Envela Corp Scales Recommerce and Recycling with Strong 2025 Profit Growth Amid Market Volatility

Envela combines sustainable luxury recommerce with electronic asset recycling, posting robust revenue and earnings growth in fiscal 2025.

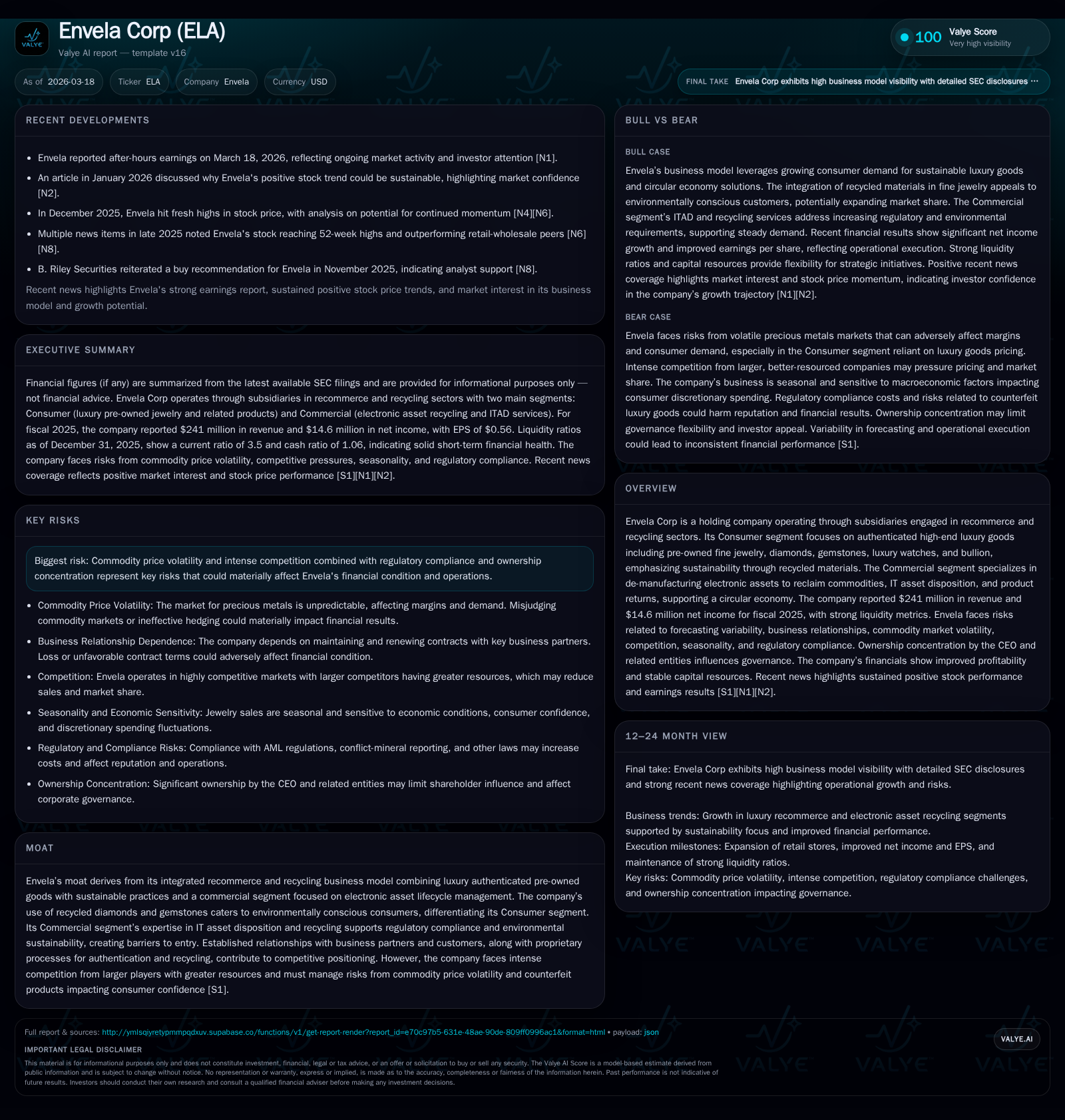

Envela Corporation delivered a significant improvement in both top-line and profitability in fiscal year 2025, driven by its integrated Consumer and Commercial segments. The company’s focus on authenticated pre-owned luxury goods embedded with recycled materials, along with end-of-life IT asset disposition and electronics recycling, underpins its differentiated market position. While revenue surged by over 30% year-over-year to $241 million and net income more than doubled to nearly $14.6 million, operating cash flow contracted amid lower capital expenditures and working capital changes. Going forward, Envela aims to expand its retail footprint and commercial processing capacity but remains exposed to commodity price swings, intense competition, and regulatory complexities.

Company Overview

Envela Corp operates primarily through subsidiaries engaged across two strategic pillars: recommerce of authenticated high-end luxury goods and commercial recycling focusing on electronic assets.[S8] The Consumer segment specializes in the sale of refurbished fine jewelry, including diamonds, gemstones, watches, and bullion products featuring recycled materials. This approach aligns with growing consumer demand for ethically sourced luxury items.[S26] Meanwhile, the Commercial segment engages in demanufacturing end-of-life IT assets to recover valuable commodities and facilitate environmentally compliant IT asset disposition (ITAD) services alongside product returns processing instrumental in supporting a circular economy.[S8][S26]

Historical Performance

In fiscal year ending December 31, 2025 (FY2025), Envela reported total revenues of $241.0 million, representing an impressive 33.6% increase over FY2024's $180.4 million.[F1] Operating income surged by 122%, reaching $18.1 million compared to $8.2 million in the prior year.[F1] Correspondingly, net income more than doubled to $14.6 million, evidencing effective cost controls and operating leverage against revenue growth trends.[F1]

Gross margin expanded substantially by $9.6 million or 21.7% over FY2024 driven predominantly by a $7 million increase in the Consumer segment's gross margin — itself a result of a substantial $62 million revenue growth offset partially by increased costs of goods sold.[S24][S27] The Commercial segment saw a moderately higher gross margin by around $2.6 million despite slightly reduced sales volumes, attributable to favorable inventory cost management and processing efficiencies.[S24][S27]

Year-over-year selling, general and administrative (SG&A) expenses fell modestly by 1.9%, signaling disciplined overhead management amidst expanding operations.[S27]

Operating cash flow however declined sharply by nearly 75%, from approximately $10.2 million in FY2024 down to about $2.6 million in FY2025.[F1] This was largely influenced by working capital impacts as well as reduced cash conversions even while capital expenditures dropped substantially from nearly $3.5 million the prior year to about $1.2 million during FY2025.[F1][S28]

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 241 | 15 | 3 | 18 | +33.6% | +116.0% |

| 2024 | 180 | 7 | 10 | 8 | -5.5% | |

| 2023 | 7 | 6 | 9 | -54.4% | ||

| 2022 | 16 | 10 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 1 | 21.8 |

| 2024 | 2 | 7 | 12.8 |

| 2023 | 4 | 14.8 | |

| 2022 | 10 | 36.2 |

Source: SEC companyfacts cache [F1].

Segment Operations Detail

Consumer Segment

The Consumer segment is at the forefront of Envela’s sustainable luxury strategy combining authenticated pre-owned pieces with innovative use of recycled gemstones and diamonds which appeal to environmentally conscious consumers seeking ethical origin products at accessible price points.[S26] This segment benefits from seasonal spikes around gifting holidays such as Valentine’s Day, Mother’s Day, and the Christmas period though these may be tempered by economic factors affecting discretionary spending.[S7]

Despite macroeconomic pressures that typically influence consumer confidence levels in luxury goods purchases, Envela managed significant revenue growth principally through expanding its retail footprint — opening one new store during FY2025 following five store openings in FY2024 — as well as bolstering its e-commerce capabilities.[S28]

Commercial Segment

The Commercial division focuses on lifecycle management for technology assets encompassing de-manufacturing electronic equipment for commodity recovery (including metals/plastics/glass), ITAD services ensuring data sanitization compliance before reuse or resale, and product returns that reintegrate goods into supply chains.[S8][S26] It also provides freight arrangement services intrinsic to inbound logistics.

Although sales slightly declined year-over-year due to varying contract terms or customer mix, this unit improved gross margins through cost reductions and operational efficiencies leading to increased absolute gross profit dollars despite softer top-line figures.[S24][S27]

The company pursues organic growth via service expansion alongside targeted acquisitions consolidating processing capacity within geographic clusters.[S20]

Capital Structure & Liquidity

Envela entered FY2025 positioned comfortably with a strong liquidity profile — current assets stood at approximately $65.4 million against current liabilities of about $18.7 million yielding a current ratio close to 3.5x.[F1][S11] Cash balances remained robust at over $18 million with notes payable declining significantly from prior year levels ($9.9M vs ~$13.5M).[F1][S11]

Moreover, operating lease liabilities nearly doubled reflecting increased real estate commitments aligned with new retail expansions but are supported by enhanced operating earnings capacity.[S17] Adjusted leverage ratios incorporating lease obligations show conservative coverage metrics relative to adjusted EBITDAR.

The company finished FY2025 with shareholder equity rising roughly 27%, now exceeding $67 million reflective of strong retained earnings accumulation plus limited share repurchases totaling under $190K compared to over $2M retired shares previous year.[F1][S14]

Capital expenditures were curtailed considerably as management prioritized cash conservation following heavier investments in prior years’ store rollouts and ERP system upgrades.[F1][S28]

Future Growth Prospects

Envela's growth will likely hinge on further developing both segments synergistically:

- Consumer: Expanding brick-and-mortar locations nationwide strategically while scaling digital platforms offers organic revenue upside given growing recommerce demand and sustainability trends among luxury consumers.

- Commercial: Enhancing contractual arrangements with major business partners alongside facility optimization can consolidate market share in ITAD/recycling spaces increasingly governed by tightening environmental regulation.

- Selective acquisitions remain a tactical pathway for geographic coverage enhancements especially near existing facilities reducing integration complexity.[N1][S20]

Nonetheless, constraints exist including exposure to volatility in precious metals markets which directly impacts inventory valuations/cost basis,[S1] unpredictability of consumer discretionary spending particularly amid inflationary pressures, heightened competition from deeper-pocketed rivals,[S13] seasonality effects skewing quarterly comparability,[S7], and regulatory compliance demands both domestically and international jurisdictions complicating operational agility.

Risks & Governance Considerations

Key risks highlighted include:

- Significant exposure to commodity price fluctuations impacting margins for bullion-related inventory despite hedging mechanisms employed.

- Dependence upon maintaining strong business partner relationships especially within commercial contracts where termination or unfavorable renegotiations could materially impact revenues.

- Ownership concentration primarily held by CEO-related entities poses potential governance challenges or conflicts of interest requiring investor scrutiny regarding management accountability.

- Competition intensity across both segments from larger competitors leveraging scale and brand recognition.[S1][S13]

What to Watch Forward - Analysis

Absent explicit multi-year guidance disclosures,[N1] monitoring should focus on:

- Pace of Consumer segment store openings coupled with online channel development effectiveness.

- Trends in commodity pricing influencing margin stability particularly given inventory sensitivities.

- Success factors in contract renewals or new wins within commercial services pipeline.

- Operating cash flow trajectory relative to capital expenditure requirements signaling investment sustainability or need for financing adjustments.

- Any shifts in ownership governance that might affect strategic decision-making or shareholder interests.

Conclusion

Envela Corp’s integrated recommerce plus electronics recycling model has yielded robust financial improvement recorded in fiscal year ended December 2025. Revenue expanded above expectations while net profit margins widened significantly evidencing operational execution strength albeit offset partially by working capital pressures impacting free cash flow conversion metrics. The company is strategically positioned at the nexus of sustainability-focused consumer luxury demand alongside growing regulatory-driven commercial electronics recycling needs — two markets expected to endure long-term structural tailwinds but clouded near-term by macroeconomic uncertainty and commodity market volatility. Careful attention should be paid going forward towards sustaining momentum across both hallmark segments while managing inherent risks related to pricing environment sensitivity, competitive landscape dynamics, seasonality fluctuations, and governance structures centered on concentrated insider ownership.

This report is intended solely for informational purposes based on publicly available information as of March 18th, 2026. It does not constitute investment advice or solicitation for any securities transaction.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments