Nobility Homes Inc Builds Stability with Vertical Integration and Strong Balance Sheet

Nobility Homes leverages its vertically integrated business model and conservative capital management to sustain operational stability and modest growth in Florida's manufactured housing market.

With over 58 years in Florida's affordable housing sector, Nobility Homes maintains a resilient operational footprint rooted in manufacturing, retail sales, and insurance services. The company reports modest revenue growth and improved operating margins supported by inventory ownership that avoids floor plan financing costs. Despite macroeconomic pressures including inflation, supply chain disruptions, and rising interest rates, Nobility’s strong liquidity position and zero-debt balance sheet underpin its financial flexibility. Future growth hinges on navigating market demand variability, maintaining efficient cash flow generation, and managing cost inflation headwinds across materials and labor.

Legacy of Steady Growth: Financial Performance and Key Historical Drivers

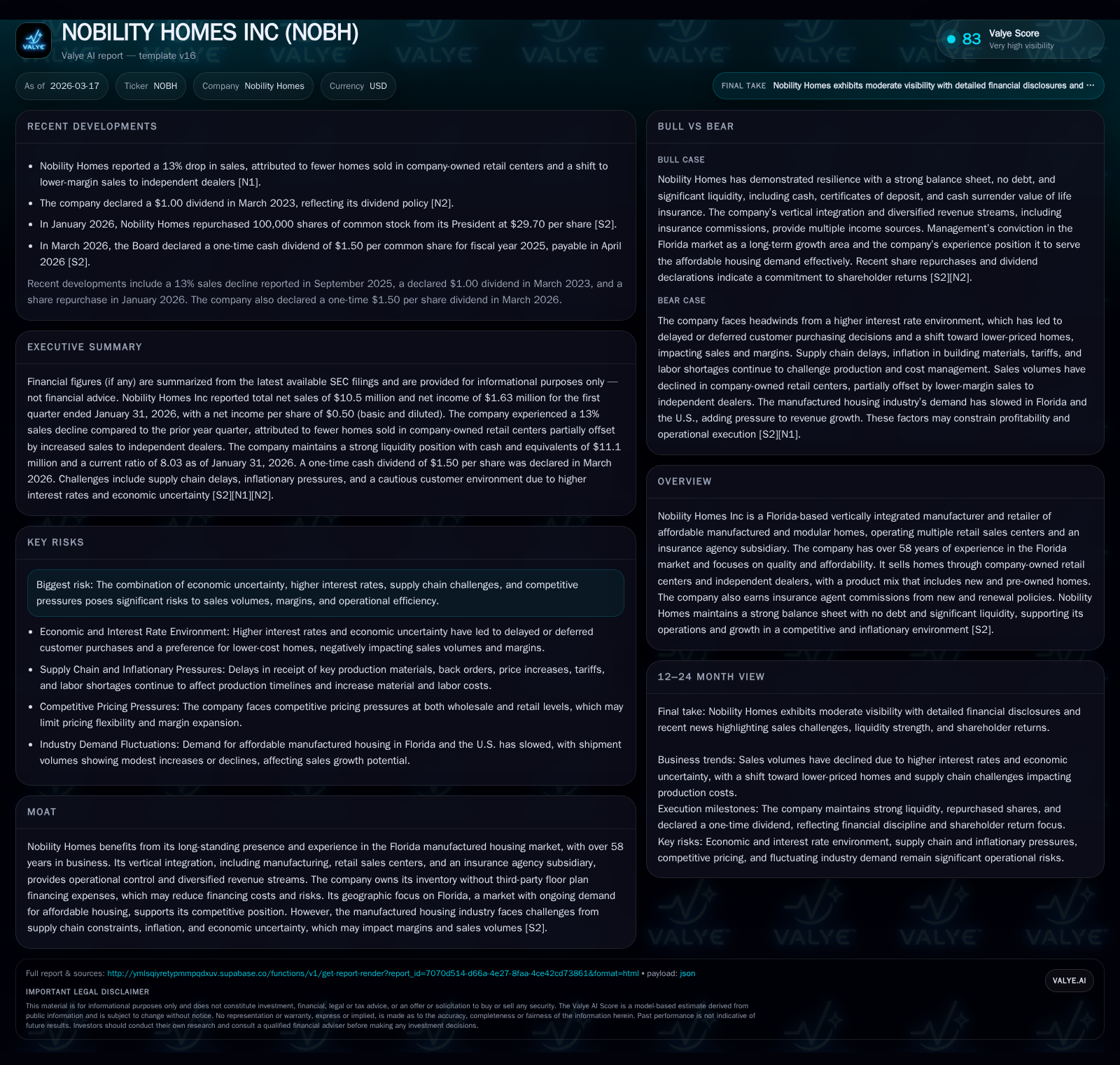

Nobility Homes has showcased a pattern of steady operational results over recent fiscal years anchored by its established position within Florida's affordable manufactured housing sphere. Fiscal Year (FY) 2025 top-line revenue reached approximately $52.7 million representing a modest increase of around 1.4% compared to FY2024's $51.9 million [F1]. Operating income expanded by 4.7% to over $10 million during the same period reflecting efficiency gains despite inflationary cost pressures. However, net income showed a mild contraction of roughly 1.9%, declining from about $8.6 million in FY2024 to $8.4 million in FY2025 [F1].

Operating cash flow exhibited a sharper decrease with a near-41% drop year-over-year from approximately $7 million in FY2024 to just above $4 million in FY2025. This decline stemmed largely from working capital fluctuations characteristic of inventory management cycles amid supply constraints and customer deposit changes documented by management [F1], [S11]. Capital expenditures remained minimal around $180 thousand annually supporting plant and equipment maintenance rather than expansion reflective of measured asset reinvestment priorities.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 53 | 8 | 4 | 10 | +1.4% | -1.9% |

| 2024 | 52 | 9 | 7 | 10 | -18.0% | -21.0% |

| 2023 | 63 | 11 | 10 | 13 | +22.9% | +50.7% |

| 2022 | 52 | 7 | -8 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 4 | 0 | 4 |

| 2024 | 5 | 0 | 7 |

| 2023 | 3 | 3 | 10 |

| 2022 | 4 | 5 | -9 |

Source: SEC companyfacts cache [F1].

This consistent topline expansion paired with historically stable operating margins has been driven by Nobility’s strategic focus on the Florida market where demand for affordable housing remains persistent. The company's unique offering includes new factory-built homes alongside pre-owned models sold through its own retail outlets as well as independent dealer channels.

Vertical Integration as a Strategic Moat in Manufactured Housing

Nobility Homes’ vertically integrated business model forms the cornerstone of its operational stability and competitive edge. Ownership spans the entire value chain: from manufacturing homes at company plants to distribution via multiple retail sales centers scattered across Florida; complemented by an insurance agency subsidiary earning commissions on both new and renewal policies [S2].

This operational structure yields several sector-specific advantages notably the elimination of third-party floor plan financing commonly utilized by competitors to fund substantial inventory holdings through external creditors or lenders. By owning its inventory outright—valued near $20 million including finished homes—the company sidesteps typical financing expense burdens that can erode margins during inflationary cycles or credit tightening phases [S9], [S11].

Moreover, the insurance arm diversifies revenue streams away from pure home sales volatility; commission income has been gradually increasing with premiums related to newly written policies providing more predictable cash inflows even amid fluctuating housing demand dynamics [S23]. Such diversification shields earnings from cyclical swings inherent in the manufactured housing industry.

Current Operating Environment: Market Dynamics and Emerging Constraints

Despite localized demand strength within Florida—a state characterized by ongoing population growth—Nobility contends with mounting headwinds broadly confronting manufactured homemakers nationwide.

Material supply challenges remain acute; key inputs including forest products integral to framing lumber; vinyl siding; and PVC piping suffer price inflation coupled with intermittent delivery delays attributed primarily to supply chain bottlenecks reported alongside labor shortages raising production costs sharply [S4], [S10]. These factors directly affect completion schedules at Nobility’s manufacturing facility delaying some customer deliveries.

Simultaneously macroeconomic considerations intensify purchasing hesitancy among potential buyers; higher mortgage interest rates have notably slowed sale volumes within company-owned retail centers—from selling 67 new homes in comparable Q1 last year down to just 43—with dealers absorbing increased volumes via wholesale transactions albeit at narrower margins [S20], [S23]. Homebuyers are reportedly opting for more economically priced models reflecting broader affordability concerns tied to elevated borrowing costs.

Consumer confidence remains fragile under these conditions contributing further uncertainty around near-term demand sustainability despite supportive demographic tailwinds specifically favoring more affordable housing options.

Future Outlook: Growth Prospects and Potential Headwinds

While explicit forward guidance is absent from regulatory filings or public statements ([N#] unavailable), monitoring several key indicators may illuminate Nobility’s trajectory going forward.

Inventory absorption rates at retail sales centers will be telling as they reveal whether elevated stock levels start converting into closed sales or continue stagnating due to financing bottlenecks impeding buyer activity [S2], [S5]. Access to mortgage credit for manufactured home purchasers remains critical; tightening lending standards or rising rates could further compress sales volumes while any easing might restore momentum.

Management communicates ongoing efforts to mitigate supply chain pressures possibly through supplier diversification or procurement optimization reducing risk exposure albeit no specific milestones noted yet ([S2]). The insurance agency revenue line is expected to maintain modest growth bolstering overall financial resilience during episodic downturns.

Overall growth prospects appear tethered closely to the Florida market’s health combined with macroeconomic trends impacting affordability—thereby defining a constrained but potentially stable expansion path if material costs normalize without triggering sales deterioration.

Capital Management Strategy: Robust Balance Sheet, Dividends, and Share Repurchases

A hallmark of Nobility’s financial strategy is fiscal conservatism exemplified by zero outstanding debt alongside substantial liquidity reserves comprising over $11 million in cash plus approximately $14 million locked in certificates of deposit as reported early calendar year 2026 [F1], [S5]. The strong current ratio exceeding eight times current liabilities underscores exceptional short-term financial flexibility crucial for weathering cyclical volatility.

Shareholder returns have been prioritized within this conservative framework including timely dividends evidenced by a one-time special cash dividend of $1.50 per share declared for FY2025 payable April 2026 building on prior payouts ($1.25 per share during FY2024) showing commitment but measured capital deployment policies balancing payout with internal funding needs ([S3], [S7]).

Furthermore, selective share buybacks commenced recently with purchases totaling roughly $420K executed early in fiscal year reflecting opportunistic capital return when valuation metrics align without jeopardizing liquidity cushions ([F1], [S7]). Estimated return on equity calculated using FY2025 net income over equity stands approximately at 13.9%, signaling reasonable shareholder profitability underpinned by retained earnings growth coupled with disciplined leverage avoidance.

Operational Cash Flow Trends and Capex Efficiency

Although operating cash flow slowed significantly by about four-tenths compared to prior fiscal year ($4.2 million vs nearly $7 million), the generation remains positive affording sufficient internal funding cover for nominal capital expenditure outlays totaling just under $180 thousand annually focused on routine plant upkeep rather than growth investments ([F1]). This low capex spend relative to CFO aligns with stable manufacturing scale absent major expansions or upgrades indicating a mature asset base maintained efficiently ([S20], [S24]).

The contraction in cash flow partly derives from shifts in working capital driven by inventory buildup timing and receivables adjustments consistent with industry norms given seasonal sales patterns along with changes seen in customer deposits ([S11]). Effective management of these balancing items will be essential going forward to sustain free cash flow generation capacity supporting dividends and repurchase activity.

Risks on the Horizon: Inflation, Supply Chains, and Interest Rates

As detailed extensively in Nobility’s risk disclosures ([S4], [S10]), principal threats center on cost escalations for critical raw materials—particularly forest products used heavily in framing lumber along with other construction essentials such as vinyl siding and PVC piping whose availability remains irregular leading to backlogs.

Labor shortages contribute further upward wage pressure undermining margin stability aggravated by fuel cost inflation impacting transportation logistics throughout distribution channels.

Additionally heightened interest rates substantially affect buyer affordability constraining mortgage financing availability thereby exerting downward pressure on manufactured home demand levels especially relevant given Nobility’s Florida market concentration where competitive pricing intensifies consumer sensitivity ([S20]). The cyclicality intrinsic to the manufactured housing industry exacerbates vulnerability during economic slowdowns emphasizing prudence necessary around inventory levels and sales pacing.

Operational disruptions caused by extreme weather events remain notable risks given their potential impact on manufacturing facilities directly as well as on downstream retail operations including insurance claim cost spikes affecting related commission revenues.

This analysis integrates data strictly derived from Nobility Homes’ SEC filings through early fiscal-year-end periods alongside contextual interpretation grounded firmly on company-stated facts without speculative forecasts or extrapolations beyond available evidence.

Investors should monitor evolving macroeconomic conditions affecting consumer credit markets alongside Nobility's operational responses particularly surrounding supply chain adaptations and capital allocation choices shaping the firm’s medium-term resilience within the competitive manufactured housing landscape.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments