous years to $4.54 million positive cash inflow last year [F1]. Capital expenditures remained relatively low throughout this period (<$100k annually) reflecting the company's software-centric business model [F1].

The firm’s equity base expanded from around $17 million to over $20.7 million between FY2023-25 indicating modest retained earnings accumulation after years of deficits exceeding $133 million cumulatively [F1][S1]. The balance sheet remains liquid with cash & equivalents approximating $9.65 million alongside a current ratio near 3.7 at year-end FY2025 [F1].

Growth Drivers & Future Prospects

Intellicheck’s near-term growth strategy revolves around several key initiatives:

AI-enhanced fraud detection: The company is investing heavily to integrate advanced artificial intelligence technologies that improve risk scoring accuracy against increasingly sophisticated fraud schemes including synthetic IDs and deepfakes [S21].

Market Expansion: Efforts focus on increasing market share within existing commercial verticals such as retail instant credit issuance and age verification while also pursuing additional government agency contracts leveraging their patented technology portfolio [S11][S18][S38].

Product Diversification: Extensions into online identity validations respond to the growing need for fraud prevention across billions of internet transactions daily; enhanced facial recognition features also aim to maintain a leading edge amid rapid technological evolution [S11][S27].

Strategic Partnerships: Membership on advisory boards like AAMVA allows Intellicheck to influence industry standards and maintain privileged access to government reference ID data critical for product effectiveness which is a moat element protected by patents [S18].

However, growth is not assured: considerable customer concentration risk persists with the top ten clients comprising about three-fourths of revenue which may expose the company to significant volatility if any major customer contracts diminish or are lost [S19]. Sales cycles remain prolonged particularly within large retail chains or government procurement processes impacting revenue timing [S19]. Regulatory compliance costs escalate alongside privacy laws targeting biometric data usage posing future expense burdens as well as reputational challenges highlighted by an ongoing biometric privacy class action complaint under Illinois BIPA cases starting early 2026 that Intellicheck intends to contest vigorously without currently accruing loss contingencies [S22]. Cybersecurity dependence on external cloud providers also presents risks around service disruptions or breaches that could materially impact service availability or lead to liabilities despite board-level oversight attention [S25].

Outlook & Milestones To Watch

Official forward guidance is not explicitly provided; however notable upcoming points include:

- Monitoring quarterly earnings releases post Q4/25 will be important for signs that operating profitability can be sustained against expanding R&D investments particularly focused on AI capabilities.

- Customer diversification progress metrics including contract wins or renewals among large retail chains or government sectors will reflect success executing sales strategy.

- Regulatory developments regarding biometric privacy laws that might impact the operational model or introduce new compliance costs.

- Technological adaptation relating to mobile OS ecosystem changes or emerging competing digital identity platforms built into iOS/Android wallets which could challenge Intellicheck's middleware positioning.

- Innovations or patent grants extending competitive moats.

Capital Allocation & Returns

With no dividends paid historically or anticipated in the foreseeable future per management statements reflecting reinvestment focus [S6], shareholder returns are predicated solely on stock price appreciation.

The firm's return on equity approximates a modest ~6% in FY2025 based on net income relative to shareholders’ equity indicating early-stage profitability recovery but room for improvement given technology sector norms [F1].

Free cash flow remained robust last year estimated near $4.49 million after deducting modest capex from operating cash flow illustrating strong cash generation supporting operating expansion without immediate capital raises though the company maintains a shelf registration allowing issuance if necessary [S6][F1].

Past minor repurchases occurred circa FY2016-17 but no recent buyback activity exists reflecting focus on growth reinvestment rather than capital returns to shareholders presently [F1].

Risks Summary

Key risks include:

- Heavy reliance on governmental reference data sharing programs; cessation would erode software efficacy regionally causing material harm.

- Customer concentration risk with dependency weighted towards few large accounts impacts revenue stability.

- Technological obsolescence risk amid accelerating innovations including generative AI-enabled synthetic identities requiring continual investments.

- Privacy regulatory environment tightening particularly around biometric data collection/storage potentially increasing compliance costs or legal exposure.

- Long sales cycles especially with larger customers introducing revenue recognition timing uncertainty.

- Cybersecurity vulnerability heightened by reliance on third-party cloud infrastructure exposing company to potential breaches inheriting legal liabilities.

- Potential intellectual property disputes could arise given competitive industry dynamics despite currently holding multiple patents protecting core technologies.

Conclusion

Intellicheck stands at a cautious inflection point having reversed multi-year losses into profitability through improved operational execution bolstered by its differentiated technology integrating patented barcode ID parsing with biometrics and AI-driven risk scoring. Its SaaS delivery model supporting rapid customer deployments aligns well with emerging demands for real-time identity verification broadly across commerce and government sectors.

Yet navigating ongoing industry challenges such as maintaining access to government datasets critical for its product accuracy coupled with managing concentrated buyer relationships while innovating ahead of disruptive advances like embedded mobile wallet IDs will dictate long-term growth trajectories.

Close monitoring of incremental financial performance indicators alongside R&D investment outcomes related to AI capabilities combined with mitigation strategies around regulatory/privacy compliance will be essential signals ahead for the firm’s sustainability as a competitive identity validation provider.

This report is intended solely for informational purposes based on publicly available data as of March 20, 2026, without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments