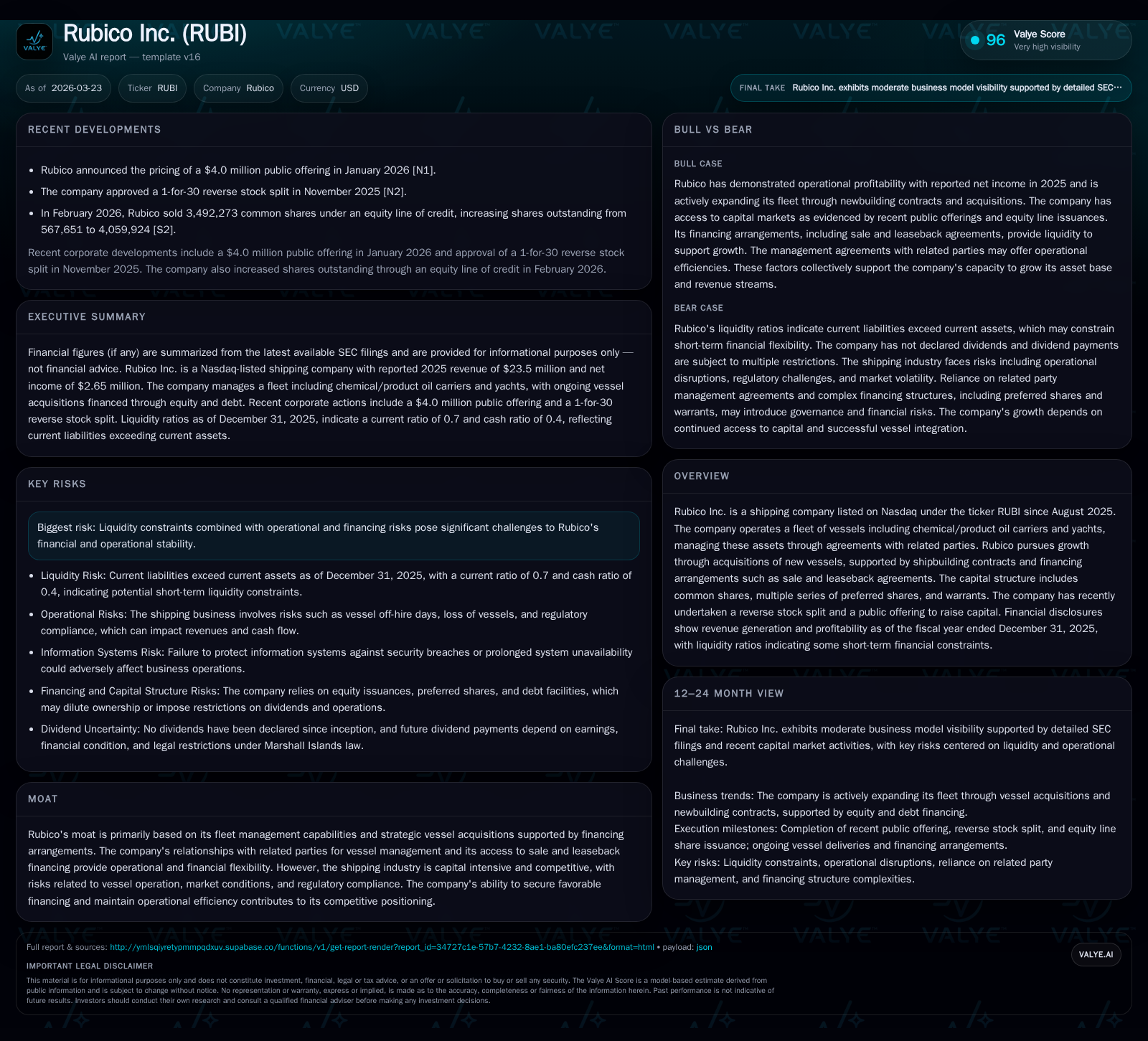

Rubico Inc.’s Trajectory from Fleet Expansion to Financial Footholds

Rubico has rapidly built a diverse fleet through strategic acquisitions and sale-leaseback financings, while addressing liquidity constraints that shape its financial footing.

Since its Nasdaq debut in August 2025, Rubico Inc. has pursued an aggressive growth model centered on acquiring vessels via purchase agreements and affiliated party management services. Revenue and profit generation for FY2025 demonstrate operational scale despite a tight liquidity position evidenced by a sub-1 current ratio. The company’s capital structure features multiple preferred share classes, warrants, and financing backed by guarantors, with newbuildings lined up through 2029. Dividend payments remain suspended pending financial stabilization, highlighting the balancing act between expansion ambitions and cash flow pressures. Monitoring upcoming vessel deliveries and debt installment schedules will be pivotal for assessing Rubico's evolving financial resilience.

Historical Growth Catalysts: Vessel Acquisitions and Fleet Management

Rubico's rapid emergence in the shipping sector has been anchored on concrete acquisition plays backed by ship finance mechanics typical of capital-intensive maritime ventures. The company entered into a Newbuilding SPA (Share Purchase Agreement) on December 31, 2025, to acquire Roman Explorer Inc., which owns the Newbuilding Yacht expected for delivery in Q2 2027. This transaction involved an initial installment settlement including advance payments totaling $19.5 million with remaining yacht construction installments of €35.5 million (approximately $41.7 million) payable through May 2027.[S1][S10][S8]

Further fleet growth via chemical/product oil tankers is secured through a February 20, 2026 SPA with Central Mare Inc., an affiliated party related to Mr. Evangelos Pistiolis' family. This acquisition targets Roman Shark IX Inc., contracted with Guangzhou Shipyard International for delivery scheduled in 2029.[S3][S8][S13]

These transactions leverage sale-leaseback financing structures where approximately 85% of pre-delivery installments are financed at an effective interest rate of Term SOFR plus margin (~1.80%). Upon vessel delivery, Rubico commits to quarterly installments of roughly $0.5 million over a decade, capped by balloon payments approximating $18.2 million payable at contract maturity.[S5][S13][S8] This financing approach mitigates upfront capex needs while preserving operational control.

Vessel management remains largely contracted out to related parties such as Central Shipping Inc., enabling specialized handling of commercial and technical operations yet creating intercompany dependencies that must be monitored for conflicts or concentration risk.[S10]

Operating Highlights and Financial Performance in First Year

Financial disclosures for the fiscal year ended December 31, 2025 reveal Rubico’s initial scale of operations during its inaugural reporting period post-spin-off from the former parent.[F1] Revenue totaled $23.5 million accompanied by robust operating income of $12.4 million — illustrating effective cost management or favorable charter rates early in their operational cycle.

Net income settled at approximately $2.65 million producing a modest return on equity near 5.8%, reflecting both growth stage capital deployment and existing leverage levels.[F1] However, the balance sheet highlights liquidity pressure with current assets recorded at $7.05 million versus current liabilities exceeding $10 million resulting in a sub-1 current ratio near 0.7.[F1]

Cash balances maintained at circa $4 million provide some runway for working capital needs but emphasize the tight operating liquidity environment common in shipping startups undergoing fleet buildup phases.[F1]

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Table summarizes Rubico's financial performance metrics for fiscal year ended December 31, 2025 based on SEC filings.[F1]

Navigating Capital Structure: Debt Facilities and Equity Raises

Rubico's capital structure exhibits complexity customary in nascent maritime operators striving to balance growth funding with manageable financial risk profiles.[S1][S4][S5][S8][S10][S11]

The company operates multiple series of preferred shares including Series D, E, and G each carrying distinctive dividend rights, conversion features, and transfer restrictions impacting shareholder value dynamics.[S26][S25][S27] Notably, some acquisition installment payments may be settled via issuance of Series E or G Preferred Shares depending on negotiation terms with related sellers.

Equity issuance activities underpinning liquidity included a January 2026 public offering delivering gross proceeds near $4 million through units bundling common shares and Class B warrants exercisable at defined prices.[S18] This was supplemented by an equity line facility executed in February boosting outstanding common shares from approximately half a million to over four million weighted shares outstanding within weeks.[S22]

The company also authorized a reverse stock split up to one-for-250 range designed to improve share price trading mechanics though timing remains at Board discretion.[S20]

On the debt front, vessel-owning subsidiaries benefit from sale-leaseback arrangements guaranteed by the former parent entity enhancing creditworthiness toward lessors while institutional term loans linked to floating benchmarks plus margins drive interest expense calculations.[S4][S5]

Covenants embedded across these credit facilities curtail dividend distributions if cash flows weaken or default events arise—reflecting restrictive frameworks typical of leveraged shipping plays with collateralized assets.[S6][S7]

Newbuilding Orders and Future Fleet Expansion Plans

Rubico’s growth blueprint extends beyond legacy assets into ordered newbuildings secured via binding shipyard agreements spread across different market segments.

The Newbuilding Yacht SPA concluded in late 2025 set an acquisition cost proximate to $38 million payable over about ten months post-agreement execution inclusive of prior down payments; delivery is slated for Q2 2027 aligning with seasonally strong charter demand windows.[S1][S10]

Chemical/product tanker expansion focuses on mid-size MR vessels measuring roughly 47,499 deadweight tonnage contracted at Guangzhou Shipyard International slated for completion in 2029 with employment contracts already secured presenting revenue backlog near $75 million including optional extensions.[S3][S13]

Such diversified asset mix combining luxury yachts alongside product tankers signals strategic risk balancing although it introduces operational segments unfamiliar to management requiring diligent execution oversight rooted in maritime sector core competencies such as off-hire day management or regulatory certifications.[S24]

Liquidity Challenges and their Operational Implications

A salient theme underscored throughout Rubico’s disclosures is constrained short-term liquidity manifested in a current ratio below unity,[F1] signaling that current liabilities exceed readily convertible assets posing working capital challenges.

The company details legal restrictions under Marshall Islands corporate law prohibiting dividend payments if insolvent or lacking operating surplus thereby mandating strong cash flow discipline given blocked access scenarios are credible.[S6]

Further vulnerabilities stem from unanticipated vessel off-hire days or extraordinary liabilities influencing near-term cash availability,[S1] exacerbated by debt repayment obligations including balloon installments due years ahead necessitating ongoing refinancing or equity injection strategies.

Such liquidity tightness could impact operational flexibility including capacity for dry-docking scheduling or crewing arrangements pivotal within volatile shipping cycles leading to elevated focus on treasury monitoring.

Capital Allocation Strategy: Dividends, Buybacks, and Returns

To date, Rubico has withheld dividend distributions commensurate with its growth phase status compounded by restrictive covenants attached to credit facilities limiting cash payouts under default or insolvency events.[S6][S7][F1]

Despite generating positive net income producing an approximate ROE of close to 6% within its first year,[F1] capital allocation prioritizes reinvestment into fleet expansion over shareholder return enhancement.

No share buybacks are disclosed nor expected given existing equity raises dilutive potential combined with funding demands aligned with planned vessel acquisitions requiring capital retention rather than distribution.[S6][S7]

This reflects prudent stewardship given nascent profitability trajectories common among shipping firms entering post-spin-off growth stages requiring sustained capitalization before resuming capital returns.

Risks from Financing Dependencies and Market Volatility

Rubico confronts intrinsic risks tied to an industry marked by cyclical freight rates sensitivity amplified by reliance on leveraged financing structures involving sale-leasebacks incurring fixed obligations regardless of charter market downturns.[S17]

Additional operating hazards referenced include regulatory compliance exposure specific to chemical/product tanker segment such as pollution prevention mandates alongside standard product liability claims arising from cargo mishandling — usual risk spheres maritime operators must actively manage.[S17]

Off-hire days result in revenue interruptions during maintenance or unexpected vessel downtime further stressing cash flows reinforcing the importance of robust operational risk controls embedded within charter party agreements and insurance coverage provisions.

Counterparty relationships with affiliated parties offer efficiencies but concentrate governance risks warranting transparent independent committee oversight as performed during recent newbuilding acquisitions.[S3][S13]

Outlook and Key Milestones to Monitor

Looking forward beyond FY2025 results absent explicit company forecasts,[N/A] critical milestones hinge upon timely delivery of contracted vessels such as:

- The Newbuilding Yacht projected for Q2 2027 closing involving scheduled installment settlements,

- The chemical/product oil tanker targeted for delivery in 2029 along with commencement of charters backing substantial revenue backlog,

- Adherence to quarterly installment payments on sale-leaseback financings including balloon sums maturing over coming decade,

- Additional capital raising activities balanced against dilution risk adaptations as fleet scales. Monitoring these will provide insight into Rubico’s capacity to solidify financial stability amid capital intensive growth while navigating sector cyclicality.

Disclaimer: This analysis is based solely on publicly filed SEC documents as of March 23, 2026 and does not constitute investment advice or prediction regarding Rubico Inc.’s stock performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments