WEWARDS Faces Persistent Liquidity and Revenue Challenges with Bitcoin Rewards Platform

Despite innovative Bitcoin rebate and gaming IP, WEWARDS has not generated revenue since 2021 and remains heavily reliant on CEO-controlled loans amid liquidity strains.

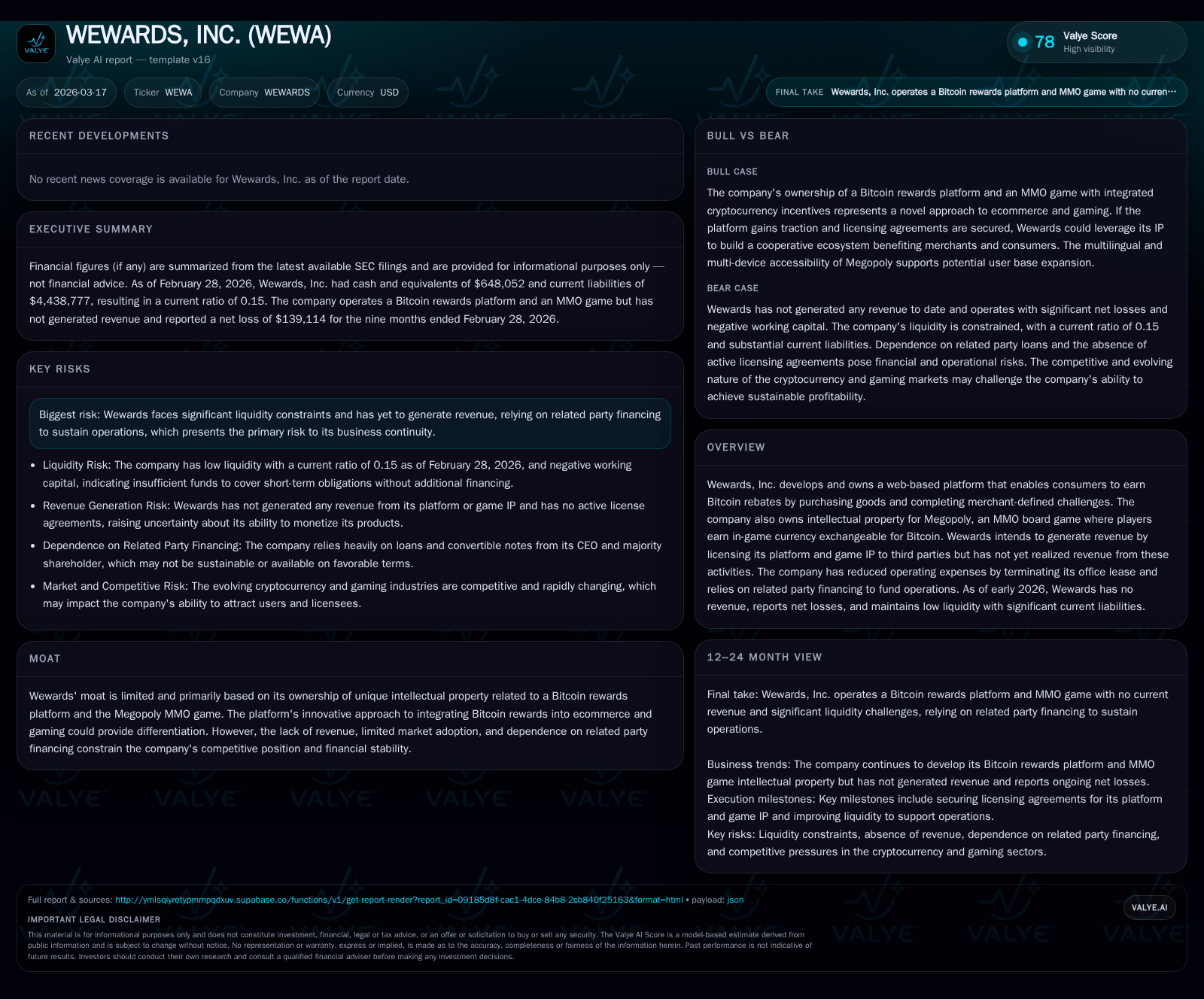

WEWARDS, Inc. operates a web-based platform rewarding consumers with Bitcoin rebates and owns intellectual property for the Megopoly MMO game where in-game currency can be exchanged for Bitcoin. Despite innovative concepts, the company has not generated revenues since FY2021 and remains financially strained with a low current ratio and large accrued interest liabilities. Reliance on related party convertible loans controlled by CEO Lei Pei underscores ongoing funding risks. Licensing of white-label platforms and gaming IP remains the intended growth path, but no material agreements have been secured to date.

Innovative Platform with Delayed Commercial Traction

WEWARDS, Inc. operates a web-based platform accessible through mobile apps designed to reward consumers with Bitcoin rebates when they complete merchant-defined challenges [S1]. This creates a cooperative commerce ecosystem aiming to distribute commercial wealth between merchants and consumers using Bitcoin as the reward currency.

In addition, WEWARDS acquired intellectual property rights in April 2020 related to Megopoly, an MMO board game where players trade virtual real estate with an in-game currency (Megopoly Coins) exchangeable for Bitcoin at real-time rates [S14]. Megopoly supports gameplay across devices in both English and Chinese, blending traditional gaming mechanics with cryptocurrency incentives.

Despite these assets within ecommerce and gaming technology spheres, the company has yet to secure external licensing agreements that generate revenue from either the Platform or Megopoly [S1][S14]. This reflects an early-stage monetization phase facing significant challenges in market adoption.

Historical Financial Performance: No Revenue, Narrowing Losses

Financial data shows no revenues since FY2022 after modest $83K licensing income reported in FY2021 largely from related parties [F1][S1]. Operating losses improved markedly from -$1.87 million in FY2022 to -$90.7 thousand in FY2025 driven primarily by cost reductions rather than sales growth [F1][S4]. Net losses decreased slightly over this period but remain material at -$596K for FY2025 [F1].

Operating cash flows used have similarly improved from -$1.86 million in FY2022 to -$70.9 thousand in FY2025 reflecting tighter expense control [F1][S5]. However, continued negative free cash flow underscores ongoing investment without offsetting revenues.

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -1 | -70915 | -90670 | +8.5% |

| 2024 | 0 | -1 | -125200 | -145846 | +14.3% |

| 2023 | -1 | -250977 | -245331 | +68.1% | |

| 2022 | -2 | -1859416 | -1865309 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 4.3 |

| 2024 | 4.9 |

| 2023 | 6.0 |

| 2022 | 20.1 |

Source: SEC companyfacts cache [F1].

Severe Liquidity Constraints and Capital Structure

As of February 28, 2026, cash and equivalents stood at approximately $648K against current liabilities exceeding $4.4 million resulting in a current ratio near 0.15—indicating acute short-term liquidity pressure [F1][S6]. A significant portion of liabilities consists of accrued interest on related party convertible loans controlled by CEO Lei Pei and affiliated entities [S3][S6].

Since Mr. Pei gained control in 2015, WEWARDS has depended almost exclusively on related party financing generally structured as convertible debt [S3]. There is no assurance such support will continue or be available on favorable terms [S3][S8]. The termination of office lease in October 2023 reduced rent expenses materially but did not resolve fundamental liquidity issues [S4][S8]. Operating cash outflows remain negative despite cost containment efforts.

Licensing Strategy as Growth Lever

The company’s growth strategy focuses on licensing white-label versions of its Bitcoin rewards Platform to third parties who would integrate or distribute it within their ecommerce offerings [S14]. Additionally, Megopoly is intended to generate revenue through licensing contracts comprising software licenses combined with online hosted service fees including fixed minimum guarantees plus sales royalties based on user engagement [S14][S19].

To date however, no material third-party licensing agreements have been executed outside affiliated entities; thus revenue streams remain non-existent [S1][S14]. Successful commercialization depends on securing such partnerships.

Capital Allocation Reflects Early-Stage Investment Needs

No dividends or stock repurchases have been made; capital allocation prioritizes sustaining research & development efforts and general administrative functions amid unprofitable operations [F1][S18]. Approximately 4.3% return on equity is nominally indicated by net loss relative to deeply negative equity balances stemming from accumulated deficits over time [F1]. Free cash flow remains negative consistent with ongoing investment without offsetting income generation.

Risks Centered on Financing and Market Adoption

Risk disclosures emphasize illiquidity exacerbated by zero revenues from commercializing unique crypto-linked IP; heavy reliance on CEO-affiliated financing sources; uncertain market acceptance of Bitcoin rebate ecosystems; regulatory uncertainties surrounding digital currency reward platforms; competitive pressures inherent in incentive-based consumer engagement models; and limited litigation risk currently identified [S7][S10][S11].

Outlook: Key Metrics for Monitoring Progress

Absent explicit guidance or milestone disclosures beyond stated intentions:

- Execution of definitive licensing contracts that lead to ASC 606-compliant revenue recognition will be critical,

- Improvement in liquidity ratios reflecting reduced reliance on related party debt,

- Reduction in accrued interest obligations,

- Observable user adoption metrics for Megopoly or Platform usage signaling commercial traction.

Quarterly filings should be monitored closely for updates on license agreements or partnership developments that signal transition from capital-dependent survival toward sustainable growth.

This report synthesizes SEC filings and XBRL financial data strictly without projecting outcomes beyond documented evidence. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments