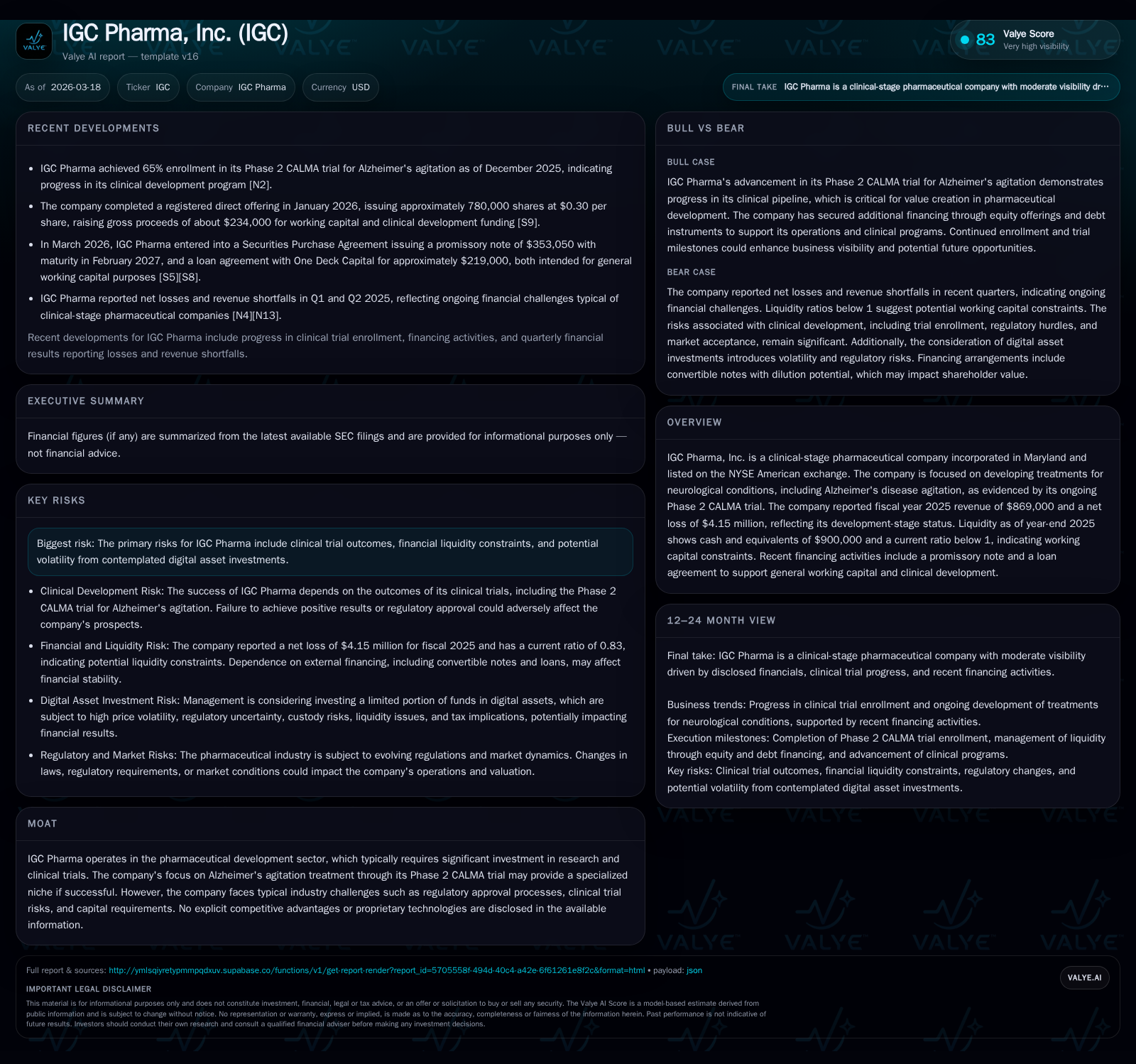

IGC Pharma Advances Clinical-Stage Neurological Pipeline Amid Funding Hurdles

IGC Pharma pushes forward its Alzheimer’s agitation treatment program while managing liquidity constraints and evolving capital strategies.

IGC Pharma, a clinical-stage biopharmaceutical company, reported fiscal year 2025 revenue of $869,000 with a net loss improved to $4.15 million. Its core development effort centers on the Phase 2 CALMA trial for Alzheimer’s agitation. Recent debt financings aim to bolster working capital, though the current ratio under one signals sustained liquidity pressure. Management’s consideration of digital assets for treasury diversification introduces novel risks uncommon in early-stage pharma firms. Continuous monitoring of clinical milestones and financing needs will be critical in assessing its path forward.

Steady Progress in Neurological Therapeutics: Historical Revenue and Operating Trends

IGC Pharma is an emerging clinical-stage pharmaceutical company focused on neurological conditions with particular emphasis on Alzheimer’s disease agitation. Its financials illustrate classic early-stage drug developer dynamics marked by modest revenues related mostly to licensing fees or service arrangements, alongside substantial R&D investment driving operating losses.

For fiscal year 2025 ending December 31, IGC reported revenues of $869,000 representing a significant -35.4% decline from $1.345 million recorded as of March 31, 2024 [F1]. This top-line contraction appears linked primarily to the inherent timing variability of milestone payments or collaboration income tied to pipeline progression rather than core product sales.

Despite diminishing revenue, operating income loss improved notably by about 21% from -$9.8 million in FY24 to -$7.75 million in FY25 [F1]. This narrowing reflects concerted cost management and prioritization of spending towards key clinical activities consistent with the company's Phase 2 CALMA trial efforts. Net loss also shrank materially by over two-thirds, from -$13 million to roughly -$4.15 million—supported by reduced operational cash burn.

Operating cash flow remained negative at -$4.72 million but improved compared to previous years, signaling stabilization though not yet sustainability [F1]. Capital expenditures were minimal at $49,000 showing no material reinvestment outlays typically seen in later-stage pharma players.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 869000 | -4 | -5 | -8 | -35.4% | +68.1% |

| 2024 | 1345000 | -13 | -5 | -10 | +47.6% | -13.0% |

| 2023 | 911000 | -12 | -7 | -12 | +129.5% | +23.4% |

| 2022 | 397000 | -15 | -7 | -15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -55.9 |

| 2024 | -5 | -177.6 |

| 2023 | -7 | -77.2 |

| 2022 | -8 | -62.8 |

Source: SEC companyfacts cache [F1].

The table summarizes IGC Pharma's recent operating results emphasizing volatile revenues typical for clinical-stage biopharma alongside improving loss metrics indicative of refined burn rate management.

Capital Structure Dynamics: Recent Financings and Liquidity Pressures

Managing liquidity remains a key challenge for IGC Pharma as it continues funding expensive clinical trials without commercial product revenues. At the close of fiscal year 2025, the company held only $900,000 in cash with current liabilities exceeding current assets at $2.16 million against $1.79 million respectively—yielding a current ratio of approximately 0.83 [F1]. This shortfall indicates potential working capital constraints requiring near-term financing interventions.

Recent filings reveal material debt raises aimed at supplementing operational cash flow: On March 5, 2026, IGC entered into a Securities Purchase Agreement issuing a promissory note to Vanquish Funding Group for $353K principal amount [S3][S5][S6]. Further financing included a loan agreement with One Deck Capital totaling around $219K.[S5] Both financings are intended principally for general working capital and ongoing clinical development expenses.

The convertible note carries protections constraining dilutive conversions capped at under 20% of outstanding shares absent shareholder approval per NYSE American regulations [S6]. Additionally, conversion rights include a limitation preventing Vanquish from owning more than approximately 5% beneficial ownership through note conversion rights ensuring controlled shareholder dilution.

On the equity front, the October 2025 annual meeting approved increasing authorized common stock from 150 million to 600 million shares providing flexibility for future capital raises without immediate equity issuance [S9]. Despite this authorization expansion and recent registered direct offerings raising roughly $234K net proceeds in January 2026 [S18], working capital remains marginal necessitating continued financing vigilance.

Clinical Development Focus: Phase 2 CALMA Trial in Alzheimer's Agitation

IGC’s foremost clinical initiative is its Phase 2 CALMA trial targeting agitation in Alzheimer’s disease—an indication representing a high unmet medical need within neurodegenerative disorder therapeutics . The CALMA study embodies typical mid-stage clinical pipeline risk factors including dose optimization refinement and efficacy endpoint validation before regulatory submission prospects can be contemplated.

Precision around trial phases is crucial: Phase 2 suggests initial human proof-of-concept data generation but precedes effectiveness confirmation required for pivotal Phase 3 trials generally necessary for market approval. Results from CALMA will materially influence both downstream partnering interest and capital appetite as regulatory authorities weigh safety/efficacy balance for this challenging neurological symptom domain.

Given Alzheimer’s agitation remains underserved with few approved pharmacological options beyond symptomatic relief agents prone to adverse effects such as sedation or motor impairment—IGC’s niche emphasis is strategically targeted yet fraught with classic regulatory uncertainties that often lengthen timeframes and inflate costs within neuropsychopharmacology development realms.

Emerging Considerations: Digital Asset Investment Initiative and Associated Risks

In an unconventional move for a nascent pharmaceutical enterprise focused on neurological drug discovery programs, IGC management is contemplating adoption of a treasury policy enabling investment of limited funds into digital assets including cryptocurrencies either directly or through exchange-traded products (ETPs) [S2][S4][S7]. Though no purchases occurred as of late-2025 reporting dates,[S2] several categories of risk are explicitly disclosed:

- Price Volatility: Cryptocurrencies exhibit historic price fluctuations driven by market sentiment shifts and macroeconomic swings potentially amplifying earnings volatility.

- Regulatory Risk: Evolving compliance landscapes across federal/state jurisdictions could impede trading or holding activities impacting asset values adversely.

- Custody & Operational Risk: Exposure arises from cybersecurity breaches or custodial insolvencies jeopardizing asset security.

- Liquidity Risk: Trading venues might experience outages limiting transactional access especially during stressed markets.

- Tax & Accounting Impact: Potential Corporate Alternative Minimum Tax liabilities on unrealized gains plus mandated fair value accounting introduce further earnings variability.

This proposed diversification represents an atypical exposure profile for early-stage biopharma treasury strategies which traditionally prioritize liquidity preservation facilitating uninterrupted R&D expenditure schedules rather than speculative asset classes.

Outlook and Milestones: What to Watch in IGC Pharma’s Path Forward

IGC has not released formal guidance or forecast metrics publicly regarding clinical data readout timing or anticipated financial milestones [N1][S3]. Market participants should track several critical upcoming catalysts:

- Final data releases from the Phase 2 CALMA trial; positive signals could unlock strategic partnerships or licensing deals vital for long-term viability.

- Debt maturity schedules particularly around February 28, 2027 concerning the promissory note; refinancing negotiations will be essential given tight liquidity conditions.

- Potential additional equity offerings leveraging recently expanded authorized share count; capacity exists but timing remains uncertain given balancing shareholder dilution concerns versus urgent cash needs.

Close attention to quarterly filings disclosing burn rates post financing initiatives will illuminate whether IGC can bridge operating deficits successfully through capital markets access while progressing towards pivotal clinical endpoints.

Capital Allocation Review: Lack of Dividends or Buybacks, Cash Burn Profile, and ROE Analysis

IGC Pharma does not currently pay dividends nor has it engaged in share repurchase programs recently reflecting standard practice among development-stage biotechs where available cash opts towards sustaining R&D pipelines rather than distributions [F1][S9][S14][S16].

Operating cash flow trends remain negative—FY25 CFO was approximately -$4.72 million while capex was negligible at $49K yielding free cash flow near -$4.77 million consistent with typical clinical-stage burn profiles seeking proof-of-concept through costly trial execution [F1].

Equity base contracted markedly over prior years from roughly $23.9 million in FY22 down to $7.42 million as of end FY25 illustrating substantial accumulated losses eroding net assets [F1]. This dynamic drives an estimated return on equity (ROE) near negative -56%, emphasizing the high capital intensiveness and risk associated with early pharmaceutical innovation absent commercialized products.

Future focus on improving ROE metrics depends heavily on advancing portfolio candidates toward commercialization stages where revenues scale relative to fixed overheads reducing loss ratios fundamentally.

Disclaimer: This analysis summarizes public financial data and disclosures as of March 18, 2026. It does not constitute investment advice or recommendations but aims to provide an informed overview based on available sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments