Alpha Star Acquisition Corp's Path to Value Creation Through Strategic SPAC Merger

Alpha Star Acquisition Corp’s evolution as a blank check company highlights key financial patterns and critical dependencies on its merger with OU XDATA Group.

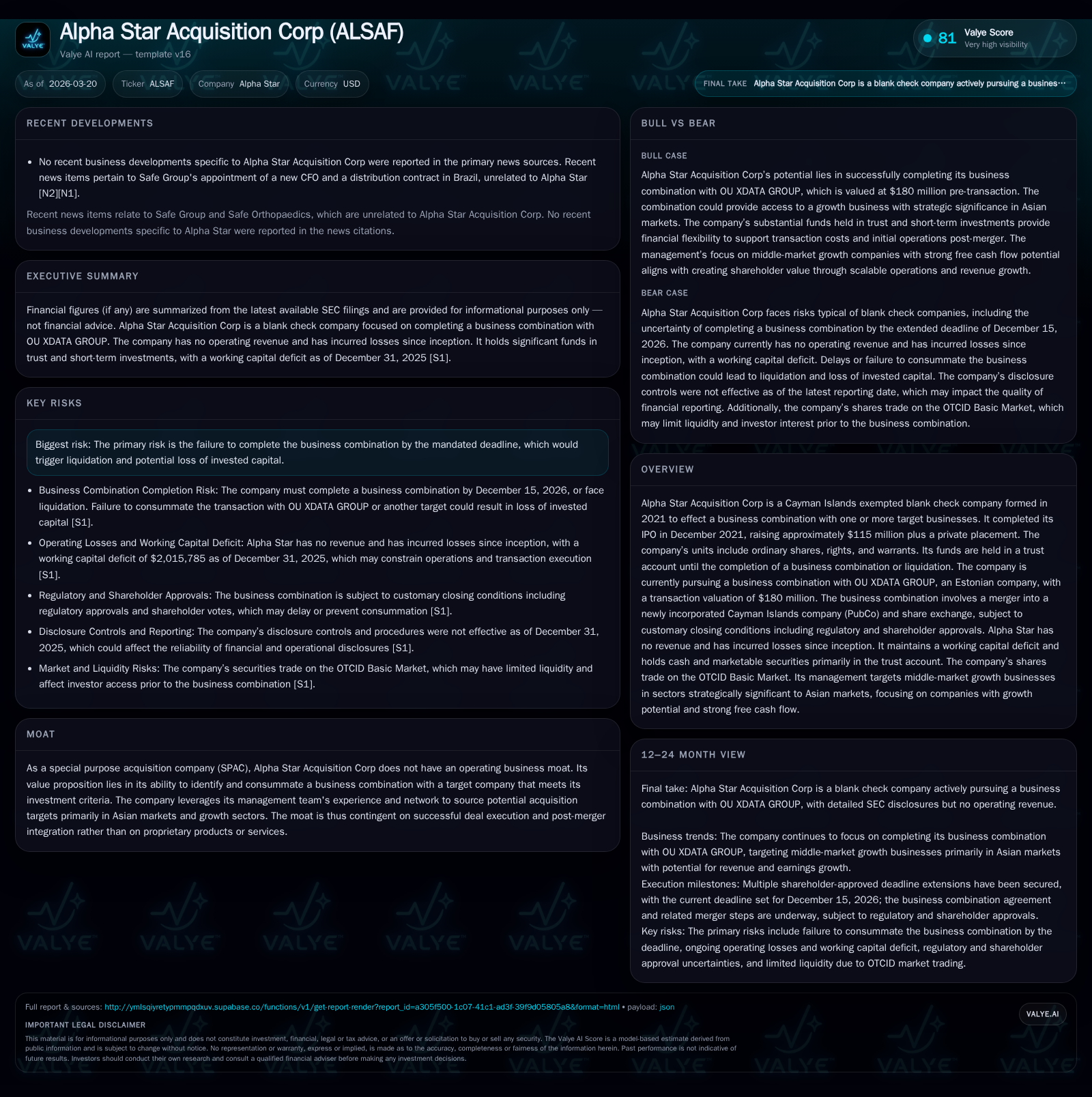

Since its inception in 2021, Alpha Star Acquisition Corp (ALSAF) has operated solely as a special purpose acquisition company (SPAC) without revenue generation, incurring consistent operating losses. It raised an aggregate of $118.3 million in late 2021 through an IPO and private placement, holding most funds in a trust account pending its initial business combination. The company is currently pursuing a merger with Estonia-based OU XDATA Group, structured as a Cayman Islands merger and share exchange subject to regulatory and shareholder approvals. ALSAF’s liquidity has been challenged by working capital deficits and reliance on interest-free sponsor loans to finance transaction costs. Completion risks persist, tied principally to meeting the December 2026 deadline and securing necessary approvals. No dividends or buybacks have occurred, and operating cash outflows reflect ongoing preparatory expenses; the planned business combination and relisting would mark significant milestones going forward.

Alpha Star’s Historical Financial Footprint: Losses and Limited Operations

Alpha Star Acquisition Corp (ALSAF) is a Cayman Islands-exempted blank check company formed in March 2021 with the purpose of effecting an initial business combination by December 15, 2026. As expected for a SPAC without operational business activity, ALSAF has reported no revenue since formation. Its operations have been limited to organizational activities, preparation for the IPO completed in December 2021, and identification of acquisition targets culminating in a signed Business Combination Agreement with OU XDATA Group.

Financially, ALSAF has incurred net losses recently after prior positive net income years largely due to interest income on marketable securities held within the trust account [F1][S1]. Operating income reflects continuous negative results driven by formation costs, legal fees, accounting compliance expenses, underwriting fees, and ongoing public company administrative costs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -1 | -651811 | -887584 | -163.0% |

| 2024 | 1 | -243395 | -913909 | -72.7% |

| 2023 | 5 | -235925 | -435287 | +344.8% |

| 2022 | 1 | -276867 | -587614 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 28.6 |

| 2024 | -37.2 |

| 2023 | -54.3 |

| 2022 | -24.5 |

Source: SEC companyfacts cache [F1].

Operating losses have deepened modestly year-over-year while net income displays volatility owing to variable gains from interest income and mark-to-market movements on trust assets.

Capital Origination and Trust Account Structure Post-IPO

ALSAF raised approximately $115 million gross proceeds from its December 2021 initial public offering through the sale of 11.5 million units priced at $10 each [S1]. Concurrently with the IPO closing date, the Sponsor privately purchased an additional 330,000 units at $10 per unit for proceeds of $3.3 million under a private placement agreement [S1][S27].

These funds were largely placed into a U.S.-based trust account established to safeguard investors’ capital until closure of the initial business combination or liquidation [S8]. Interest earned on these holdings is retained unless withdrawn to pay taxes. Transaction costs including underwriting fees totaled approximately $5.67 million across underwriting commissions and related offering expenses [S1][S8]. Deferred underwriting fees were partially reduced in October 2025 from $2.875 million to $950 thousand reflecting adjustments related to shareholder redemptions [S29].

Strategic Merger with OU XDATA Group: Transaction Terms and Outlook

On September 12, 2024, ALSAF signed a business combination agreement with OU XDATA Group (“XDATA”), an Estonian technology company [S14]. The transaction contemplates incorporation of a new Cayman Islands exempted company (“PubCo”), into which ALSAF will merge via share exchange [S14]. Post-merger ownership will be primarily through share interests in PubCo.

The total valuation of the combined entity is approximately $180 million , positioning this as ALSAF’s inaugural operational platform following years as a SPAC shell.

Completion depends critically on customary closing conditions including regulatory clearance in applicable jurisdictions and stockholder approval votes [S14]. Given ALSAF's lack of substantive operations outside its SPAC structure (“moat”), value creation hinges on successful merger completion.

Liquidity Profile and Working Capital Challenges Amid Sponsor Loans

Liquidity remains constrained for ALSAF as it reports nil cash balances at December 31, 2025 coupled with a working capital deficit exceeding $2 million [F1][S6][S8], reflecting accrued administrative expenses exceeding minimal current assets.

To finance transaction costs associated with pursuing the XDATA merger as well as general working capital needs before closing the business combination deadline (December 15, 2026), ALSAF relies heavily on sponsor-backed promissory notes and loan agreements totaling approximately $1.43 million outstanding as of December 31, 2025 [S4][S5][F1]. These notes bear no interest nor collateral but are repayable upon consummation of the initial business combination [S4][S6]. Notably:

- Four promissory notes issued between September 2022 and September 2023 originally totaled up to nearly $7.3 million but had principal waivers applied reducing them substantially [S4][S5].

- A loan agreement executed August 26, 2024 provides for up to $1.5 million in loans without interest for transaction fees; partial balances remain outstanding post-waiver [S4][S5].

- On March 16, 2026 another $0.5 million interest-free loan agreement was entered covering recent transaction cost advances [S6][S23].

Sponsor support remains essential since ALSAF’s operational cash burn exceeds internally available liquidity or generated interest income given depletion of most trust account assets following prior investor redemptions [S6][F1]. The inability to secure alternative financing or sponsor accommodations could jeopardize continued operations or delay closing.

Risks Surrounding Business Combination Completion and Shareholder Interests

Failure by ALSAF to complete its initial business combination by December 15, 2026—the Liquidation Date mandated under its articles—would trigger mandatory winding-up procedures including shareholder redemptions at trust account value followed by dissolution [S7][S12]. This risk threatens total loss of invested capital minus residual redemption amounts.

Additional risks include regulatory approval uncertainties given cross-border nature of the deal with an Estonian firm nested in a Cayman merger structure plus potential delays arising from shareholder vote dynamics or market conditions impacting redemption levels [S7]. Redemptions reduce available cash held post-IPO for deal financing which may force slower deal execution or changes in transaction terms due to Nasdaq requirements [S11][S26].

Integration challenges post-closing are inherent but unquantified given absence of operational history post-merger.

Capital Allocation: Focused on Transaction Funding Without Dividends or Buybacks

Capital allocation activity relates almost exclusively to funding business combination expenses via sponsor loans/promissory notes coupled with payment of operating expenses including monthly fees payable to sponsors for office space and administrative services totaling approximately $10 thousand monthly since December 2021 [S25][F1].

There have been neither dividends declared nor share repurchases conducted consistent with usual SPAC structures where returns accrue principally through successful mergers rather than ongoing payouts . Deferred underwriting commissions are payable upon business combination close but were partially waived reducing immediate outflows by nearly two-thirds compared to original commitments ($950 thousand vs. $2.875 million) reflecting negotiated cost efficiencies post-redemption activity [S29][F1].

Founder shares carry registration rights enabling resale registration post-business combination but do not impact current cash flows directly.

Summary Metrics: Operating Results and Financial Position Trends

The tabulated annual summary reveals consistent operating losses reflective of expense-heavy yet non-revenue generating status designed around preparing for acquisition completion:

- Operating income deteriorated slightly from -$913K in FY24 to -$888K FY25 indicating persistent costs albeit stable levels,

- Net income swung sharply into loss territory recently due largely to diminished trust account earnings amidst sizeable redemptions,

- Operating cash flows show deepening negative trends aligned with heightened transactional spend,

- Equity remains substantially negative reflecting accumulated losses exceeding contributed capital net of redemptions.

This trajectory underscores ALSAF’s challenge balancing cost management while advancing towards merger closure prior to liquidation triggers.

What Market Participants Should Monitor Going Forward

Key indicators shaping future investor perspective include:

- Timely consummation of merger steps including regulatory clearance updates,

- Shareholder voting outcomes signaling backing level,

- Updates on sponsor loan repayments or additional financings potentially required should transaction costs escalate,

- Any Nasdaq relisting progress for combined entity signifying regained exchange liquidity status,

- Redemption levels tendered which materially affect available cash reserves,

- Possible amendments impacting deferred underwriting commissions or capital structure changes.

Investor attention concentrated on these developments will offer visibility into whether ALSAF can successfully transition from blank check company to operating entity via OU XDATA platform thereby unlocking strategic value despite historically negative operating financials.

This analysis is based solely on publicly available SEC filings through March 20th ,2026 and associated data caches without extrapolation beyond stated figures or known facts about Alpha Star Acquisition Corporation’s SPAC status or proposed business combination with OU XDATA Group. It does not constitute investment advice nor recommendations regarding securities trading decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments