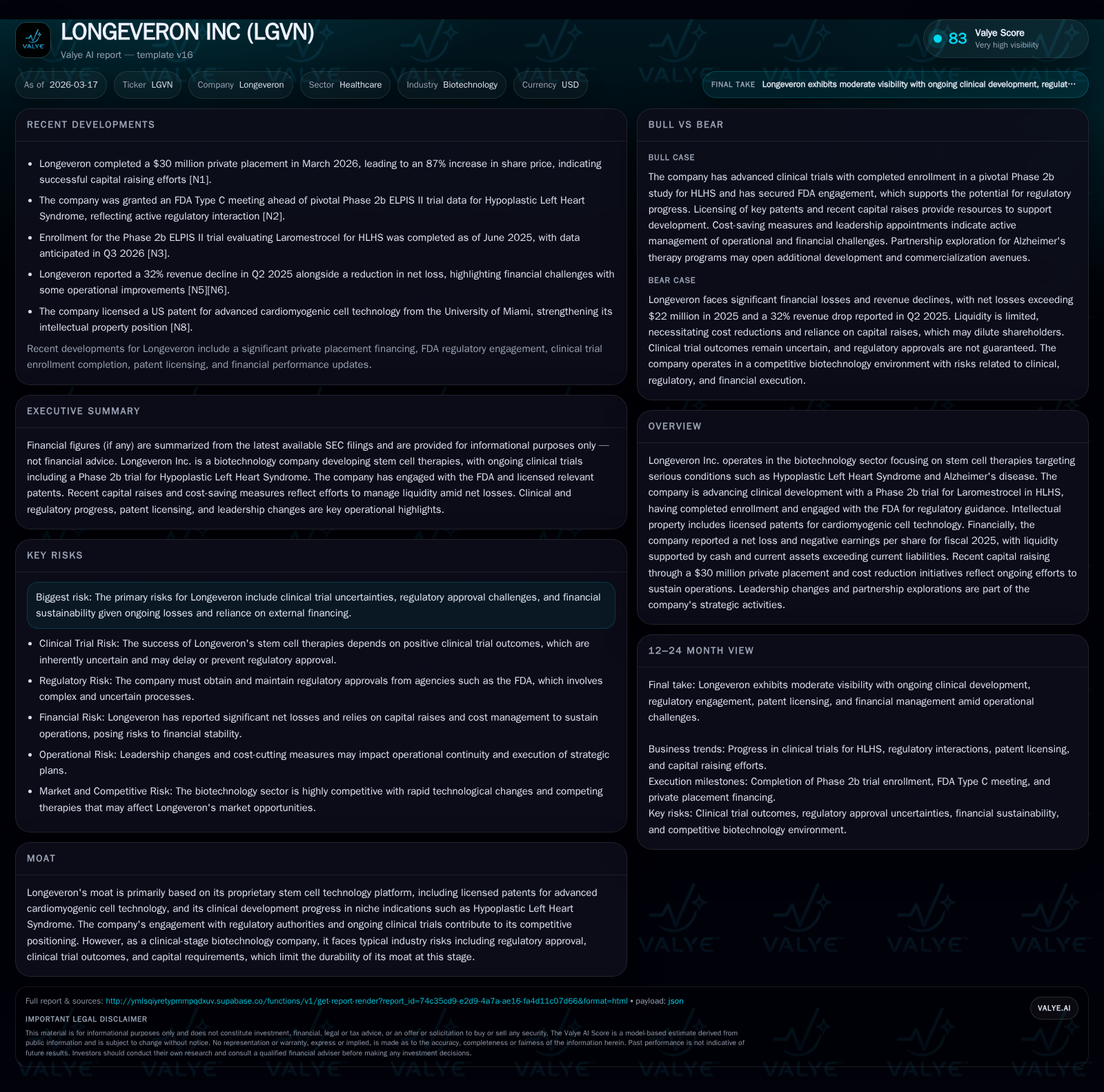

Longeveron’s Quest: Stem Cell Innovation Meets Financial Hurdles

Longeveron pursues pioneering stem cell therapies for rare diseases while confronting persistent financial and regulatory challenges typical of clinical-stage biotech.

Longeveron Inc. focuses on developing stem cell treatments for critical conditions such as Hypoplastic Left Heart Syndrome (HLHS), advancing a Phase 2b trial for its lead product Laromestrocel with ongoing dialogue with the FDA. The company’s proprietary cardiomyogenic stem cell platform underpins its niche competitive moat, but Longeveron remains a pre-commercial entity confronted by steep operating losses and negative cash flows. The recent $30 million capital raise extends its runway through late 2026, yet the business faces substantial going concern risks and dependence on further financing. Key upcoming milestones center on Phase 2b trial outcomes and regulatory feedback, while capital allocation prioritizes R&D over shareholder returns amid a negative ROE environment.

Clinical Breakthroughs and Technology Foundation

Longeveron's scientific core is anchored in its proprietary stem cell platform leveraging licensed patents specifically covering cardiomyogenic cell technology targeting rare diseases such as Hypoplastic Left Heart Syndrome (HLHS) and Alzheimer’s disease.[S1,N1] Its lead product candidate, Laromestrocel, is currently in a Phase 2b clinical trial designed to assess safety and efficacy in HLHS patients, with enrollment completed—a key milestone given the complexity of recruiting in niche indications.[S1] The company maintains active engagement with the FDA to align developmental endpoints and regulatory expectations.

While patent protection provides a specialized technological moat, Longeveron remains an early-stage clinical entity with significant regulatory and scientific risks ahead.

Revenue Trajectory and Historical Performance

Longeveron’s financial history reflects a pre-commercial profile characterized by declining revenues alongside increasing losses due to clinical investments. The following table summarizes key historical financial data from fiscal years 2022 through 2025:[F1]

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -23 | -19 | -23 | -42.1% | ||

| 2024 | -16 | -14 | -17 | +25.4% | ||

| 2023 | 709000 | -21 | -19 | -21 | -42.0% | -13.7% |

| 2022 | 1222000 | -19 | -14 | -18 | -6.4% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -19 | -400.1 |

| 2024 | -15 | -73.0 |

| 2023 | -19 | -317.7 |

| 2022 | -15 | -91.9 |

Source: SEC companyfacts cache [F1].

Revenue declined approximately 42% from FY2022 to FY2023 reflecting absence of commercial products. Operating losses widened to $23.3 million by FY2025 as clinical activities intensified. Negative net income and operating cash flows underscore sustained cash burn inherent in the company’s development stage.

Capital Structure and Liquidity Position

At December 31, 2025,[F1] Longeveron held $4.7 million in cash and equivalents against current liabilities of approximately $4.1 million—yielding a current ratio near 1.33—indicating sufficient short-term liquidity but limited cushion beyond immediate obligations.

To bolster liquidity amid ongoing cash burn and operating losses,[N1,S3] Longeveron completed a $30 million private placement financing in early March 2026. This infusion extended the company's expected operational runway into the fourth quarter of 2026 according to management disclosures.[S1]

Despite this capital raise,[S3,S5] the company continues to face substantial going concern risks due to recurring losses exceeding $132 million accumulated deficit by end-2025,[S1,F1] highlighting dependence on future financings or collaborations for survival.

Governance Changes and Cost Management

In February-March 2026,[S4,S8,S10] Longeveron implemented executive salary reductions of approximately 50% alongside furloughs and board fee cuts as part of broader cost-saving measures. Stephen Willard was appointed permanent CEO effective February 11, 2026,[S12] bringing over three decades of biopharma leadership experience.

The company intends to grant equity awards to executives as retention incentives during this financially constrained period,[S4,S10] reflecting alignment of management interests with long-term value creation despite near-term challenges.

Regulatory Engagement and Development Outlook

With no approved products currently on market,[S1] Longeveron's value proposition hinges on successful progression of Laromestrocel through its Phase 2b trial for HLHS—an area lacking effective therapies. Positive trial outcomes could enable accelerated regulatory pathways pending FDA feedback,[N1,S1] which remains closely monitored by investors.

No definitive timelines for data readouts beyond enrollment completion have been disclosed publicly; interim analyses or top-line results will serve as critical catalysts.

Capital Allocation Priorities

Reflecting its clinical-stage status,[F1,S4,S8,S10] Longeveron's capital deployment remains focused almost exclusively on research and development activities rather than shareholder returns. There are no dividends or share repurchases reported.

This approach manifests financially via negative return on equity approximating -400%, indicating that invested capital is consumed by operating deficits without earnings generation.[F1]

Summary: Investment Considerations

Longeveron represents a high-risk biotech investment premised on stem cell innovation targeting rare diseases but constrained by persistent financial losses and funding needs. Key factors for investors include:

- Monitoring Phase 2b trial progress and FDA interactions;

- Tracking liquidity trends post-$30 million raise;

- Observing any strategic partnerships or new financing announcements;

- Evaluating management’s execution of cost controls amid operational scaling.

This analysis synthesizes publicly available SEC filings and news up to March 17, 2026 without investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments