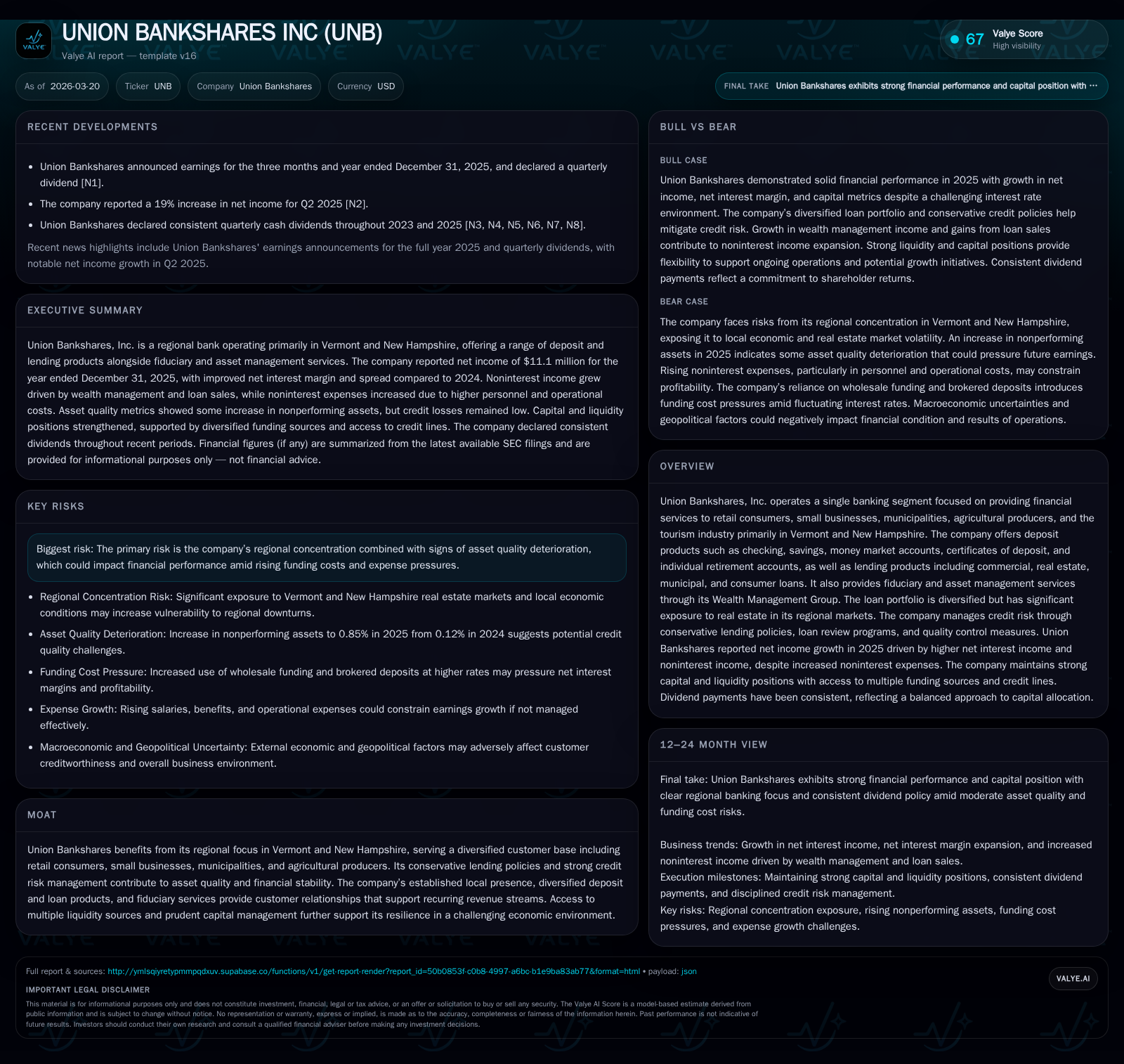

Union Bankshares Navigates Credit Challenges While Enhancing Liquidity and Capital Position in 2025

Union Bankshares delivered stable operational cash flow growth and maintained capital adequacy amid modest net income decline and rising credit risks concentrated in regional real estate portfolios.

Union Bankshares, serving primarily Vermont and New Hampshire markets, reported a slight decrease in net income for 2025 despite improved net interest margins and efficiency gains. Operating cash flow grew strongly, reflecting robust core banking activities. The bank faces elevated nonperforming assets linked to its real estate loan concentration but sustains solid capital ratios supported by retained earnings and equity issuances. Diversified liquidity sources and a recent leadership transition position the company for measured growth while managing asset quality risks.

Company Overview

Union Bankshares, Inc. primarily operates within Vermont and New Hampshire, servicing retail consumers, small businesses, municipalities, agricultural producers, and tourism-related sectors. Its product suite includes diversified deposit offerings such as checking accounts, certificates of deposit (CDs), IRAs, as well as lending products heavily weighted towards commercial and residential real estate loans alongside municipal financing. The Wealth Management Group provides fiduciary and asset management services.

Historical Performance

In fiscal year 2025, Union Bankshares recorded net income of $2.75 million, down approximately 8.4% from $3.00 million in 2024 despite quarterly improvements earlier in the year as documented in SEC filings [F1], [S1]. This decline contrasts with a significant increase in operating cash flow (CFO), which rose from $12.15 million in 2024 to $17.23 million in 2025 (+41.8%), reflecting solid working capital management and loan amortization supporting cash generation.

The bank's net interest margin (NIM) improved by 16 basis points to a fully tax-equivalent margin of approximately 2.93%. This was driven by higher average yields on earning assets—particularly loans and investment securities—and strategic repositioning of the debt securities portfolio intended to enhance future earnings potential [S1]. The net interest spread widened from about 2.30% to roughly 2.47%, illustrating improved pricing power amid prevailing rate conditions.

Cost control efforts yielded an efficiency ratio improvement from about 77.6% to near 75.1%, demonstrating disciplined expense management despite inflationary headwinds.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 3 | 17 | 1253000 | -8.4% |

| 2024 | 3 | 12 | 1071000 | -1.6% |

| 2023 | 3 | 9 | 1946000 | -11.5% |

| 2022 | 3 | 29 | 665000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 7 | 16 | |

| 2024 | 7 | 0 | 11 |

| 2023 | 6 | 130000 | 7 |

| 2022 | 6 | 79000 | 28 |

Source: SEC companyfacts cache [F1].

Table: Selected Financial Metrics for Union Bankshares (source: F1)

Business Drivers & Risks

Union Bankshares benefits from a strong regional franchise underpinned by deep community relationships across its geographic footprint in New England, providing tailored financial solutions that generate recurring fee income streams including fiduciary services [S12]. However, geographic concentration poses risks as nonperforming assets increased significantly to around 0.85% of total assets at the end of 2025—a marked rise from near negligible levels previously—primarily tied to its real estate-heavy loan portfolio within Vermont and New Hampshire markets [S1].

Credit risk management remains conservative with allowances for credit losses aligned with CECL requirements increasing moderately alongside cautious underwriting policies; nevertheless, the concentration in real estate heightens vulnerability to local economic softness or market downturns [S1]. Rising funding costs combined with competitive pressures on deposit pricing may compress margins if reliance on wholesale funding grows beyond current levels.

Capital Allocation & Liquidity

Capital ratios remain robust with total capital to risk-weighted assets at approximately 12.8%, supporting regulatory compliance and enabling future lending growth [F1], [S1]. Return on average equity was around mid-teens percentage levels according to SEC disclosures, consistent with moderate profitability tempered by slower top-line expansion.

Dividend payments held steady at $1.44 per share during both years analyzed; however, the dividend payout ratio decreased from over 74% in prior periods to near 59%, signaling a more balanced approach favoring retained earnings for reinvestment or capital buffers amid evolving credit conditions [F1], [S1].

Liquidity is prudently managed through multiple channels including substantial unused Federal Home Loan Bank lines of credit totaling roughly $48 million beyond outstanding borrowings, master brokered deposit agreements, retail brokered certificates of deposit totaling approximately $10 million, along with contingent liquidity embedded within the securities portfolio enabling flexible responses to funding needs or loan demand variability [S4], [S6], [S9].

The company maintains access to public capital markets through an at-the-market equity offering program which generated net proceeds exceeding $1 million during fiscal year 2025 without material shareholder dilution—this supports long-term capital strategy facilitating organic growth or opportunistic acquisitions as circumstances warrant [S11], [S18].

Outlook & Strategic Considerations

No formal forward guidance has been issued; however monitoring key indicators such as loan performance metrics (notably nonperforming asset trends), margin stability amid interest rate fluctuations, shifts in deposit composition especially regarding brokered or wholesale sources, and continued efficiency improvements will be essential for assessing future operating trajectories.

A leadership transition is underway with Jeffery F. Weidley appointed President effective May 4, 2026 ahead of CEO retirement mid-year—a development that may signal strategic continuity or recalibration depending on emerging priorities at the firm level [S3].

Given these factors, sustainable growth prospects hinge on effectively managing localized credit pressures while leveraging strong customer relationships and product diversity that provide some insulation against cyclical volatility.

Conclusion

Union Bankshares exemplifies a regional community bank balancing traditional strengths with disciplined financial management: it experienced modest net income contraction offset by materially improved cash flows and operational efficiency during fiscal year 2025 despite challenges from rising credit risks concentrated in its regional real estate portfolio. Its conservative capital posture combined with extensive liquidity facilities positions it well for resilience; however execution risks remain centered on maintaining asset quality amid funding cost pressures and competitive dynamics inherent in its business model concentration. Leadership succession later this year will be an important factor shaping the company's strategic direction moving forward.

This analysis synthesizes publicly available SEC filings and financial data without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments